People don’t fear being sold during times of economic prosperity, because spending a little extra money isn’t a big deal when you have more than enough. But most people today have less disposable income, so they will work hard to make what they perceive to be the most dollar-saving decision possible. For some, the word “No” means a lower payment coupon. In order to get them to buy F&I products, we must learn to intelligently relate them to saving money.

Many people don’t realize exactly how much has changed in the last 25 years. Household income is stagnant, but the cost of goods and services keep trending upward. This presents more need than ever for customers to protect their budgets.

Ad Loading...

Our economics aren't the only thing that's different. Transactions and information availability have changed as well. Most importantly, the cavalier attitude people had when it came to their money is gone, as today’s customer has no choice but to spend wisely or risk having a poor quality of life.

The Free Money Years

From 1993 to 2008, Americans had more disposable income and the cost of living was better balanced with average household income. Times were good. Housing values were on the rise, allowing people to borrow more money against their homes with little or no concern about paying it back. It was like the money was “free.” Of course, it wasn’t.

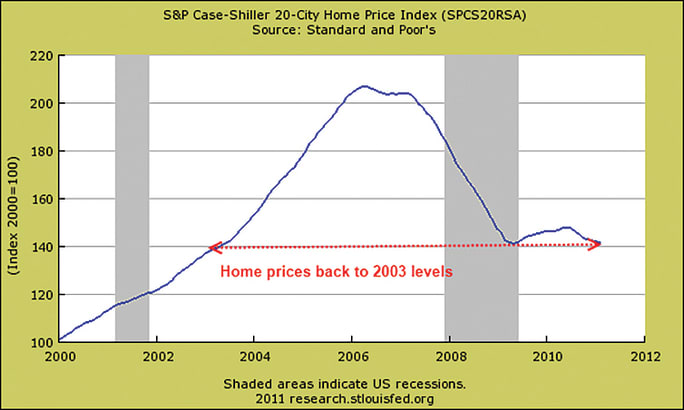

Home values had doubled over the eight-year period preceding the housing crash of 2008.

See, the “free” money idea came from the basic belief that you could buy a house, borrow more than the value, and later sell it for a high price to pay off the loan. Essentially, they were diverting potential real estate earnings toward purchases that were outside their actual budget. And since it wasn’t coming out of their budget, the money felt “free.”

And this free money paid for lots of things, from vacations and pools to elective surgeries and house remodels. This free money even led to a resurgence of Harley-Davidson. Of course, we also saw lots of cash-paying car buyers visiting our dealerships.

Needless to say, money came very easy the more home values rose. And bigger houses meant bigger advances. Borrowing 125% of your home’s value was normal by 1995, and it continued at a record pace until 2008. Even more astonishingly, home values doubled from 2000 to 2008. People didn’t worry at first, even though it was clear the situation was unsustainable. Well, the “bubble” popped in 2008, when housing values plummeted back to early-2000s levels.

Ad Loading...

Caught in the Cycle

From 2008 to 2011, almost everyone struggled. The automotive industry was no exception, as many dealers didn’t survive. While adjusting to the new economy, F&I managers began telling me that word-tracks were suddenly uncomfortable to use. Even worse, producers who continued employing them were having limited success.

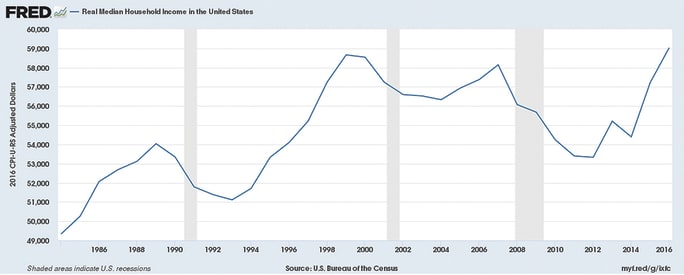

The average median household income between 1993 and 1999 grew by about 15% to $58,665, where it peaked and remained stagnant until 2012. Income, as the graph above shows, is now trending upward, but it remains well below where it should be in relation to advances in automotive inflation.

