Subprime Auto Lending Hits 11-Year Low

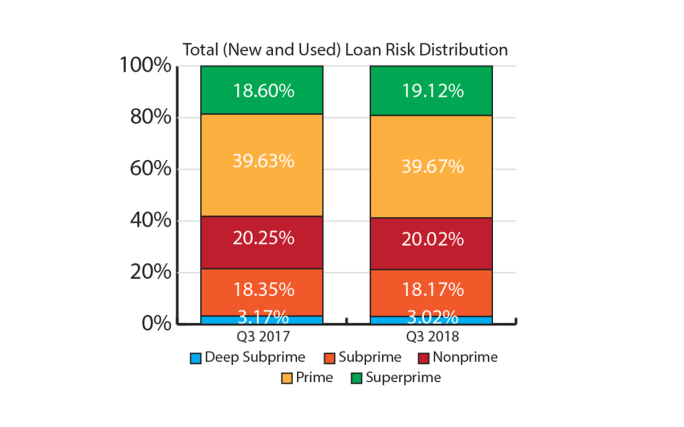

The third quarter of 2018 saw an alarming plunge in lending to subprime and deep-subprime customers, falling to 21% of all auto loans as banks and finance companies continue to favor the upper credit tiers.

The latest reports are a tale of woe for special finance, which continues to lose ground as banks and finance companies rebalance their portfolios.

Photo by anyaberkut via Getty Images

The total outstanding automotive loan balance again reached new heights in Q3 2018, hitting a record $1.17 trillion. But while the balance continued its upward trend, the mix of car buyers shifted substantially during the quarter. With many finance sources reassessing their risk-management practices and an improvement in consumer credit behavior, the percentage of subprime auto loans plunged to its lowest level in 11 years.

Subprime and deep subprime auto loans accounted for 21.19% of the total auto loan market, down 1.5% from a year ago. Alternatively, loans to prime and superprime customers rose from 58.23% in Q3 2017 to 58.79% in Q3 2018.

Much of the decrease in subprime lending was driven by higher growth rates of lower-risk car buyers in the used-vehicle market. In fact, more than 50% of the used market is made up of prime and superprime borrowers for the first time since Q3 2010.

On the flip side, loans for subprime borrowers made up the lowest percentage (22.86%) of the used-vehicle loan market on record, while used-vehicle loans for deep-subprime borrowers reached an all-time low of 4.33%.

Monthly Payments Reach Record Highs

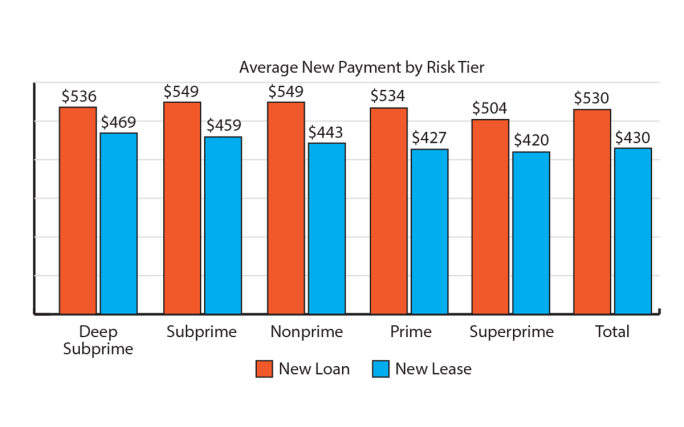

One of the trends that may be pushing many of the prime and superprime borrowers into the used-vehicle market is affordability. New and used-vehicle monthly loan payments reached historic levels as interest rates continued to rise in the third quarter of 2018. The average new-vehicle monthly payment reached $530, up 6% from a year ago. The average new-vehicle monthly lease payment was $430, approximately a 4% increase from last year. Additionally, the average used-car monthly loan payment hit a high of $381, another 4% increase.

The gap between new and used monthly payments also continues to widen, with the average new-vehicle monthly payment $149 more than the average monthly payment for used vehicles.

Given many car shoppers base their decision on monthly payment — and with such a sizeable difference between new and used monthly payments — some consumers may opt for the less-expensive vehicle.

Credit Scores and Credit Unions on the Rise

The average credit scores for new- and used-vehicle loans continued to increase, reaching 717 for new vehicles and 661 for used. Average credit scores for new-vehicle leases rose three points to 724 while new-vehicle loans also were up one point to 714. Franchise used scores increased one point to 683 while the independent space rose three points to 623.

The shifts in portfolio management have positively impacted credit unions, while banks were the only source to see a decrease in total outstanding automotive loan balances. Banks saw a decrease of approximately $1 billion in balances from a year ago, reaching $369 billion. Meanwhile, credit union balances maintained double-digit growth.

Other notable loan balance growth for this period includes captives (up 2.75%) and finance companies (up 5.07%).

30-Day Delinquency Rates Improve

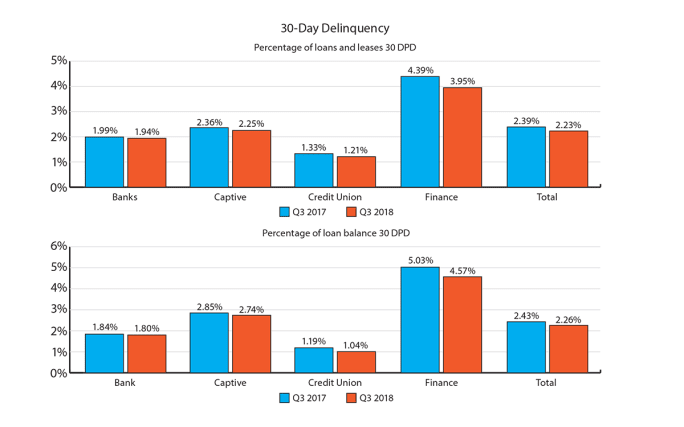

Overall delinquency rates continued to improve, providing another sign of auto loan market stability. The 30-day delinquency rate fell from 2.39% in Q3 2017 to 2.23% in Q3 2018. For 60-day delinquencies, rates fell from 0.76% in Q3 2017 to 0.72% in Q3 2018.

While the automotive finance market is cyclical, there are many factors that can contribute to shifts in market share, including consumer behavior and vehicle affordability. It’s important for auto finance sources to keep a close eye on these trends to make the right decisions and help car shoppers find affordable vehicles with the most appropriate terms — while positively impacting their portfolios.

Melinda Zabritski serves as senior director of automotive credit for Experian Automotive. Email her at melinda.zabritski@bobit.com.

More Auto Finance

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →

Permission or Approval: When to Notify Finance Sources

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Read More →

At-Risk Auto Borrowers Drive Looser Credit Access

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Read More →

Auto Loan Forecast Bucks Market Trend

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Read More →