There were plenty of new innovations on display in and around NADA 2017. The editor takes you on a tour of five new tech tools aiming to help dealers land more sales and F&I opportunities.

Three shows, miles of walking and Uber rides, and more than a dozen appointments to see the industry’s latest dealer solutions left me with this conclusion: It’s not the ecommerce reality these digital retailing platforms aim to deliver that makes them noteworthy; it’s the small innovations embedded in these digital roads to the sale.

Shop, desk the deal, value the trade, apply for financing, and maybe select a few F&I products. That appears to be the blueprint for those competing in this burgeoning digital retailing category. The way those steps connect, however, reveals the true differences between the various systems.

Ad Loading...

But something else was revealed during my stops at various hotel suites and booths on the show floor of the National Automobile Dealers Association’s 2017 convention, held inside the New Orleans Morial Convention Center this past January. The focus on digital retailing has opened up opportunities for solution makers outside that burgeoning category to find their place in that digital ecosystem.

My week began on Jan. 25 with the auto finance industry’s Vehicle Finance Conference and concluded on Jan. 29, the last day of NADA 2017. While this report doesn’t capture every innovation I saw along the way, it does offer a glimpse at tools that spoke to what was a top-of-mind topic.

DIGITAL RETAILING: WEBBUY

DATE OF VISIT: JAN. 26

WHERE: J.W. MARRIOTT

NADA 2017 marked the return of former F&I and financial services executive Tom Murray. He disappeared from the industry in 2012, about three years after serving as a keynote speaker at Industry Summit 2009. During that address, he talked about the need for dealers to use the Great Recession to rethink their operations, pointing to inventory and retail strategies employed by Amazon and Walmart as models to consider.

Founded by former F&I exec Tom Murray and dealer Steve Zabawa, WebBuy is the newest addition to the burgeoning digital retailing category. Murray describes it as a ‘360-degree solution with an Amazon-like checkout.’ It was in pilot for 15 months prior to NADA 2017 at Zabawa’s Billings, Mont.-based Rimrock Auto Group.

The former exec said his disappearance was intentional, as he connected with industry friend and 30-year dealer Steve Zabawa on a project that, after 24 months of research and development, officially kicked off in 2014. The goal was to build a “dealer-centric, 360-degree solution with an Amazon-like checkout.”

“We intentionally flew under the radar,” he said. “We’re rolling it out now because it’s highly functional and will forever change the retail landscape.”

Ad Loading...

The company was formed in 2014 under the WebBuy name, and the solution was in pilot for 15 months prior to NADA 2017 at Zabawa’s six-store, Billings, Mont.-based Rimrock Auto Group. “Our solution is geared for the internet department or BDC to not only improve conversion rates on web inquiries, but allow them to finally facilitate a true 360-degree online sale,” Murray said. “It’s also a lead-generation tool designed to convert more people who don’t complete the checkout process.”

The kicker is the system is free to dealers and consumers. And as Murray also noted, WebBuy is designed to make the dealer’s site “sticky,” even if the customer doesn’t engage its digital retailing process.

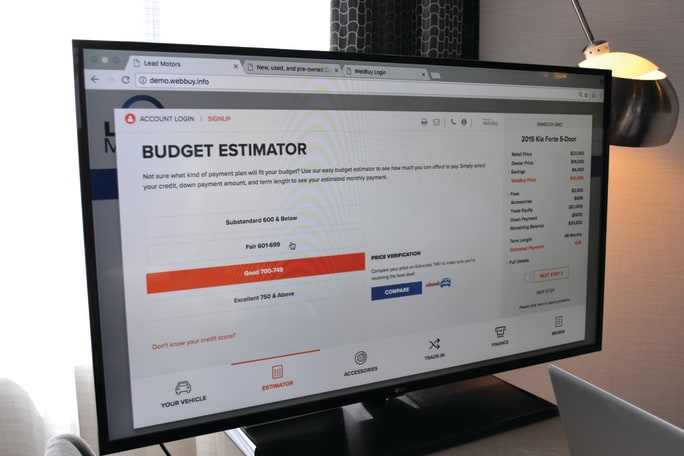

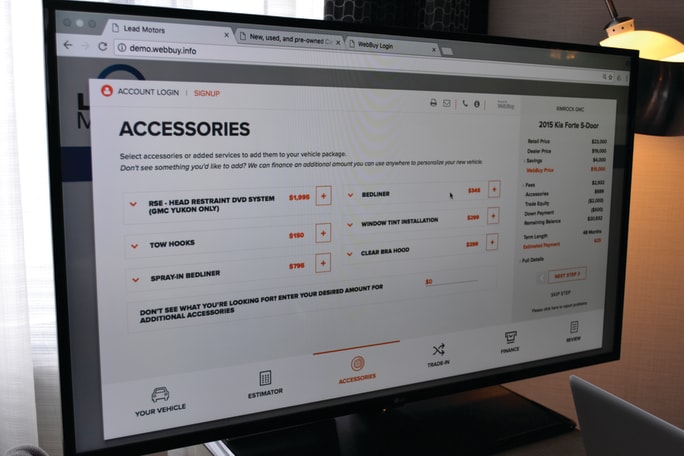

The “Buy Online with WebBuy” button is one such example. Buyers must enter their email and phone number before engaging in the WebBuy process. They must do the same to save vehicle searches and receive price alerts.

Clicking on the buy-now button initiates a five-step process that begins with a listing of available incentives, followed by a page that allows buyers to add vehicle accessories. Customers are then asked to enter their trade-in’s VIN and mileage to engage the company’s proprietary vehicle appraisal software. It poses up to 20 questions — which dealers can customized based on their specific inventory needs — about the condition of the customer’s trade-in.

The finance section opens by allowing buyers to adjust down payment, then asks for their consent to esign documents and disclosure statements. The system then moves to the credit application process, which is broken up into three sections: general, address, and employment information. Once the app is submitted, a real-time decisioning system delivers up to five lender-approved finance offers with rebates, incentives, tax, title and license included.

Ad Loading...

The system then collects a deposit from the customer to reserve the vehicle and sets the buyer’s delivery appointment. As for compliance, Murray is confident that WebBuy virtually eliminates any future liability from regulators like the CFPB, noting that the solution removes the potential for discrimination and is compliant in 50 states.. “It’s important for people to understand that, when online retailing becomes a reality, it will still only comprise a small percentage of the marketplace,” Murray said. “… Our solution is designed by car people for car people, and I’m confident that, with our solution, anyone being compensated by variable gross profit will likely be very pleased. More importantly, they’ll see improvements in CSI due to the immediate and dramatic time efficiencies WebBuy will deliver.

“If I’m an F&I manager and someone told me that half of the people backed up 10 deep on a Saturday waiting for a delivery completed 90% of the paperwork before they arrived, including hanging their own paper — and I’m likely to get a raise in the process — I’d be thrilled.”

DIGITAL RETAILING: PRECISE PRICE

DATE OF VISIT: JAN. 27

WHERE: NADA SHOW FLOOR

Precise Price represents DealerSocket’s entrance into the digital retailing arena. The new “module” connects to the firm’s legacy CRM, website builder, and desking solution tools, but consumers can engage the system without making a commitment.

The latter point is the result of Precise Price’s “Save and Finish Later” functionality, which generates a personal URL customers can use to access saved searches and configured deals. And they can do so without ever giving up their personal data. But once they’re ready to engage the dealership, the URL connects what they did online to the dealership’s showroom process.

DealerSocket’s Precise Price digital retailing platform features ‘Save and Finish Later.’ It generates a personal URL customers can use to access saved searches and configured deals without giving up their personal data. Standing with DealerSocket founder Brad Perry is Jennifer Lee, the firm’s vice president of product development.

“So, today, consumers go online and they go to the dealer’s website, and sometimes there might be a payment calculator, or there might be another digital retailing solution that allows them to put together some parts of the deal. They might be able to add a trade or they might be able to put money down,” said Jennifer Lee, DealerSocket’s vice president of product development. “With our solution, we can do the full end-to-end deal.”

Ad Loading...

By that she means car buyers can dial in their deal by incorporating every possible price influencer, including dealer incentives and fees, state and local taxes, trade-in valuation, and F&I products. Lee noted that business development center staffers and salespeople can use Precise Price to work deals with phone-in customers. They can then email or text the URL to the buyer to review the deal.

As for F&I, the link between Precise Price and DealerSocket’s desking tool means the dealer’s finance sources and product providers are already connected to the platform.

“So it allows the consumer to get familiar with finance products ahead of coming to the dealer, which they don’t do today, right?” Lee said. “Usually, the consumer is too tired to go through some of the F&I process and there’s a lost opportunity. So bringing that forward in our process for the dealer gives them a better opportunity to sell the right products on the right car to the right person.”

The solution was piloted at a handful of dealerships through the holidays. Lee said some of the early results were higher lead-to-show and show-to-close percentages.

“What we are finding is that shoppers are showing up with their mobile device and pulling up their deal and continuing the conversation in the showroom,” she said, noting the company also discovered that consumers tend to be more truthful about their credit situation when engaging Precise Price’s credit application process.

Ad Loading...

“The main feedback we’re getting from the shopper is they understand the process better,” she added. “They were more comfortable.”

Lee stressed that Precise Promise is dealer-branded. This distinction is important, she said, because most of DealerSocket’s customers have already made significant strides in making their CRM and showroom process more efficient and customer-friendly. Precise Promise, she added, represents a way to extend that into the digital space.

The pilot revealed one other thing. “What we found is that, since we’re pushing deals and not leads, we’re actually pushing more business to the dealerships,” Lee said. “So they’re getting better customers coming through the door looking to test-drive cars and close deals. So we’re increasing the throughput and making the dealership busier. It’s just a different process.”

DIGITAL MARKETING: ONECLICK LOYALTY

DATE OF VISIT: JAN. 28

WHERE: COURTYARD BY MARRIOT

In the auto finance arena, ChannelNet’s work in marketing automation for finance sources like BMW Financial Services, Volkswagen Credit, Audi Financial Services, Hyundai Motor Finance, Kia Motor Finance, and Southeast Toyota is well-known. Now it’s bringing its more than 30 years of digital marketing experience to the dealer arena.

The firm is doing so behind a marketing and loyalty solution called OneClick Loyalty. It’s built on the company’s SiteBuilder software, a patented sales and marketing platform that builds what the company calls “personalized” URLs, or PURLs. They were featured in F&I and Showroom’s April 2014 issue. Captives use them to stay connected to borrowers through the life of their loan. Company founder and CEO Paula Tompkins referred to this as “targeted lifecycle communications.”

Ad Loading...

“We start where most CRMs drop off,” she said. “We do it with personalization. We do it with turnkey support.”

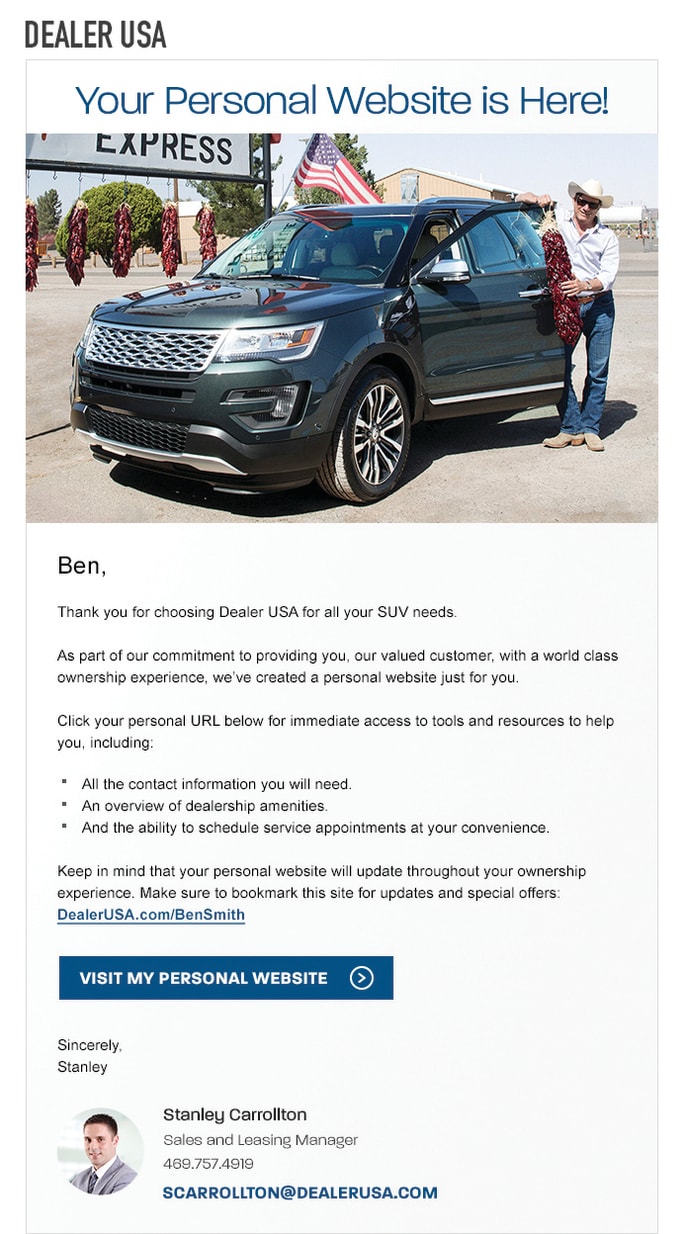

ChannelNet’s OneClick Loyalty app is a marketing communications platform. At the dealership, salespeople use the app to take photos of buyers in front of their vehicles. The platform immediately triggers a welcome email that drives customers to their very own personal website, which they can use to access dealership services and manage their auto loan, among other things. The dealership can then communicate service and sales specials through the personal website.

Here’s how it works: When a customer takes delivery of their new car, the salesperson or delivery specialist asks for the buyer’s email. Using his or her mobile phone, the salesperson enters the email and scans the VIN into the OneClick Loyalty app. They then use the app to photograph the customer in front of the vehicle.

“Now it’s going to generate an automatic email containing a link to the customer’s own personal website with their picture on it,” Tompkins noted. “It’ll have links to social media so they can share the photo with their friends and relatives.”

The social media connection isn’t the main feature, however; it’s the connection the app forges. From their PURL, customers can set service appointments, get access to service specials, and check vehicle incentives and inventory. They can also manage their loans and read about the F&I products they elected against. Tompkins added that dealers can even link the PURL to their digital retailing system or embed it into OneClick Loyalty.

“So this little mobile app goes with the system,” Tompkins said. “And then we work with the dealer’s general manager or whomever to say, ‘Look, get your sales guys to use this, because we really want to push the message out that the customer’s excited about the new car.’”

Ad Loading...

Heading up the company’s move into the dealer arena is K.C. Loughlin, who was named vice president of dealer sales and services this past January. His 30-year career includes leadership roles in used-car sales and fixed ops, as well as stints with Dealertrack and, most recently, DealerSocket.

Loughlin said the personal websites can be dressed up however the dealer wants, meaning they can showcase their quick lube lanes, play areas, massage chairs and coffee stations. “All those things that dealers like to provide, if the dealer wants that in that personal URL for the customer, we put it in there,” he said.

What Loughlin thinks will really pique dealer interest is the app’s concierge marketing service. ChannelNet’s new executive said dealers will be able to call the company’s concierge helpdesk and have an entire marketing campaign turned around within 48 hours. They can use it to promote service and sell cars. F&I offices can also use the service to reengage buyers who opted against a service contract before their warranty expires.

“So the dealer will be able to call our concierge helpdesk and say, ‘It’s ACME Chevrolet, and what I want to do is take my last five years’ worth of my old body style Chevrolet Malibu customers. And I’ve got 75 brand-new body style, fully upgraded Malibus on the lot, and I want to send the program out to those particular customers,” he said. “And we’re committing to our dealers that, within 48 hours, we’ll have that program put together, and all that content goes back out in the personal website.”

ONLINE F&I: DARWIN AUTOMOTIVE

DATE OF VISIT: JAN. 28

WHERE: NADA SHOW FLOOR

One could say the creators of Darwin Automotive are in a constant state of evolution. Fourteen years ago, they built the MenuVantage F&I menu, which is now owned by CDK Global. They were also the guys who built the service inspection tablet technology utilized by CDK and Ford Motor Co. The company’s leadership team is now prepping for its next evolution.

Ad Loading...

The Darwin F&I selling system was actually created to give Sonic’s hybrid managers additional F&I selling tools. The platform then morphed into a complete menu-selling system, said Chief Marketing Officer Jeff Stafford, with its initial entrance into the F&I space beginning in partnership with several major F&I agencies and providers, including JM&A and American Financial & Automotive Services.

“That’s how Darwin really got its start. It wasn’t the traditional F&I approach, but it works really, really well for people who employ the one touch model, as it guides them through the process,” he said. “They’re not seasoned F&I managers, so this helps by highlighting the Top 3 products.”

Darwin Automotive’s Jeff Stafford is seen here demonstrating the company’s F&I selling system during NADA 2017. It was then that the firm’s chief marketing officer revealed to ‘F&I and Showroom’ magazine the company’s plans to enter the digital retailing space behind its F&I selling tool, which was rolled out less than two years ago.

The system uses a combination of algorithms to analyze in real time the customer’s answers to a set of needs-discovery questions, deal information, previous ownership history and any other details stored in the dealership’s DMS. Then, through predictive analytics, it produces what the company refers to as a “Driver’s Needs Analysis,” which scores F&I products based on the buyer’s need and the likelihood the customer will purchase those protections.

The analytics also contain the customer’s prior ownership history, information on the vehicle’s warranty, and what the company refers to as Deal Factors. The latter are simply a list of reasons why the customer will need the product, which the producer can use to respond to questions or objections. Once the producer reviews the report, a presentation menu is created. It can be printed out or displayed on a smartphone, tablet, touchscreen, or desktop display.

The system presents the top products — all ranked accordingly — in one, two or even the traditional four-column configuration. Buyers can then drag-and-drop products in and out of each column. What makes prescriptive selling effective, Stafford said, is that buyers view the products listed in the main column as truly tied to their needs. He recalled the first time an early adopter tested it out. It was a cash deal on a $23,000 Ford Transit, and the customer laid down for the Top 3 products the system listed.

Ad Loading...

“The finance manager says, ‘That’s never happened to me before: $6,000 worth of product on a $23,000 cash deal,’” Stafford recalled. “But the iPad has no preconceived notions, so it recommends the Top 3 options. It’s a different psychology, especially coming from MenuVantage, where we supported the static column presentation.”

Stafford noted that the Darwin system, which also handles compliance disclosures, can connect to customers taking delivery offsite via their phone, tablet or computer, a feature designed to address today’s internet shoppers. But the company has bigger plans for its F&I selling system. It’s called Darwin Online.

“It’s basically a multitude of widgets that a dealership can embed in its website,” Stafford explained. “Customers are gonna do things on their own terms. They’ve already shown that. And in order to defend F&I revenue, you have to be present there.”

The revelation makes the company’s announced alliances with DMS providers CDK Global and Advent even more compelling. Although simply sales and marketing deals — CDK Global announcing it will market and sell the Darwin system as CDK MenuVantage Platinum — the announcements point to bigger things in the future. Stafford added that Darwin’s parent company, DMS integration company Superior Integrated Solutions, will also aid in the company’s future push.

“So there really is nobody better in the industry at integrating with the CDKs, Auto/Mates, Advents, and Dealertracks,” Stafford said. “We can actually get real payments if the dealer wants, because we can connect to their true taxes, fees, rates, etc.”

Ad Loading...

DIGITAL RETAILING: AUTOFI

DATE OF VISIT: JAN. 28

WHERE: RENAISSANCE ART WAREHOUSE DISTRICT

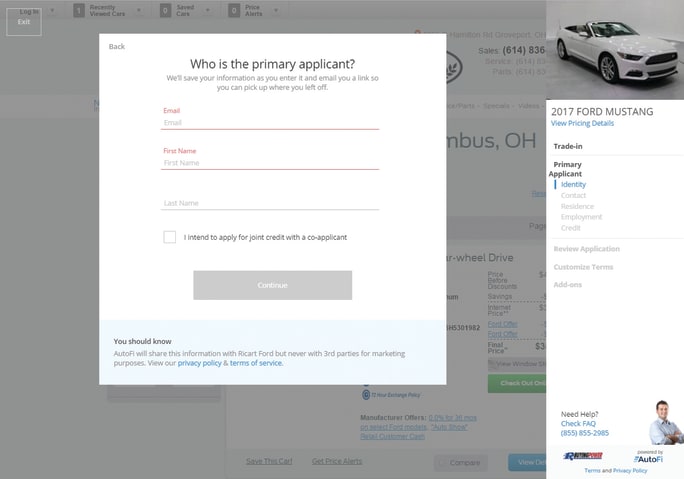

The big announcement heading into NADA 2017 was Ford Motor Credit’s investment in AutoFi, a new entrant in the digital retailing category. The startup’s founders include CEO Kevin Singerman, a former executive of SunGard Data Systems and online credit marketplace Lending Club, President Jonathan Palan, a former executive for online mortgage marketplace LendingHome, and CTO Mandar Gokhale, former product development lead for PayPal and GoDaddy.

Also on the team is Joe St. John, who joined the company last November as head of dealer success. He previously served as director of training for IAS after spending more than a decade in retail. He said much of the startup’s early funding was spent on designing the platform to interface and interact with the customer, the finance source, and the dealer. Most importantly, the system had to integrate with a dealership’s existing ecosystem.

“We’re a pipe from a consumer to a lender through the dealer,” he explained. “The dealer part is what we believe is the most important piece, because it’s the dealer’s inventory, the dealer’s website, the dealer’s CRM, and it’s the dealer’s customer and data.”

AutoFi went live on Jan. 4 at Ricart Ford in Groveport, Ohio, 24 days before officials demoed the platform for F&I and Showroom.

The system went live on Jan. 4 at Ricart Ford in Groveport, Ohio, 24 days before St. John demoed the AutoFi platform for F&I and Showroom. It was too early in the pilot to offer any real conclusions, but St. John said the declined deals were the most eye-opening.

“If we decline them, we don’t ever say, ‘Boo, you’re declined.’ We detour them back to the dealer for a manual decision,’” he said, noting that the lead and credit info gets pushed into the dealer’s CRM and credit decisioning system. Alerts are also sent to managers to pick up the baton and continue working the deal.

Ad Loading...

AutoFi first asks buyers to enter their email, a step designed to feed the dealer’s CRM. Customers are then asked if they’ll require financing. If the answer is “No,” they are rerouted into the dealership for a cash transaction.

Customer are then asked to value their trade-in and manually enter any balance owed on an existing loan. The system also provides a link to a Consumer Financial Protection Bureau web page that explains how to get a 10-day payoff quote; St. John said the payoff calculation will soon be automated.

AutoFi made a big splash heading into NADA 2017, announcing on Jan. 23 that Ford Motor Credit had invested in its digital retailing platform. Officials describe it as a pipe from a consumer to a lender through the dealer’s website, serving up actual decisions from finance sources in 10 seconds, max. The system can be loaded to a dealer’s site within two hours of signup and costs $75 per transaction.

Throughout this process, a photo of a man with his arms crossed sits at the bottom of the page. “That’s Steve the Lawyer,” St. John said. “He’s the customer advocate.”

Steve answers FAQs about financing, compliance and F&I products. And when the system spits out the customer’s net trade amount, Steve explains the quote is dependent on an inspection at the time of delivery.

The credit application process is broken into five steps. Customers can complete it manually or log into their bank accounts to prefill the app and, with some banks, verify proof of residence and income. They can also use their smartphone to photograph their driver’s license, and subprime customers can upload required stips.

Ad Loading...

“For some lenders, all the customer has to type in is birthday, income and Social,” St. John noted. AutoFi then presents the compliance disclosures, which the firm spent “considerable resources and time on to ensure its digital transactions are compliant.” Dealers can then submit credit apps directly to finance sources or through RouteOne or iLendingDIRECT. “So a customer hits submit and now I’m going to verify their identity, check their credit, check their income, calculate their APR and give them actual decisions from the lender,” St. John explained. “These decisions take about 10 seconds, max.”

St. John added that every data point associated with those offers is dynamic, meaning that the interest rate changes or offers drop off automatically as the customer adjusts term or down payment. Once the customer accepts an offer, the system provides a deal review before launching into the F&I product presentation.

St. John said AutoFi is working to integrate directly with F&I product providers to erate and econtract products and develop customizable marketing content to support sales within the platform.

The digital process concludes by allowing customers to set up their auto payment, and document signing is handled electronically within the system. The entire AutoFi system can be loaded to a dealer’s site within two hours of signup. Cost to participate is $75 per transaction.

There’s one other feature that speaks to the concerns F&I managers may have about the Digital Age: AutoFi allows the producers to rewind the entire process at the time of delivery. St. John says that creates a second opportunity at closing an F&I product sale. “It’s a first pencil with all the contracts done, so you can rewind right back to that part, select the products and then re-sign.”

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.