Rising Loan Amounts Drive Consumers to the Used-Vehicle Market

The auto finance segment is growing at a healthy rate, but average new-vehicle loan amounts are outpacing the market, driving an increasing number of car buyers — including those with prime and superprime credit scores — out of the showroom and onto the used-car lot.

Auto finance sources reported healthy growth in the first quarter, but a closer look reveals a worrisome trend.

Illustration by Svetlana Borovkova via Getty Images

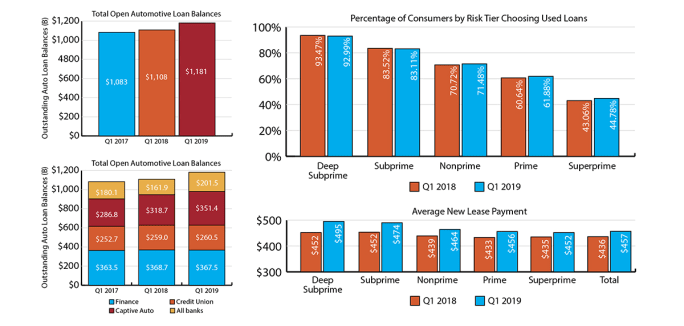

The automotive finance market has seen healthy growth over the past year, according to Experian’s most recent State of the Automotive Finance Market report. The total market balance for open automotive loans has jumped 6.5% year-over-year and reached a record-high market balance of $1.1 trillion in the first quarter of 2019.

Nearly every category of automotive lender experienced loan balance growth from Q1 2018 to Q1 2019. Finance companies exhibited the strongest growth, increasing by 24.43% (from $161.9 billion to $201.5 billion). Credit unions also had strong growth, increasing their balances by 10.26%. Captives had the least amount of growth, adding just 0.6% to their loan balances.

While banks still held the majority of loans, they experienced a 0.35% decline from $368.7 billion in Q1 2018 to $367.5 in Q1 2019. This is the second consecutive quarter banks have had a slight drop in their total loan balances.

Credit scores for new and used purchase and lease customers were stable year-over-year, but the percentage of prime and superprime car buyers buying used grew to 61.9% and 44.8% in the first quarter.

Photo by Creatas Images via Getty Images

In With the Old, Out With the New (Cars)

Vehicle affordability continues to be a hot topic within the automotive industry, which is only furthered by average vehicle loans reaching new highs: The average loan amount for a new vehicle hit $32,187 in Q1 2019, up $733 from last year. When coupled with the slight decrease seen in new loan terms to 68.85 months, the average new-vehicle payment reached $554.

Consumers are adapting to the new high-payment environment by exploring and utilizing all options available to them. Most notably, prime and superprime consumers are shifting into the used-vehicle space at a high pace.

The percentage of prime and superprime consumers choosing used vehicles reached 61.88% and 44.78%, respectively.

Lease Payments Up, Terms Remain Stable

Leasing continues to be another alternative for a smaller monthly payment, with the average difference between a lease and loan payment clocking in at $97.

Overall, leasing of new vehicles saw a slight decrease, from 29.83% in Q1 2018 to 29.07% in Q1 2019, but used leasing saw a slight uptick, from 4.01% to 4.68%.

Average lease payments rose $18 between this year and last, from $436 to $457. All categories saw a rise in lease payments, with deep subprime increasing the most (by $43). However, average lease terms have not risen with payment amounts and remain at 36 months.

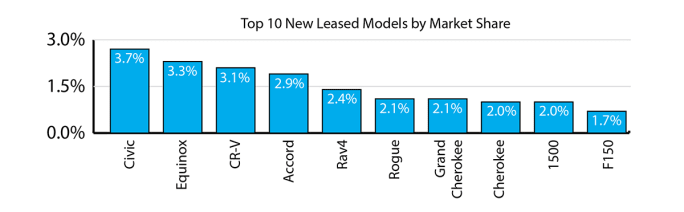

This rise in average lease payments is primarily driven by consumers’ vehicle preferences shifting from smaller cars to larger ones, in particular crossover vehicle models. Bigger cars typically mean bigger prices, and they now comprise the majority of the top leased vehicle models.

30-Day Delinquencies Increase, Remain Below Recession-Era Rates

Q1 2019 saw 30-day delinquencies increase to 1.98%, up from 1.90% in Q1 2018. However, banks, credit unions, and finance companies all saw slight decreases in 30-day delinquency rates.

Additionally, 60-day delinquencies remained relatively stable at 0.68% year-over-year.

Even with a slight uptick in 30-day delinquencies, lenders should keep in mind the larger historical context of these trends. For example, the 30-day delinquency rate is still well below the high mark in Q1 2009, which was 2.81%.

Auto Loan Credit Scores Remain Largely Unchanged

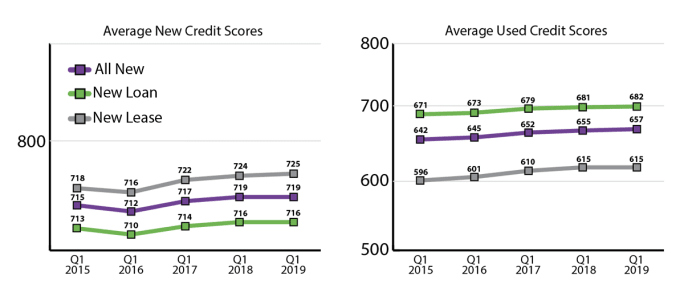

Q1 2019 showed growth for average credit scores for used auto loans. All used lending saw the average score increase two points to 657. Meanwhile, franchise used credit scores are up one point to 682 while independent used remained 615.

Average new credit scores experienced less change overall. While new lease scores saw a one-point increase to 725, all new-vehicle credit scores remained consistent with last year’s score of 719 and credit scores for new loans maintained at 716.

A Stable Credit Market Combined With Rising Vehicle Costs

This past year has brought the highest level of lending volume to date, and the automotive finance market continues to display healthy growth. Shifts in consumer behavior indicate they’re already beginning to act on higher vehicle prices, and more choose to drive used vehicles.

With new, innovative technology and product offerings being developed daily, it’s clear that the automotive industry is evolving at a breakneck pace. It will be important for finance sources, dealers, and manufacturers to continue monitoring these trends so they can provide consumers with the best vehicle financing options available.

Melinda Zabritski serves as senior director of automotive financial solutions for Experian Automotive. Email her at melinda.zabritski@bobit.com.

More Auto Finance

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →