The auto finance market is a trillion-dollar industry. It’s also very much a prime market, with subprime financing remaining at near-record lows in the second quarter.

by Melinda Zabritski

October 11, 2017

5 min to read

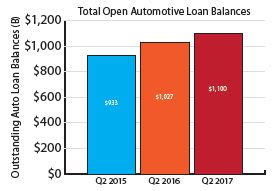

The auto finance market is growing, with the industry’s total balance of open automotive loans reaching a record $1.1 trillion in the second quarter. The only difference from the year-ago period, when loan balances first surpassed $1 trillion, is that the rate of growth has slowed from 10.13% to 7.12%.

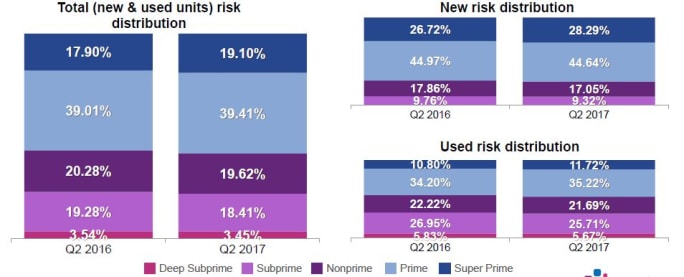

The industry reached new highs in several other key categories during the period, but not every record translated into more metal moving over the curb for dealers. Finance sources are tightening underwriting standards, with the high-risk tiers accounting for less than 20% of total balances. In fact, the market remains at near-record lows for subprime and fell to an all-time low for deep subprime.

Ad Loading...

But it wasn’t smooth sailing for prime customers, either, with record-high payments for new vehicles sending prime and superprime customers to used lots in record numbers. Leasing also remained above 30% of all new vehicles financed during the period. The following is a look at some of the trends that shaped the auto finance industry in the second quarter of 2017.

Prime, Superprime Tiers Gain Share The prime and superprime risk tiers captured 58.51% of the total finance market in the second quarter — up from 56.91% in the second quarter of 2016 — while the share of loans extended to borrowers with subprime and deep subprime credit dropped from 22.82% in the year-ago quarter to 21.86%.

The deep-subprime category alone fell to a record low of 3.45%. In fact, the last time the share of deep subprime fell below 4% in any second quarter was 2012, when the risk tier registered a share of 3.77%. The all-time low for deep subprime was recorded in 2011, when the high-risk tier’s share came in at about 3.64%.

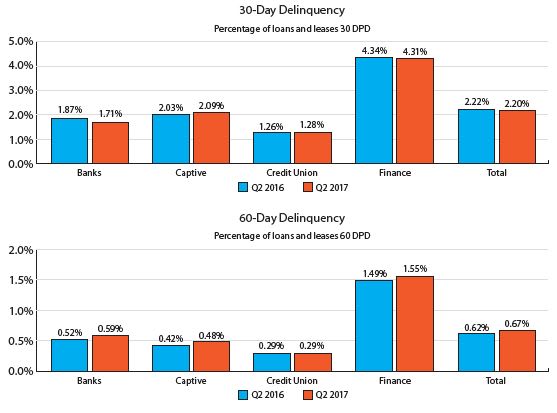

Typically, a decrease in the share for subprime and deep-subprime loans is tied to a rise in delinquencies. But that wasn’t the case in the second quarter, with delinquencies remaining relatively flat with the prior-year period.

Captives, Credit Unions Gain Market Share During the period, 30-day delinquencies inched down from 2.22% in the year-ago quarter to 2.2%, while 60-day delinquencies grew slightly from 0.62% to 0.68%.

Ad Loading...

If the 60-day delinquency rate continues to rise, the shift toward customers with higher credit scores is likely to continue. That scenario would play right into the hands of captives and credit unions, which typically cater to customers with better credit profiles.

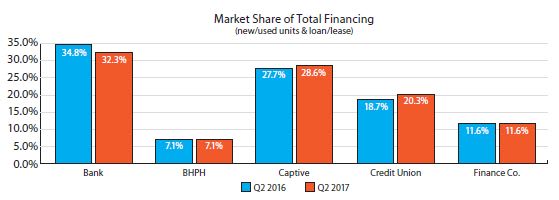

In fact, both captives and credit unions realized strong year-over-year market share growth as the market shifted more toward prime. Captives saw their share rise from 27.7% in the year-ago quarter to 28.6%, while credit unions saw their share jump from 18.7% in the year-ago period to 20.3%.

The story was different for banks. That segment’s share fell sharply from 34.8% in the second quarter of 2016 to 32.3%. Market share for finance companies remained flat with a year ago at 11.6%.

Credit Scores Rise for New and Used The second quarter also saw credit scores increase for all transaction types, another sign of the market’s shift toward car buyers with prime credit. For new-vehicle financing, the average credit score increased from 708 in the year-ago quarter to 711 — the highest second-quarter score since 2013.

For new-vehicle leases, the average credit score increased from 716 in the year-ago quarter to 722. The average for new-vehicle financing and leasing, combined, rose four points from a year ago to 714.

Ad Loading...

For used-vehicle financing, the average credit score rose four points from a year ago to 652. For franchised dealers, however, the average credit score for used financing fell one point from a year ago to 673, while the average score financed by independents increased by three points to 611.

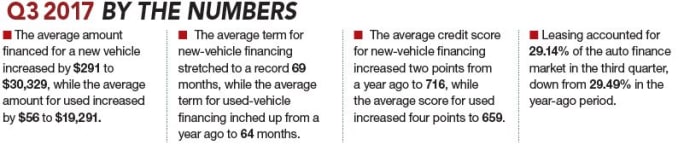

Amount Financed, Monthly Payments Rise Again With new-vehicle transaction prices registering year-over-year increases every month during the quarter before settling in at $34,442, according to Kelley Blue Book, it’s no surprise that the average monthly payment and amount financed followed suit.

In fact, the average monthly payment for a new vehicle increased by $27 from a year ago to a second-quarter record of $504, while the average amount financed for a new vehicle increased by $338 from a year ago to $30,324.

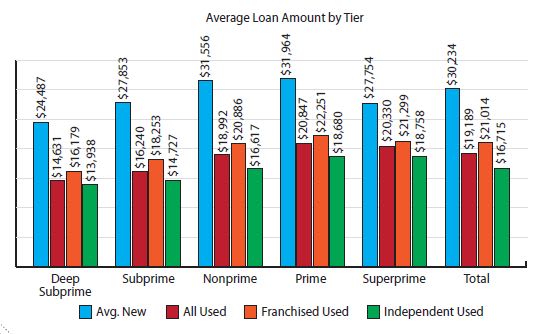

On the used side, the average retail transaction price increased 2.1% from a year ago to a second-quarter record of $19,227, according to Edmunds. That’s not far off from the average amount financed for a used vehicle, which rose by $81 from a year ago to $19,189. As for monthly payments, the average increased $6 from a year ago to $365.

That’s a difference of $139 between the average payment for a new vehicle and a used vehicle — and a likely reason a record 61.02% of prime consumers and a record 44.32% of superprime customers opted to finance a used-vehicle purchase in the second quarter. And if they weren’t shifting to the used-vehicle lot, car buyers were opting for longer terms in the new-vehicle space.

Ad Loading...

In the second quarter, the average term for new-vehicle financing inched up from 68.3 months in the year-ago quarter to 68.8 months, while the average term for used increased from 63.7 months to 64.

By term band, terms between 61 and 72 months led the way, accounting for 40.40% of all new-vehicle loans. Showing the sharpest growth, however, were the 73- to 84-month and 85- to 96-month term bands. The prior’s percentage of new-vehicle loans increased 1.22 percentage points from a year ago to 32.5%, while the latter increased by 0.3 percentage point to 1.25%.

Tracking the Subprime Pullback There are several factors at play when looking at the long-term trends. First, the need for vehicle affordability continues to grow. Higher-priced vehicles mean higher-priced loans, which could keep more high-risk customers out of the market. Second, if underwriting guidelines continued to tighten during a period in which the 30-day delinquency rate registered a decrease, finance sources are likely to tighten further if delinquencies rise even slightly.

Overall economic uncertainty could also be behind the more conservative approach demonstrated by finance sources, and a drop in the stock market or a spike in unemployment could bump delinquencies higher. It’s possible that finance sources are simply being proactive and hedging against a stagnant economy. As always, time will tell. For now, the market continues to grow and remains strong.

Melinda Zabritski is senior director of automotive credit for Experian Automotive. Email her at melinda.zabritski@bobit.com.

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.