F&I Showroom Magazine

Loading data...

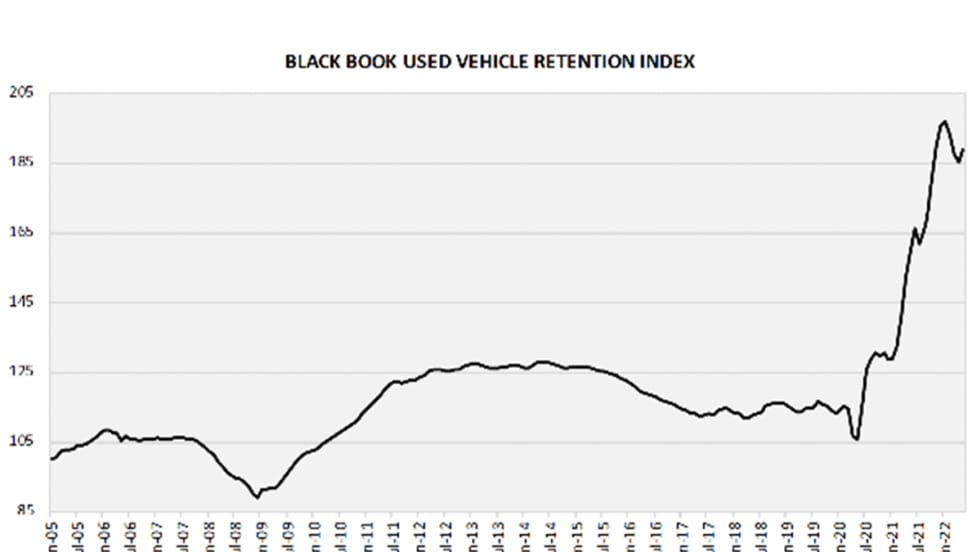

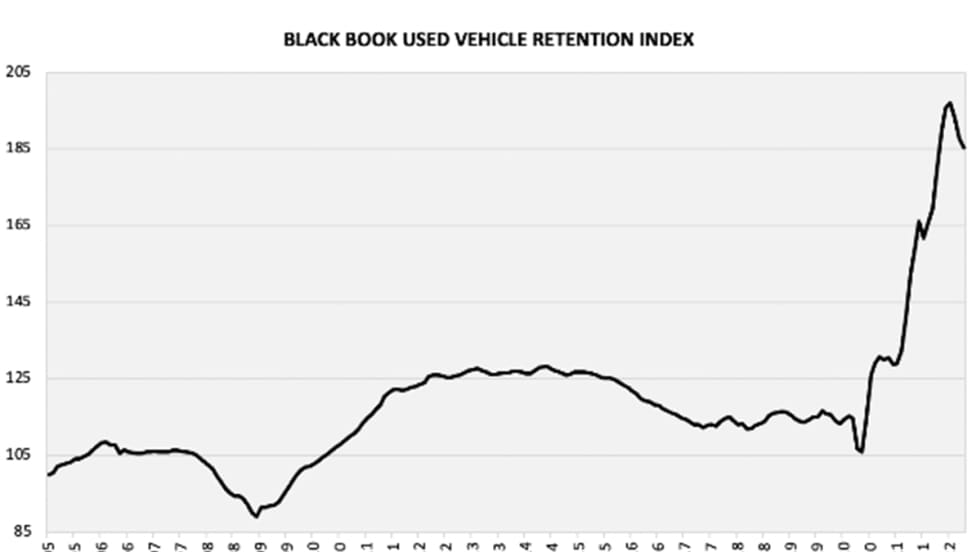

Index reverses a 3-month slide and increases to 188.8 points in May 2022 as tight new inventory and record low incentives push used wholesale prices up across most segments.

Read More →

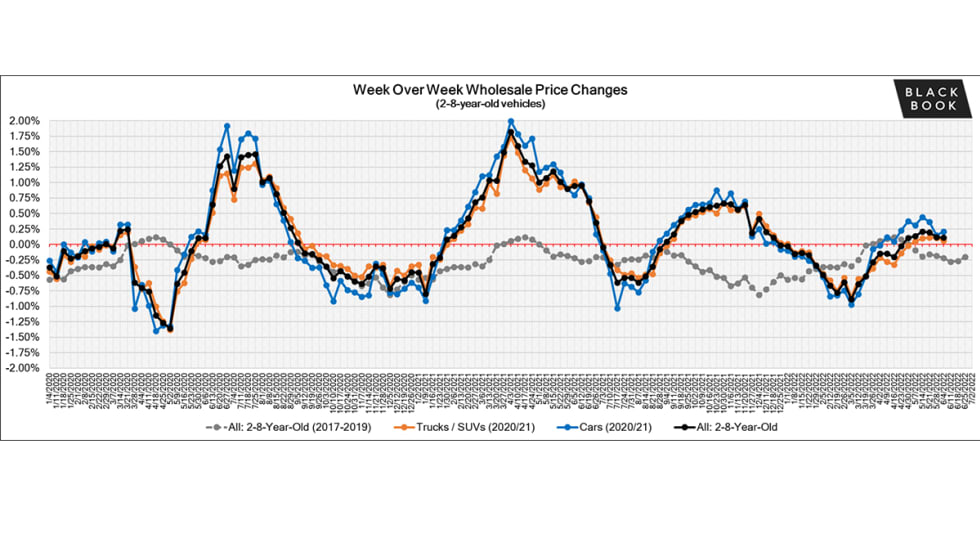

The overall market continued to see positive movement last week, but some of the segments that have been catching our eye in recent weeks for their pricing movements are now doing so for different reasons.

Read More →

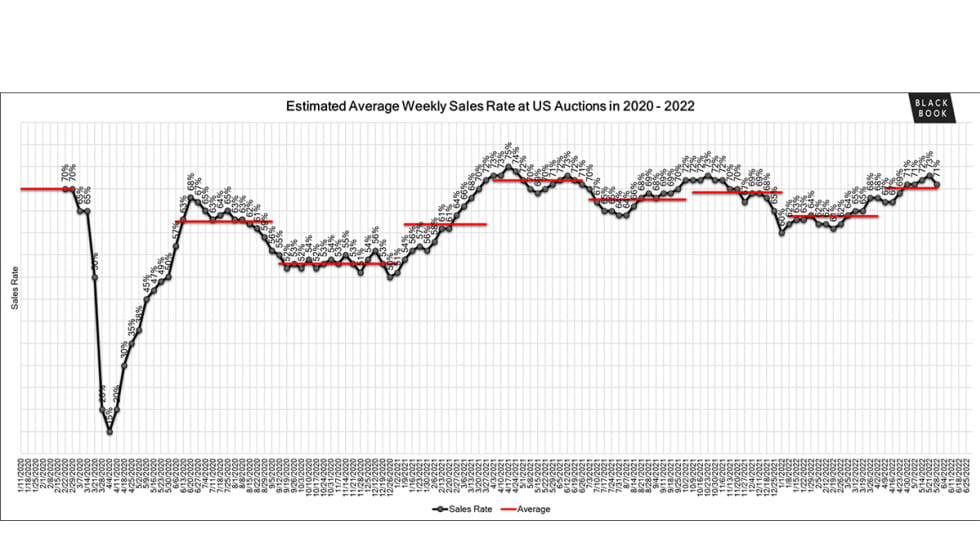

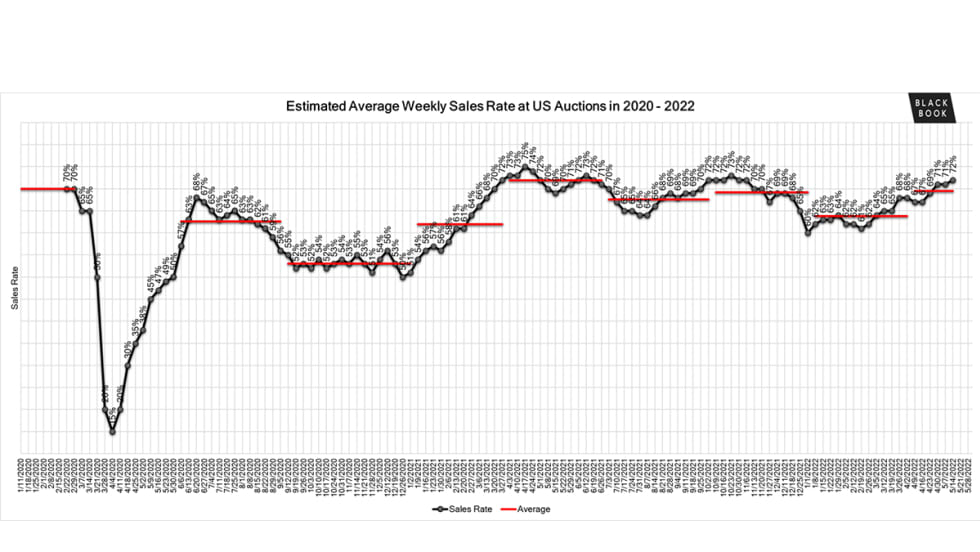

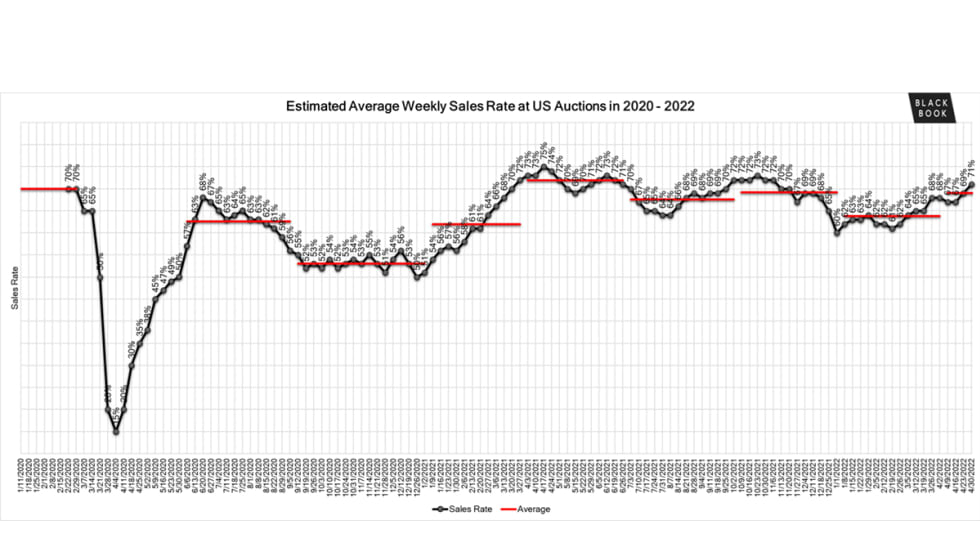

The Estimated Average Weekly Sales Rate has dropped down to 71% after several weeks of increases.

Read More →

The overall market continued to experience increases last week, with the more fuel-efficient segments reporting some of the largest gains.

Read More →

The Estimated Average Weekly Sales Rate continues to increase and now is at 72%.

Read More →

Historically, the first week of May is an exciting time for new model year launches and an increase of lease returns in the auction lanes. This year, like the past 2 years, has been plagued with microchip shortages and supply chain issues causing a significant reduction in both new inventory production and used lease and fleet returns in the wholesale market.

Read More →

The seasonally adjusted Retention Index went down to 185.4 points in April 2022 as high gas prices strengthen some segments and weaken others.

Read More →

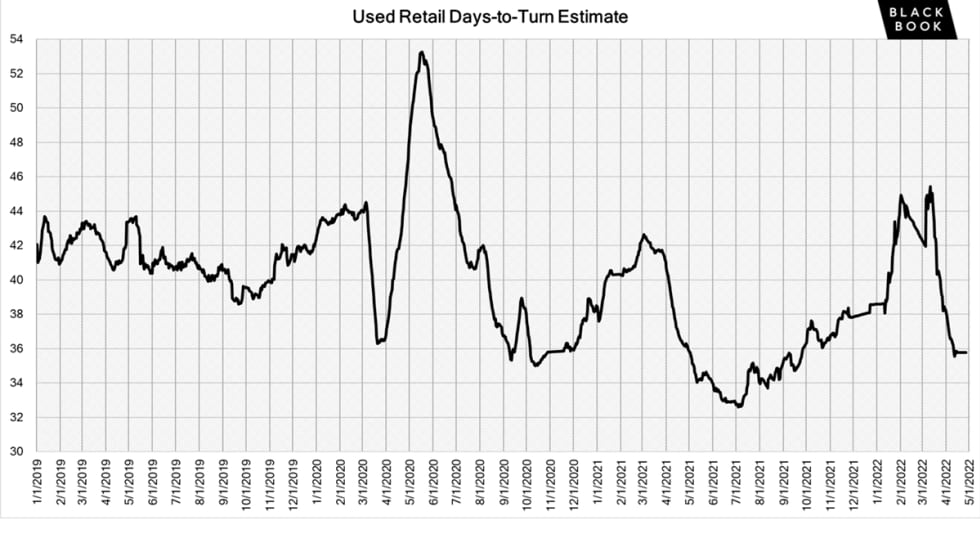

The Used Retail Days-to-Turn Estimate has continued to drop over the last few weeks and remains below 36 days.

Read More →

The car market continued its ascent last week, with the rate of gain accelerating to 0.23%, larger than the typical increase for this time of year.

Read More →

The big picture has not changed much from last month to now; overall prices are increasing, but by much smaller amounts than we have seen since the pandemic began a little over two years ago.

Read More →