Automotive Finance Industry Shows Consistency in Q4 2020 Despite Disruptions

Overall, the automotive finance market has remained resilient, despite the pandemic. Staying close to the data will help lenders ensure they have the right options available to fit consumers’ needs and budgets.

Overall, the automotive finance market has remained resilient, despite the pandemic. Staying close to the data will help lenders ensure they have the right options available to fit consumers’ needs and budgets.

IMAGE: MHJ via GettyImages.com

As 2020 came to an end, all eyes were on the automotive market. Some industry pundits and economists view the automotive landscape as a barometer of recovery from COVID-19. And overall, the industry continued to move ahead, with open automotive loan balances growing 2.8% from Q4 2019 to Q4 2020, reaching $1.2 trillion.

Staying close to the data will help lenders understand the state of the market and ensure they have the right options available to fit consumers’ needs and budgets.

This is especially significant when you consider that the volume of vehicle registrations declined in 2020. New vehicle registrations saw a 15.5% drop from 2019 from 16.8 million to 14.2 million in 2020. Used vehicles also saw a decrease, though not as drastic: there were 39.3 million used vehicle registrations in 2020, which was a 7.5% decline from the 42.5 million registered in 2019.

But even with the industry’s rebound, there are still many unknowns in the days and months ahead. As a result, it’s more vital than ever for lenders to stay close to the trends to make more strategic decisions for the future.

Q4 2020 data shows a lot of consistency within the automotive finance space, despite some minor shifts to trends as a result of COVID-19. Some of those disruptions include prime consumers financing new vehicles in increasing volumes and an overall reduction in leasing. Aside from that, things were fairly consistent, with trends such as increasing average loan amounts, monthly payments, and loan terms continuing. Below is a closer look at each of these trends, and some key considerations to keep in mind as we navigate 2021.

Prime Consumers Shift Back to New Vehicles

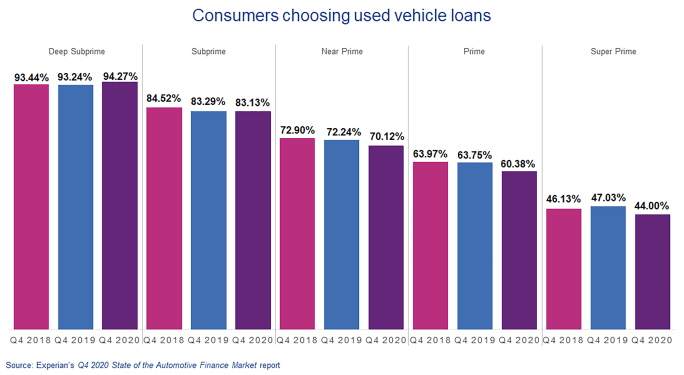

Prior to COVID-19, prime consumers began to finance used vehicles in higher volumes, which was likely driven by affordability concerns and the availability of late-model used vehicles. COVID-19 disrupted that pattern. Approximately, 44% of super prime consumers financed used vehicles in Q4 2020, down from 47.03% in Q4 2019. Similarly, 60.38% of prime consumers financed used vehicles, down from 63.75% in the same time frame.

In the early days of COVID-19, we could attribute the shift to heavy incentives offered to keep consumers purchasing vehicles, and we saw some residual effect of carryover incentives in Q4. Additionally, circumstances like inventory shortages and availability of stimulus funds played a role in making new vehicles more attractive to prime and super prime consumers. If incentives remain high in 2021, this trend could continue.

Leasing Continues to See Decline

The other notable reaction to COVID-19 was a sudden decrease in leasing, which we first saw earlier in 2020. In Q4 of 2020, 26.45% of new vehicles were leased, compared to 30.64% of new vehicles in Q4 of 2019. The drivers of this decline may be similar to those for the increase in new car financing among prime consumers: Incentives may make loans a more attractive offer than a lease. Additionally, some consumers were still unable to physically visit dealerships to trade-in their leased vehicles.

For consumers who do choose to lease, it could be one of the ways they’re looking to manage affordability concerns. On average, the difference between a monthly payment for a loan and lease is $116, as of Q4 2020. We see this most dramatically for larger vehicles, such as full-size pickups. The Chevy Silverado 1500 has an average monthly payment of $638, compared to an average lease payment of $455. But, even for other vehicles such as the Honda CR-V, which was the most commonly leased vehicle in Q4 2020, the difference is nearly $100 — the average monthly payment was $453, while the average lease payment was $367.

Average Loan Amounts and Monthly Payments Continue to Rise

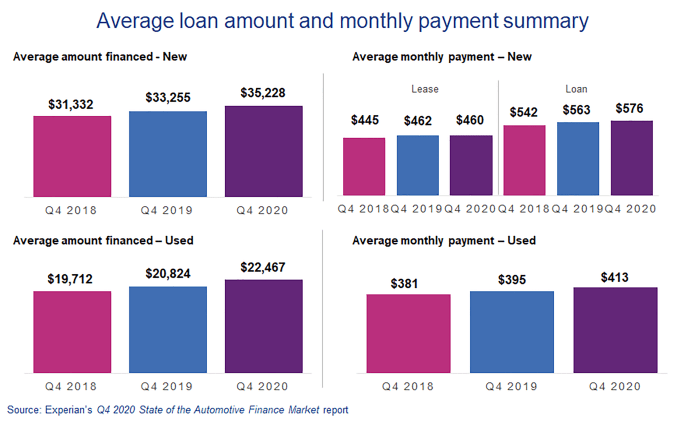

In the fourth quarter, we continued to see average loan amounts and average monthly payments for new and used vehicles continue to rise. The average loan amount for new vehicles reached $35,228 in Q4 2020, up from $33,255 in Q4 2019. A similar trend was seen for used vehicles, as the average used vehicle loan reached $22,467, up from $20,824 in the same time frame. The average monthly payment for a new vehicle increased $13 year-over-year, reaching $576, while the average monthly payment for used vehicles rose $18 year-over-year, surpassing $400 for the first time at $413.

What’s driving these increases? To better understand, let’s look at what was financed in Q4 2020. More than 50% of new vehicles financed in Q4 2020 were SUVs, followed by pickup trucks. These larger vehicles come with larger price tags, resulting in larger loan amounts. As consumers have shown a preference for larger vehicles for a number of years at this point, we’ve also seen the trend within the used market.

Loan Terms Extend While Interest Rates Lower

With higher average loan amounts and monthly payments, affordability is a common topic of conversation. Two factors that have helped keep monthly payments manageable are extending loan terms and decreasing interest rates.

Year-over-year, we continued to see slight increases in average loan terms for both new and used vehicle loans. The most common loan term for a new vehicle was 69.68 months, in Q4 2020, up from 68.84 in Q4 2019, while the average loan term for a used vehicle was 65.58 months, increasing from 64.67 months in the same time frame. Extending loan terms can help keep monthly payments lower by spreading the amount of the loan across a longer time period. However, it’s important to consider that extending terms also means that it will take longer to achieve positive equity and can result in paying more interest over the life of the loan.

Another factor that has helped keep payments manageable is decreasing interest rates. The average interest rate for a new vehicle saw a dramatic decrease year-over-year, going from 5.25% in Q4 2019 to 4.31% in Q4 2020. Average interest rates for used vehicles also dipped, though not by as much, with the average interest rate coming in at 8.43% in Q4 2020, down from 9.05% in Q4 2019.

Subprime Sees Shrinking Share of Originations

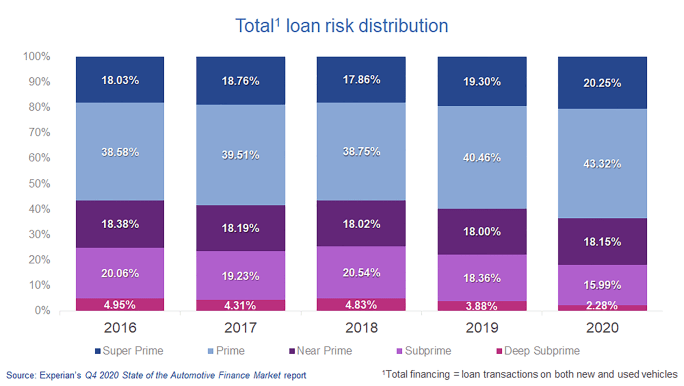

One of the other ongoing trends that pre-dates COVID-19 is the decrease of subprime and deep subprime originations. In total, subprime loans accounted for 18.27% of originations in Q4 2020, down from 22.24% in Q4 2019.

While this trend did start prior to COVID-19, it was accentuated by the pandemic with a sharper decline year-over-year. While it’s entirely possible these consumers may not be in the market for a vehicle, it’s an important trend to pay attention to, to ensure these consumers aren’t locked out of the market. Lenders should consider looking to additional data sources to layer in with traditional credit data, to gain a complete picture of creditworthiness. This data can include things such as rental payments, monthly bill payments including cell phone, utility, and others. Layering in data such as this can help lenders identify additional consumers to lend to without expanding their risk.

Overall, the automotive finance market has remained resilient, despite the pandemic. Staying close to the data will help lenders understand the state of the market and ensure they have the right options available to fit consumers’ needs and budgets. Ultimately, this will keep the industry on the rebound as we navigate 2021.

Melinda Zabritski is Experian’s senior director of automotive financial solutions.

More Auto Finance

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →