Third-quarter data from Experian Automotive shows that the auto finance market gained strength and stability, but mostly at the expense of subprime originations.

by Melinda Zabritski

January 16, 2018

4 min to read

Loan balances rising above the $1 trillion mark wasn’t the big story coming out of the auto finance arena in the third quarter. The real stunner was subprime financing falling to its lowest point since 2012.

The subprime pullback dates back to the second quarter of 2016, with the auto finance industry doing its part to disprove talk of a subprime bubble ever since. In the third quarter, the rise in average credit scores for both new- and used-vehicle financing provided further evidence of the caution finance sources are taking when it comes to their portfolios.

Ad Loading...

In fact, much of the growth in overall loan balances came out of the superprime and prime tiers. But with credit delinquencies rising slightly, look for auto finance sources to continue steering their respective portfolios away from the high-risk tiers. The following is a look at some of the trends that shaped the auto finance industry in the third quarter of 2017.

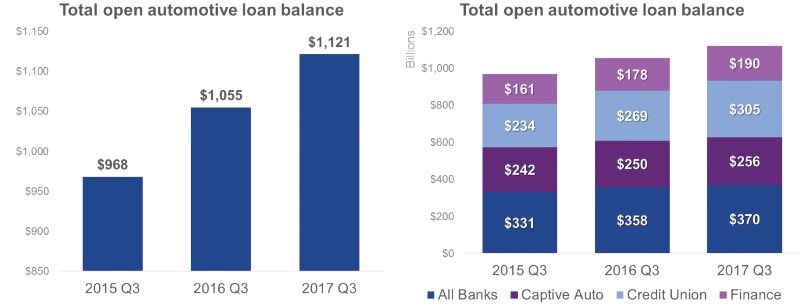

Overall Loan Market Rises 6.3% The overall auto finance market continued to grow at a rapid pace, with total outstanding loans rising 6.3% from a year ago to $1.121 trillion. And while all finance segments experienced portfolio growth, credit unions showed the most growth in terms of both total dollar volume (up $36 billion from a year ago) and by percentage (up 13% from a year ago). In fact, the segment exited the third quarter with its loan balances jumping from $269 billion in the year-ago quarter to $305 billion.

Finance companies also recorded significant growth in outstanding balances, which grew 6.7% from a year ago to $190 billion. Banks and captives registered the smallest year-over-year growth by percentage. Outstanding balances for banks grew 3.3% from a year ago to $370 billion, while balances for captives grew 2.4% to $256 billion.

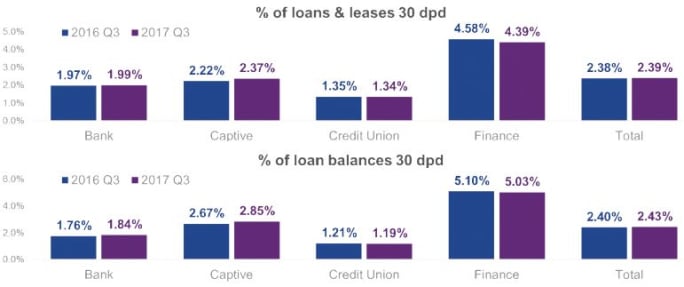

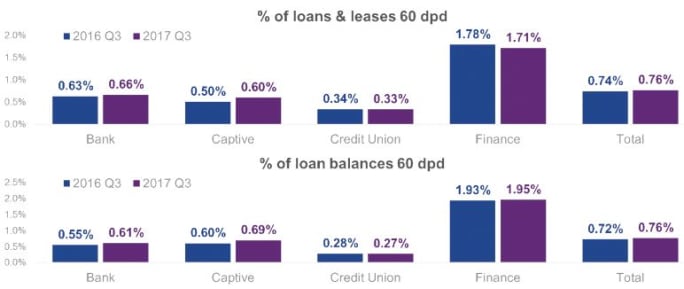

Delinquencies Show Slight Uptick Considered a critical bellwether for the auto finance industry, both 30- and 60-day delinquencies for loans and leases combined were up slightly from the year-ago period. For 30-day delinquencies, the rate increased from 2.38% in the year-ago period to 2.39%, while the 60-day delinquency rate inched up from 0.75% to 0.76%.

Even finance companies, which typically cater to credit-challenged consumers, registered declines in their delinquency rates. The segment’s 30-day rate fell from 4.58% in the year-ago period to 4.39%, while its 60-day rate fell from 1.78% to 1.71%. Lenders shift to higher-tier consumers.

Ad Loading...

The rise in delinquencies, albeit slight, caused finance sources to turn to the usual countermeasure of tightening credit standards. The result was a continued shift toward borrowers with prime and superprime credit.

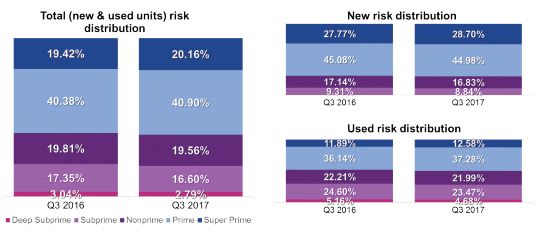

In fact, prime consumers accounted for the largest share of loans originated during the period, which increased from 40.35% in the year-ago quarter to 40.9%. The superprime risk tier, however, showed the largest percentage gain, rising from 19.42% to 20.16% of the market.

Conversely, market share for the nonprime, subprime and deep-subprime risk tiers all contracted. Nonprime’s share dropped from 19.81% in the year-ago quarter to 19.56%, while subprime’s share dropped from 17.35% of the market to 16.6%. Deep subprime’s share fell from 3.04% to a record low of 2.79%.

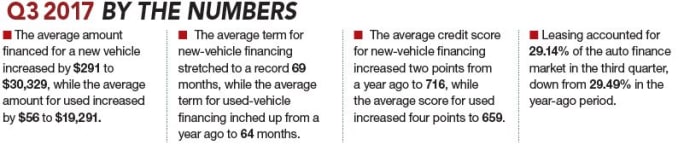

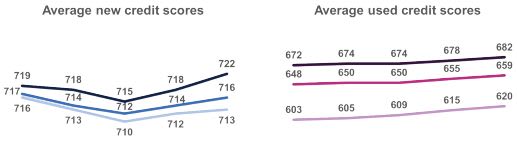

Credit scores reflected the contraction of the below-prime tiers. For new-vehicle financing, the average score rose from 712 in the year-ago period to 713. For used-vehicle loans, the average score rose from 655 to 659.

Shift Toward Prime Drives Down Share of Leasing Even leasing continued to shift toward prime and superprime customers, with the average credit score for a new-vehicle lease rising from 718 to 722. As a result of that shift, the transaction type’s total share of the finance market fell slightly from 29.49% in the year ago quarter to 29.14%.

Ad Loading...

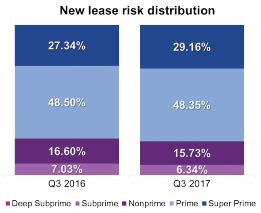

In the superprime risk tier, leasing’s share grew from 27.34% in the year-ago quarter to 29.16%. In the nonprime and subprime tiers combined, however, leasing’s share dropped from 23.63% to 22.07%.

Even the percentage of consumers choosing to lease dropped in every risk tier, as more consumers opted for a loan or paid cash. In the superprime and prime tiers, the percentage of consumers opting for a lease dropped from 34.6% in the year-ago period to 33.1%, while the percentage of nonprime consumers opting to lease fell from 32.2% to 29.4%. In the subprime and deep-subprime tiers, the percentage dropped from 25.1% to 22.4%.

Analytics, Consumer Behavior Contribute to Solid Market For some time now, the story in the auto finance industry has focused incorrectly on the rise in subprime lending. The data over the last several quarters, however, points to the entire market growing. Yes, subprime has grown, too, but only in proportion to the rest of the market.

The reality is the market is turning more prime, which is an encouraging trend given the rise in average amount financed and stretching loan terms. The tightening also demonstrates that finance sources are using data and analytics as part of the lending process. Consumers are also taking a more active role in managing their credit before buying a car. As long as these trends continue, the market should remain in good shape for the foreseeable future.

Melinda Zabritski is senior director of automotive credit for Experian Automotive. Email her at melinda.zabritski@bobit.com.

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.