These revelations forced me to take a hard look at F&I in this new environment. I began taking F&I benchmarking assignments in distinctively different environments and measured my own numbers. The enjoyment of working inside the dealership with customers again didn’t hurt my spirits, either.

I quickly discovered the F&I training I received in the early ’90s and all the closes I had taught hundreds of F&I managers as a full-time F&I trainer had become a thing of the past. So rather than presenting and trying to overcome objections, I began having conversations with my customers. I also began viewing F&I products as ways to protect my customers’ budgets instead of just ways to make gross. Yes, the gross was still there, but my attitude was completely different. My product count went way up, and my chargebacks went way down.

By not selling, I sold a lot more. Today, I understand why.

See, for the first time, I was focused on helping people, not selling people. The difference is paramount. I didn’t apply the 300% rule. Instead, I listened to and shared with people. I also kept my process transparent. I ran the highest numbers I ever had. In fact, I outperformed the existing F&I departments in every store I worked in.

Ad Loading...

From Prosperity to Austerity

In 1993, you could buy a base model F-150 for $10,877. Today, a base F-150 has an MSRP of $28,770. That’s a 264% increase over the last 25 years. Talk about inflation, right? Well, according to recent reports from Kelley Blue Book, it’s still trending upward.

Wages, on the other hand, have barely changed.

The average median household income between 1993 and 1999 grew by about 15% to $58,665, where it peaked and remained stagnant until 2012. Income is now trending upward, but it remains well below where it should be relative to advances in automotive inflation. And no relief is in sight. Because when wages rise, the stock market falls, as corporations recognize that higher wages mean lower profits. So prices must go up again and the cycle continues.

Economic prosperity is gone for most Americans, with wages down and inflation up for a long time now. That means people are focused on not getting sold, even when products like vehicle service contracts, prepaid maintenance, and GAP are designed to help them save money and provide budget control.

Living Check to Check

As a culture, Americans live check to check. In fact, 78% of your friends, family, and co-workers live check to check.

Recently, the CEO of a publicly traded auto finance source shared that many of the company’s customers have less than $400 in emergency savings. And it’s not just subprime, it’s everyone — even customers shopping in highline stores.

Ad Loading...

getty images/ Evgeniy Shkolenko

I’m sure many of you F&I pros can relate, as there isn’t a week that goes by that I don’t hear, “I need to make at least $12,000 a month or it’s not worth getting out of bed.”

The truth is that most people spend every dollar they make. It’s not a criticism; it’s a fact backed by data. And it’s not necessarily a bad thing.

In fact, the reason for living check to check is usually noble. People love their families and tend to invest in them. They live in nicer neighborhoods, drive nicer and safer cars, eat better foods, send their children to better schools, enjoy family vacations, and improve their quality of life — even when money is tight.

That said, money will become tighter if trends continue. Kelley Blue Book reported in December 2017 that new-car prices reached an all-time high. As if higher prices weren’t enough, it is likely that interest rates will also continue to rise. The end result will inevitably be more customers arguing over payments.

A Noble Pursuit

When we adopt habits of helping, not just selling people, we can begin having real conversations about real economics and how our products actually protect their budgets. This is more important than ever because the likelihood of continued inflation is high and our customers need F&I managers operating with a spirit of nobility.

Beyond our customers, we need to do it for ourselves, too. If the experience in F&I doesn’t improve for our customers, dealers will continue to search for ways around the F&I department. But fear not, friends, as we are all looking for the same thing: a solution that meets the needs of your customer, your dealership, and your wallet.

Ad Loading...

Customers need to feel protected and treated well. The dealer needs to profit. If both sides get what they want and need, you, the F&I pro, will be fairly compensated for your efforts.

Lloyd Trushel is a 28-year veteran of the automotive business and co-founder of the Consator Group, an F&I development company specializing in customized training solutions. Contact him at lloyd.trushel@bobit.com.

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.