High New-Vehicle Prices Drive Auto Finance Industry to New Highs in Q1

The industry smashed several records in the first quarter thanks to high new-vehicle prices, but stretching terms and leasing weren’t the only ways consumers sought payment relief.

Courtesy of iStock.

The first quarter provided a good lesson in the principle of causation, with the continued rise in new-vehicle pricing causing three closely-watched loan attributes to reach new highs in 2016’s opening quarter. The net effect is that consumers will be paying more per month and will be doing so over a longer period of time.

Reaching new highs was the average finance amount and monthly payment for a new vehicle, with the prior surpassing the $30,000 market for the first time ever at $30,032. The latter increased by $15 to $503.

But the continued rise in new-vehicle prices did more than push several loan attributes to record levels. It also caused consumers to explore alternative financing options, with leasing continuing to serve as a viable alternative for payment-conscience car buyers. In fact, leasing accounted for a record 31.1% of all new-vehicle transactions in the first quarter, with credit-worthy consumers able to secure a monthly lease payment that averaged $100 less than the average monthly payment for a new-vehicle loan.

The following is a look at some of the trends that shaped the auto finance industry during the first quarter of 2016.

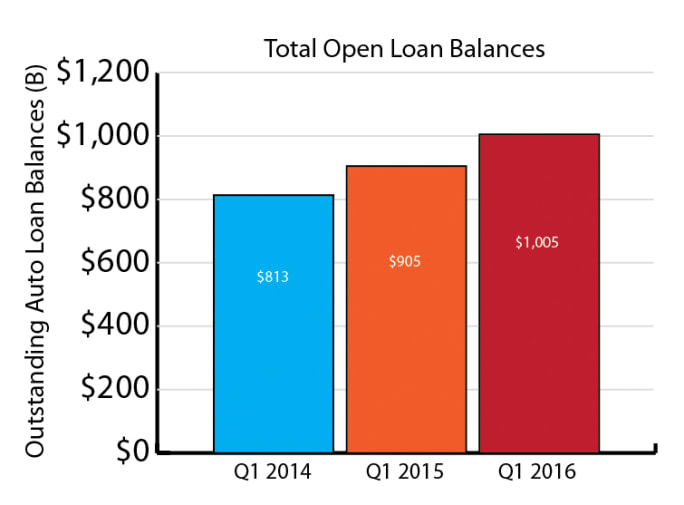

A New High

The big news coming out of the first quarter was the industry’s total balance of open automotive loans, which increased 11.1% from a year ago to $1.005 trillion. This was the first time the industry surpassed the $1 trillion mark, with much of that growth fueled by finance companies. That segment’s total outstanding balance increased 25.6% from a year ago to $170 billion.

Credit unions posted the second biggest increase, with the segment’s outstanding balance increasing 15.9% from a year ago to $249 billion. Outstanding balances for banks increased 7.9% from a year ago to $244 billion, while captive finance companies increased their outstanding balances by 6.7% to $343 billion.

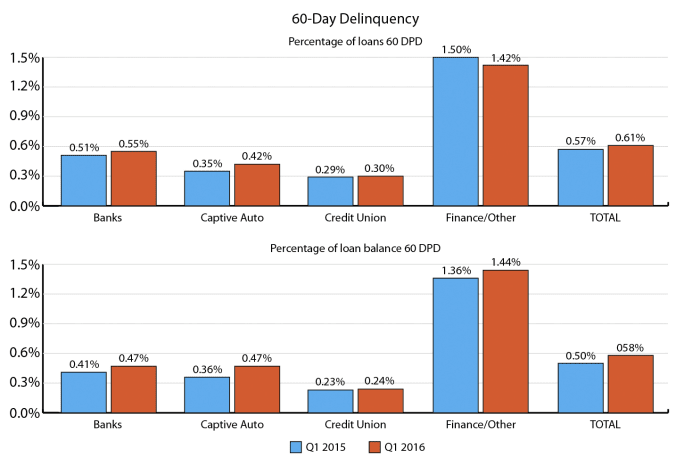

Delinquencies Rise as Subprime Grows

The first quarter also saw an increase in subprime financing, with financing secured by credit-challenged consumers accounting for 18.8% of all open automotive loans and leases. That’s a 10.9% increase from the prior-year period. Despite the uptick, prime consumers still make up the largest share of open loans and leases at 63.4%.

Still, the increase in subprime financing did impact delinquency rates, with both 30- and 60-day rates showing slight increases. The prior increased eight basis points from the year-ago quarter, accounting for 2.1% of all open automotive loans in the first quarter. The 60-day rate increased four basis points from a year ago, accounting for 0.6% of all open automotive loans during the period.

However, finance companies, which typically play in the high-risk tiers, actually lowered their 30- and 60-day delinquency rates. In fact, the 30-day rate for finance companies decreased 29 basis points, while the 60-day rate decreased eight basis points.

While the uptick in delinquencies isn’t a surprise given subprime’s increased share, the decrease in delinquency rates for finance companies is. It’s why the industry would do well to keep a close eye on these trends in the coming months and quarters.

Prime Borrowers Shifting Away From New

As previously mentioned, the continued rise in new-vehicle prices is pushing car buyers to seek out alternative financing options. It’s also forcing more prime consumers to consider the used-vehicle market. In fact, 54% of prime borrowers elected to purchase a used vehicle during the first quarter, a 4.8% increase from the year-ago period.

It’s that shift that’s impacting the average credit score and interest rate for used-vehicle financing. In the first quarter, the average credit score for used-vehicle financing ticked up three points from the year-ago period to 645, while the average interest rate for a used vehicle financed during the period fell 2.7% from a year ago to 7.8%.

Additionally, the average interest rate for used-vehicle financing secured at independent dealerships dropped from 12.23% in the year-ago period to 12.22%. Conversely, the average rate for new-vehicle financing increased eight basis points to 4.79%, while the average credit score for a new vehicle financed during the quarter fell three points to 712.

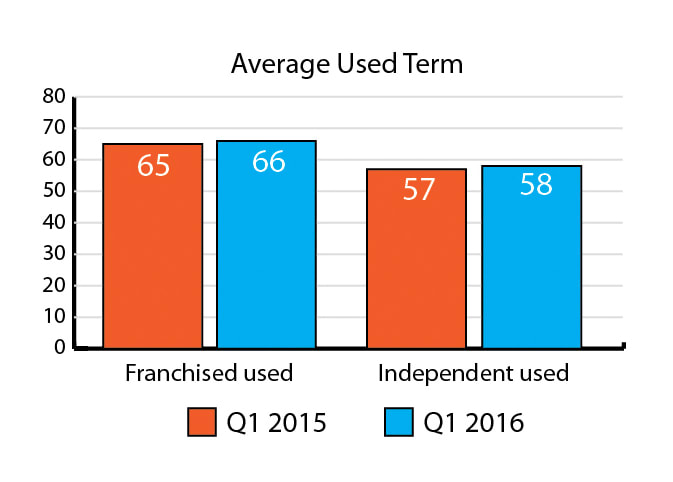

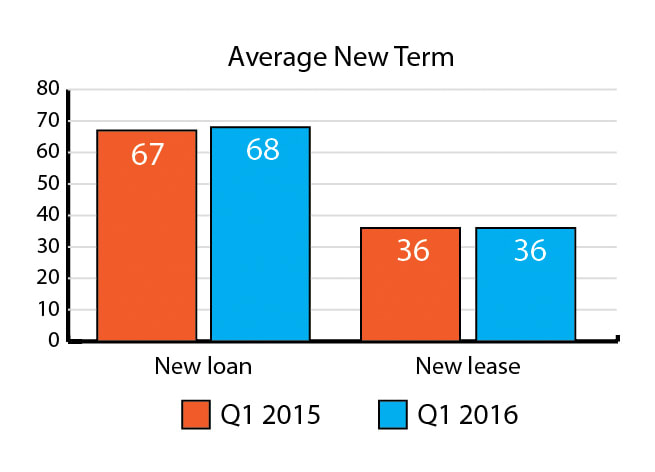

Stretch Effect Continues

Another way consumers are combating high new-vehicle prices is by extending loan terms. In the first quarter, the average term for a new vehicle financed during the period reached 68 months — the highest level on record. As for used, the average term increased one month to 66 months.

Eye on F&I

The last time the industry reached the $1 trillion mark — including both the total balance of open loans and leases — was in the third quarter 2015, so the industry’s first quarter performance was certainly notable. Even the total balance of open leases reached an all-time high of $76.9 billion, growing 27.66% from the year-ago period. So, yes, the auto finance industry opened the first quarter with a bang.

And with more and more car buyers relying on financing, it’s critical that finance sources and dealers keep a close eye on delinquency trends to ensure the market remains healthy. Likewise, consumers need to continue to do their part by making their loan payments on time to keep affordable financing options open and available.

So whether it’s growth in leasing, longer loan terms or the next new trend, the automotive industry needs to continue monitoring fluctuations in the market to stay ahead of the competition. The principle of cause and effect tells us that if the industry does exactly that while helping consumers meet their payment obligations, the automotive marketplace will continue to shine.

Melinda Zabritski serves as senior director of automotive credit for Experian Automotive. Email her at melinda.zabritski@bobit.com.

More Auto Finance

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →