Finding Greatness in the Box

F&I professionals who stop swinging for the fences and focus on base hits stand to gain the confidence of their customers and the per-copy average that comes with it.

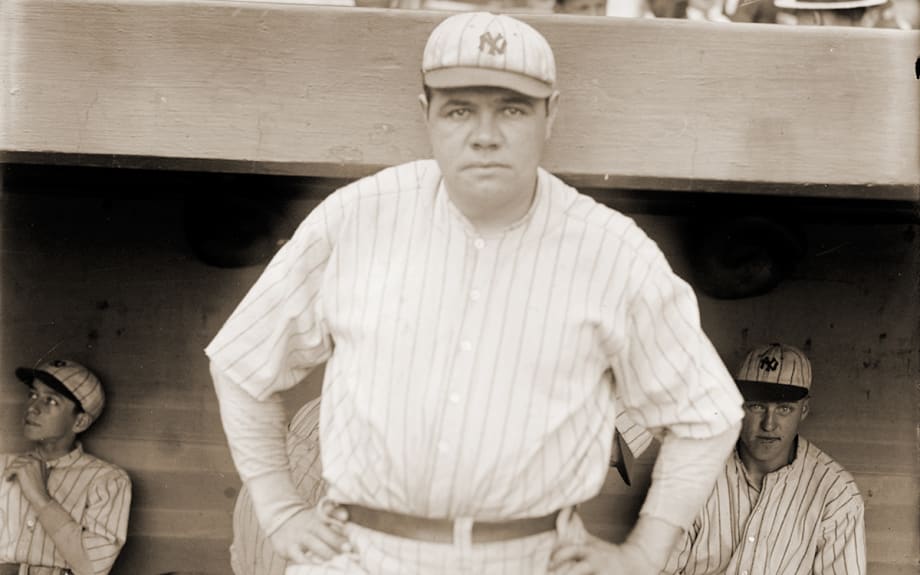

Babe Ruth became a baseball legend by hitting home runs, but he won pennants by batting runners in.

Photo by George Grantham Bain via Wikimedia Commons

Babe Ruth was a professional baseball player for 22 years. During his career, the “Sultan of Swat” faced opposing pitchers 8,400 times and was feared as a force to be reckoned with because of his ability to hit home runs. That said, over 91% of the time, he didn’t actually hit a home run.

Babe Ruth’s greatness actually occurred through runs batted in (RBIs). He only hit 714 home runs (an 8.5% success rate), but he was responsible for producing 2,213 RBIs — which wouldn’t have been possible without the base hits his teammates produced.

"Focusing on producing base hits might not feed my ego, but it will feed the success of the whole team. A base hit mentality doesn’t mean we never hit homers, but it does mean that we will be willing to take a walk or lay down a sacrifice bunt if it helps our team."

Take Barry Bonds. He hit more home runs than Babe Ruth but never won a World Series. The difference wasn’t personal ability. It was the ability of Babe Ruth’s teammates to produce base hits consistently.

In the box, we must strive for consistency. We get 60 to 70 at-bats a month and we typically don’t rotate through eight other players before we’re up again. I see a lot of F&I managers focused on the instant gratification and short-term goal of hitting a “home run.” That might feel exciting, but the bigger accomplishment is being consistent.

See, I believe in approaching every customer with short and long-term goals in mind, because the importance of reducing future risks like chargebacks and poor CSI cannot be ignored.

For instance, if I run a very high per-copy average but have a low penetration rate, you can bet I’m a home run hitter. You can be certain I’ll also have lots of “strikeouts,” a.k.a. chargebacks. My customers refinance, they cancel products, they refuse products in the future, and, if they feel taken advantage of, they never come back. This is not a formula for long-term success.

Focusing on producing base hits might not feed my ego, but it will feed the success of the whole team. A base hit mentality doesn’t mean we never hit homers, but it does mean that we will be willing to take a walk or lay down a sacrifice bunt if it helps our team.

See, in every transaction, the very first decision the customer makes is whether or not the salesperson can be trusted. By adopting a “win-win” attitude and standard pricing models, as well as striving to create loan structures that are intelligent for the customer, we show that our intent is focused on them. This allows customers to relax, consider the benefits, and trust you enough to say “Yes.”

Sure, I could ask for $3,000 over on a VSC every time, but a more intelligent method would be to adopt pricing habits based on the culture of my dealership and keep my pricing fair. If I find that I’m apprehensive to disclose the price of a product I’m selling, then it becomes obvious I’m only looking for a home run.

Trying to bury your customer actually lowers your chance of success. Like it or not, your eye movement, body language, and vocal tone will betray you, and the customer will subconsciously begin the process of telling you “No.”

It is of paramount importance to operate in harmony with your values. That means creating an offer for your customer that is fair. This may represent selling every product you have, but with a spirit of fairness in mind. You can always adjust your pricing to align with your goals, but consistency is the key. Build your menu around fair pricing and keep it consistent. If you need higher profits, raise your margins, but maintain consistency in product pricing.

Remember that our long-term goal is consistent income with low chargebacks and high CSI, and we share this goal with our customers and the dealership.

Lloyd Trushel is a 28-year veteran of the automotive business and co-founder of the Consator Group, an F&I development company specializing in customized training solutions. Contact him at lloyd.trushel@bobit.com.

More Auto Finance

Subaru Enters Lending Business

The automaker follows other brands in adding captive financing in the U.S., and says the move will strengthen its position here.

Read More →

Positive Equity Reaches Record High

Mainstream vehicle owners who bought a car seven years ago are likely to have positive equity when trading in for a new vehicle, according to second-quarter Edmunds data.

Read More →

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →