First Quarter Delivers Optimistic Outlook

Delinquencies and dollar volume of at-risk loans continued to fall in the first quarter, and auto finance sources responded, with shares of loans to credit-challenged buyers increasing by 11.1 percent. Experian Automotive’s director of automotive credit provides a snapshot of other auto finance trends from the quarter.

As the auto finance landscape continued to stabilize in the first quarter of 2011, lending sources continued to show a higher tolerance for risk. So what looked like a light at the end of tunnel in previous quarters now appears to be an expanding bright spot for the auto finance marketplace.

The clear winners for the quarter were drops in 30- and 60-day delinquencies, a growing share of new-vehicle loans for credit-challenged customers, lower dollar volumes of at-risk loans and a drop in the average loan age. The quarter also represented the best time in 30 months for consumers to secure an auto loan, and all signs point to a market that will continue to improve and expand.

Drop in Delinquencies Lowers At-Risk Loan Volumes

Vehicle owners did a significantly better job making payments on time in the first quarter, helping the automotive finance market stabilize more than it had during the year-ago period.

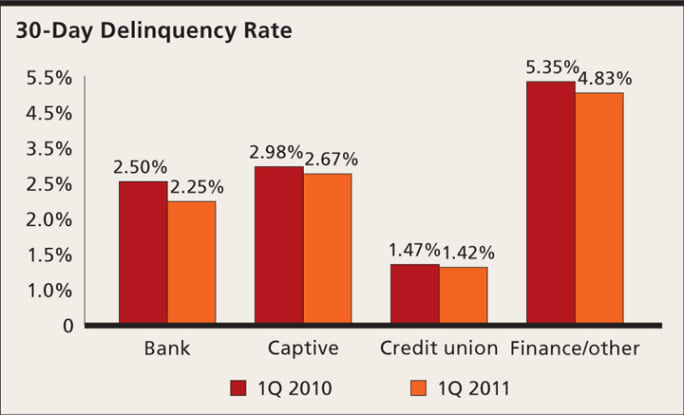

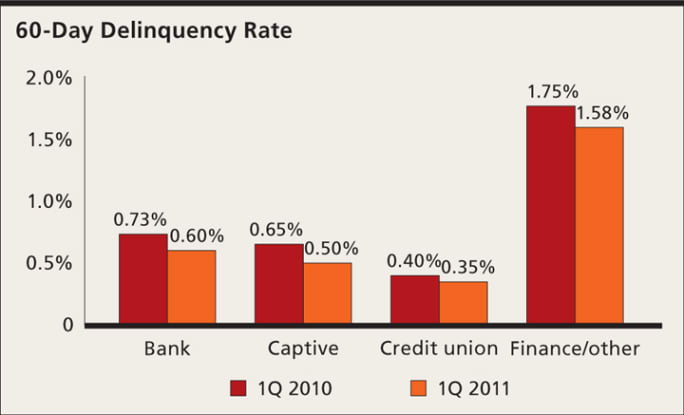

Thirty-day delinquencies are at their lowest point since the fourth quarter of 2008, giving lenders a little more leeway in their credit decisions. Having dropped 7.95 percent, 30-day delinquencies contracted to 2.52 percent in the first quarter from 2.74 percent a year ago. Sixty-day delinquencies dropped by 13.45 percent in the same period, with the captive finance segment enjoying the largest decline.

In addition, those drops in delinquencies lowered the total dollar volume of at-risk automotive loans from nearly $20 billion in the first quarter of 2010 to $16 billion in the first quarter of this year.

Lenders Ease Loan Criteria

In a stabilizing automotive credit market, lenders were in a better position to loosen lending criteria and provide more consumers with opportunities to qualify for loans.

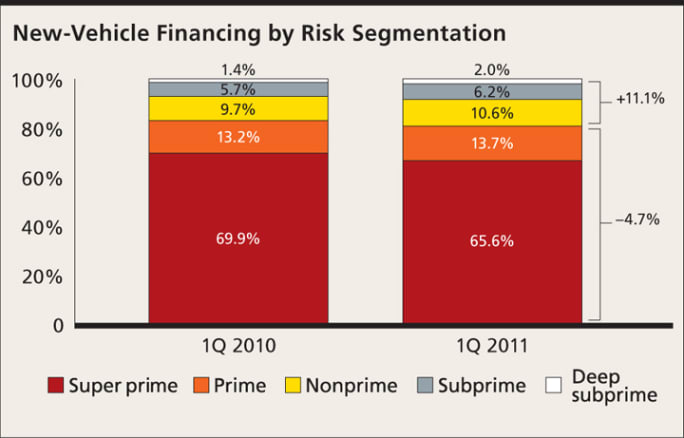

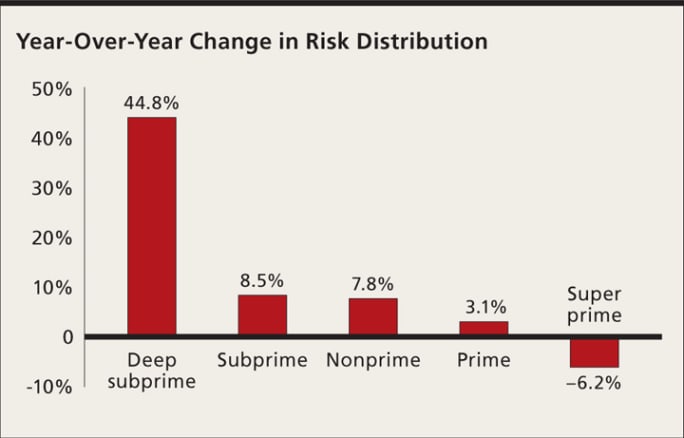

The share of loans to credit-challenged new-vehicle shoppers increased 11.1 percent from the year-ago period. The share of loans made to the nonprime segment increased from 9.71 percent in the year-ago quarter to 10.57 percent. The share of loans made to subprime customers jumped from 5.67 percent to 6.16 percent, while the share of loans made to deep subprime customers rose from 1.38 percent to 2 percent.

The improving ease of obtaining a new-vehicle loan also was reflected in average credit scores. For new-vehicle financing, the average credit score fell to 766, 10 points lower than in the first quarter of 2010. Coincidentally, 766 also was the average score in the fourth quarter of 2008, after which the market began to contract in earnest.[PAGEBREAK]

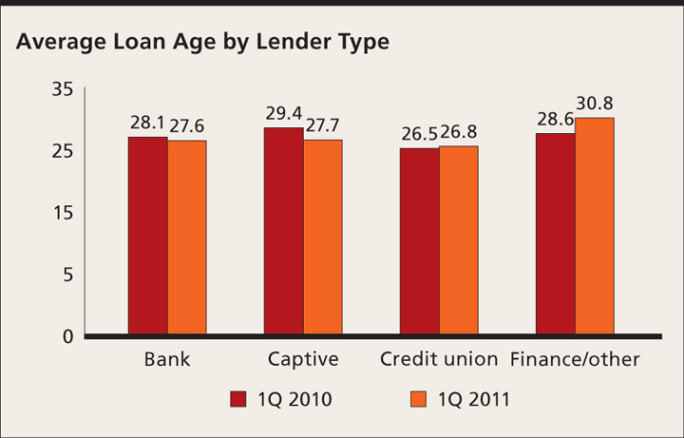

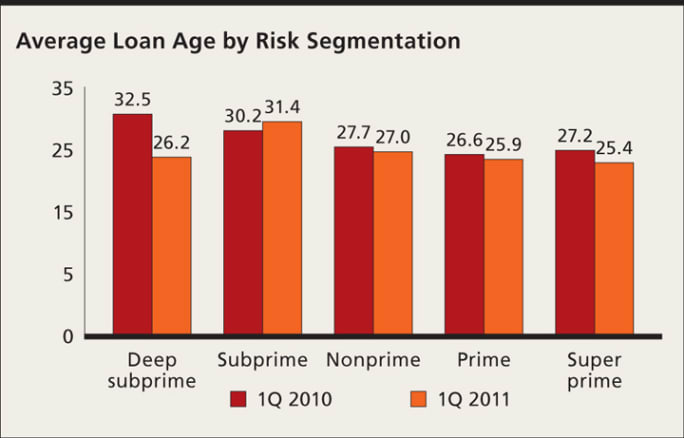

Loan Ages Decline as Consumers Return to Market

Despite all the buzz about the sluggish economy causing consumers to hold on to their vehicles longer, loan data suggests that this may not be the case. Taking into consideration variances with different lenders and risk tiers, the average age of vehicle loans in the first quarter was 27.89 months, down from 28.14 months in the year-ago period.

Among lenders, loan age for banks and captive lenders dropped, while the average loan age for credit unions and finance companies increased. Finance companies showed the largest spike, moving from 28.64 months in the first quarter of 2010 to 30.82 months in the first quarter.

Loan age for all risk tiers except for subprime, which jumped by 1.22 months, experienced a drop from the first quarter of 2010 to the first quarter of this year. Loan age fell 1.82 months for superprime customers, 0.69 months for prime customers and 0.76 months for nonprime customers. Loan age for the deep subprime segment plummeted by 6.25 months.

This data points to customers with solid credit returning to market faster than in 2010, which bodes well for new-vehicle retailers and for lenders with portfolios geared toward higher-end credit customers.

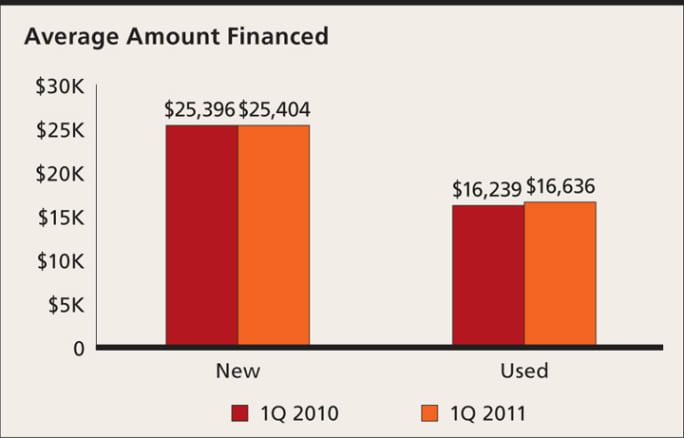

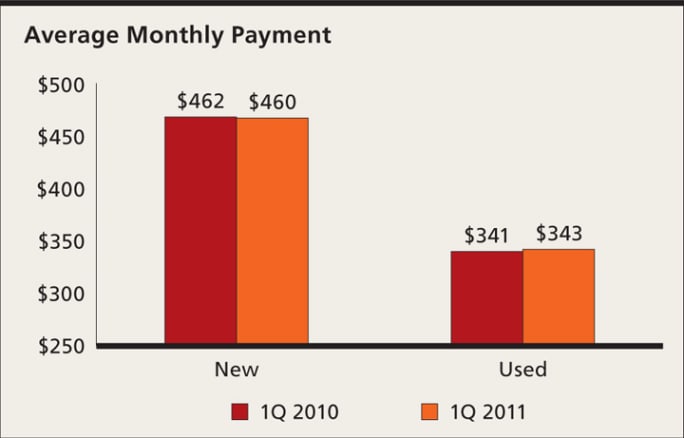

Financing and Monthly Payments Remain Flat

There was little change in loan characteristics, with monthly payment, loan length and amount financed staying relatively stable. The average loan amount for a new vehicle increased by a mere $8 to $25,404 in the first quarter, while the average used-vehicle loan increased by $397 to $16,636 in the first quarter of this year.

Average monthly payments showed little movement as the average new-vehicle payment fell from $462 to $460, while the average used-vehicle payment rose from $341to $343. Loan terms followed suit, jumping just one month for both new and used vehicles. Terms for new vehicles jumped from 62 months to 63 months, while used increased from 57 months to 58 months.

Continued Expansion Rests on the Economy

The combination of improved consumer payments and lower dollar volumes at risk has given lenders breathing room to loosen their overall lending criteria. It’s also made it easier for automakers to get customers into new vehicles.

Brighter days are ahead for lenders and automotive retailers should these trends continue. However, if sustained economic turmoil causes consumer delinquencies to sneak back up, the lending industry could contract once again.

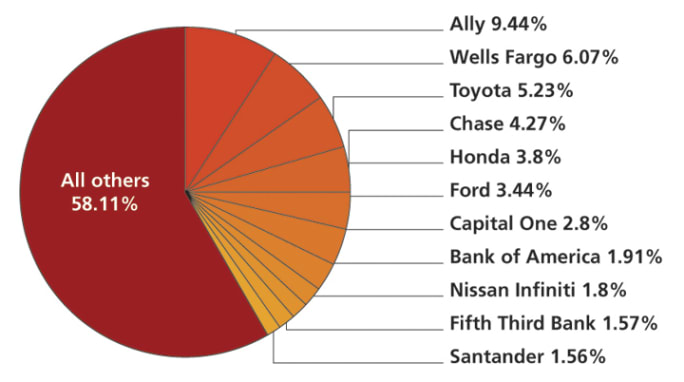

Top 20 Lenders by Market Share

Melinda Zabritski serves as director of automotive credit for Experian Automotive. E-mail her at melinda.zabritski@bobit.com.[PAGEBREAK]

SIDEBAR: 1Q By the Numbers

The average credit score for used-vehicle customers was 663, down two points from 665 in the year-ago quarter.

The average loan amount for a new vehicle was up $8, increasing from $25,396 in the year-ago quarter to $25,404.

The average loan amount for a used vehicle jumped $397, increasing from $16,636 in the first quarter of this year.

The average loan term increased by a full month, jumping to 63 months for new vehicles and 58 months for used.

More Auto Finance

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →