Priced Out

Record highs in two critical auto finance categories make clear that vehicle affordability is becoming a big problem for car buyers.

©GETTYIMAGES.COM/GPOINTSTUDIO

The dream of owning a new vehicle is becoming more elusive to the average American, with the average amount financed and monthly payment for a new vehicle climbing to record highs in the opening quarter of 2018.

The average amount financed for a new vehicle in the first quarter increased by $921 from the year-ago period to a new high of $31,455. And with the average interest rate for a new vehicle jumping to 5.17% during the period, the average monthly payment for a new vehicle rose $15 from the prior-year period to a record $523.

And car buyers found little relief in the pre-owned market, where the average amount financed for a used vehicle rose $410 from the prior-year period to a record high of $19,536. Leasing also is becoming more difficult for payment-conscious consumers, with the average new-vehicle lease payment jumping from $410 to $436 over the same period.

Bottom line, it’s getting more and more challenging for the average American to find affordable transportation. But higher costs are just part of the equation. The following is a look at some of the trends that shaped the auto finance industry in the first quarter of 2018.

A Risk-Averse Market

In addition to higher loan amounts and monthly payments, finance sources were quite discerning when it came to creditworthiness in 2018’s opening quarter, as evidenced by the uptick in credit scores. For new-vehicle financing, the average customer credit score was 716, up two points from the year-ago period and six points from the first quarter of 2016. For used, the average credit score rose three points from a year ago to 655. Since the first quarter of 2014, however, the average credit score for used financing has climbed 14 points.

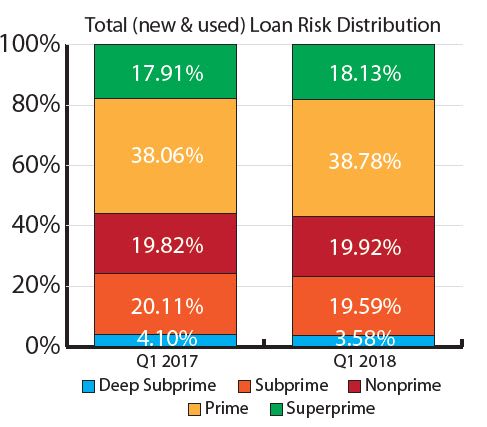

The rise in average credit scores caused a corresponding drop in subprime and deep subprime financing. Deep subprime’s share of the market in the first quarter fell from 4.10% in the year-ago period to 3.58%, while subprime’s share fell from 20.11% to a first-quarter record low of 19.59%. The declines caused the total subprime segment’s share to fall from 24.21% in the year-ago quarter to a record low of 23.17%.

In contrast, the prime and superprime shares continued to grow in the first quarter, with the percentage of new-vehicle loans made to consumers in the low-risk tiers reaching 73.4%. That’s up from 72.16% and the highest first-quarter level since 2012, providing further evidence that finance sources have become more risk-averse.

Low Delinquencies Provide Hope

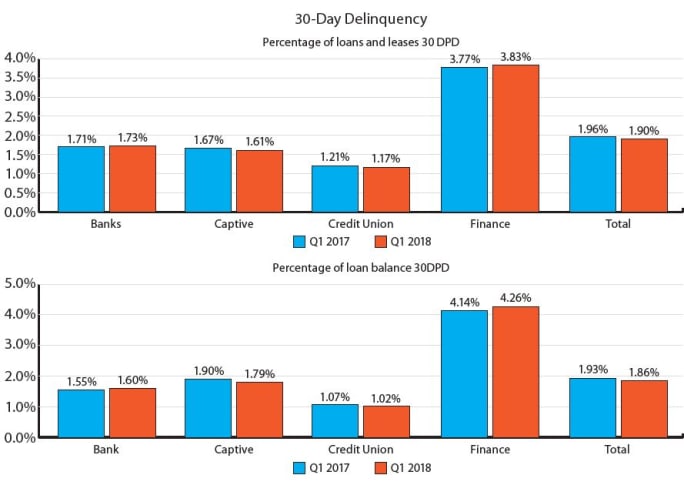

The key to reversing these trends are consumers — that’s if they continue to make timely payments. In the first quarter, the percentage of loans 30 days delinquent inched down from 1.96% in the year-ago quarter to 1.90%. The percentage of loans 60 days delinquent, however, remained flat at 0.67%.

Lender appetite for risk may seem to swing like a pendulum. Today, that pendulum appears to be swinging in the direction of car buyers with high credit scores. But if delinquencies drop, the pendulum could swing back toward a more risk-tolerant strategy. That doesn’t mean finance amounts and monthly payments will fall, but it does mean a likely drop in average credit scores for new- and used-vehicle financing.

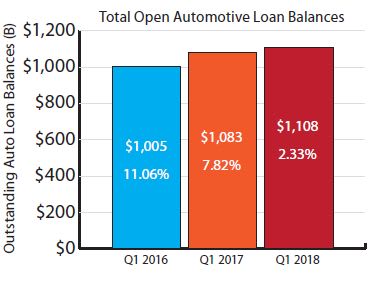

Record High Loan Balances

The expectation among industry pundits early on was that auto sales are headed for a slowdown. Yes, the market has cooled, but it is still on a 17.1 million-unit pace for 2018. It’s one of the reasons open auto loan balances climbed to record highs in recent quarters.

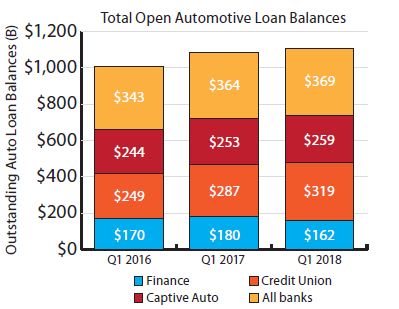

In the first quarter of 2018, total open automotive loan balances jumped 2.33% from a year ago to a record $1.108 trillion. Banks continued to capture the largest share of the market, growing their auto loan balances by $5 billion from the year-ago period to $369 billion. Within striking distance are credit unions, which grew their total loan dollar values by a market-leading $32 billion from a year ago to $319 billion.

Captives grew their auto loan balances by $6 billion from the prior-year quarter to $259 billion.

The only lending segment to lose ground on a year-over-year basis was finance companies, which typically cater to credit-challenged customers. The segment’s total loan balances fell from $180 billion in the first quarter of 2017 to $162 billion in 2018’s opening quarter.

In terms of overall market share, credit unions were the big winners. The segment’s share jumped by 6.9% overall, while banks lost 2.5% share. Finance companies and captives also saw their shares fall 1.8% and 1.1%, respectively.

Restoring the Dream

As previously mentioned, the dream of owning a new car is becoming more challenging for the average American thanks to record-high finance amounts, rising interest rates, and record-high monthly payments. Risk aversion among finance sources is also keeping some credit-challenged customers on the sidelines.

As finance sources take a deeper dive into current data, they will better understand the current reality and make more informed decisions. They may begin to explore options to make new-vehicle ownership more accessible and appealing — at least until the pendulum swings the other way.

Melinda Zabritski is senior director of automotive credit for Experian Automotive. Email her at melinda.zabritski@bobit.com.

More Auto Finance

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →