Rethinking Leasing

What if there was an F&I product on your menu that could guarantee the trade-in value of your customer’s vehicle? Leasing expert breaks down the fundamentals of this often-overlooked option.

It’s important to make sure the customer knows leasing offers a fixed price purchase option. This structure allows the customer to capture any equity at lease end if the vehicle is worth more than the residual value.

Why are F&I professionals so invested in selling “used-car futures?” Don’t think you’ve ever sold one? Think again. A retail installment sales contract (RISC) is essentially a used-car future because new-vehicle financing is a product that loads the customer with the risks inherent to the used-car market; specifically, the value of his or her vehicle at trade-in time.

If you asked your new-car customers whether they would prefer to take the risk of selling their vehicle against the vagaries of the market or drive off with a guaranteed trade-in value, how do you think they’d answer? A better question is: How many of you can predict used-car values three or four years out and can guarantee the trade-in value of your customer’s vehicle?

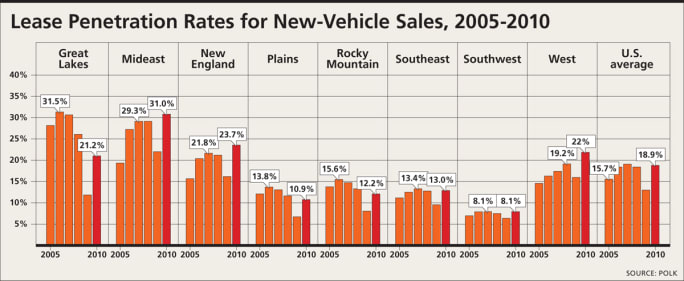

If you’ve been in F&I more than five minutes, you know one central mantra is to present 100 percent of your products to 100 percent of your customers. But how many F&I professionals present leasing to every customer? Unless you work in a luxury dealership, I would venture to guess that the answer is, “Not very many.” I could list many reasons why that is, but they boil down to two: First, a lack of understanding of the benefits to the customer and, second, inexperience in addressing their objections and misunderstandings accurately and confidently.

3 Ways to Present Leasing

There are several options available for presenting leasing accurately. As with any F&I product, the key to a successful presentation is to start by understanding the customer’s concerns and needs, along with his or her expected driving pattern and trade cycle.

The main benefit of leasing is the protection it provides against unexpected depreciation. With that protection comes two key advantages: If the model doesn’t depreciate faster than expected, the customer enjoys a residual value that is higher than he or she could have expected to negotiate as an end-of-term trade-in value. Better yet, the customer won’t have to negotiate the trade-in value in the first place. Thus, it’s critical that you understand how valuable those benefits are to a customer.

Most customers — and, I venture to say, most F&I professionals — don’t understand that the average lease saves the customer thousands of dollars of paid-in depreciation. It also is important to make sure the customer knows leasing offers a fixed price purchase option. This structure allows the customer to capture any equity at lease end if the vehicle is worth more than the residual value.

Let’s take a look at three methods you can employ to make those benefits clear:

Problems and Solutions: The most straightforward way to present leasing is to share your expertise on the pitfalls of trade-ins and how to avoid them. Here’s a workable word-track: “Many of our customers have returned hoping to trade in their vehicles after a few years, but found they had significant negative equity and couldn’t afford to trade. We have a finance option that offers a guaranteed trade-in value. Would you be interested in learning how that works?”

Another effective word-track is: “Many of our customers have found that the trade-in value of their vehicle is less than they expected. Often, that makes it too expensive to get the new model they want at the time they want it and at a payment they can afford. We have a finance option that offers a guaranteed trade-in value. Would you like to hear more?”

Finance vs. Lease Comparison: Another clear way to present leasing is to offer a quick comparison of financing vs. leasing, which you can do using data from third-party sources. The Federal Reserve’s “Keys to Leasing” brochure (www.federalreserve.gov/pubs/leasing/) lists nine comparison items, including up-front costs, monthly payments and future value.

The Association of Consumer Vehicle Lessors’ Website (www.acvl.com) is even more comprehensive. The ACVL lists 17 items, 14 of which are “Different Items” that offer comparisons between financing and leasing. One of the most persuasive is “D1: Monthly Payments,” which describes how leasing allows customers to drive a more expensive vehicle for a similar monthly payment.

Finance vs. Lease Quiz: A third alternative and my personal favorite is to invite the customer to take a quick, multiple-choice quiz to determine which finance option fits his or her needs and preferences better. Again, the ACVL Website offers an excellent resource. Its questions touch on subjects ranging from maintenance costs to annual mileage, but they all point to the same conclusion: Leasing is an excellent option if you don’t plan to drive your new car into the ground.

Randall McCathren is an attorney and consultant with BLC Associates. His more than 28 years of experience in consumer vehicle leasing includes representing industry members in the formulation of Regulation M and consulting with the Federal Reserve Board on leasing regulatory issues. Contact him at randall.mccathren@bobit.com.

More Auto Finance

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →