Weekly Market Insights Report

The market continues to increase, but the rate of weekly gains has slowed while still remaining at levels that would be record-setting by any historical comparisons.

The market continues to increase, but the rate of weekly gains has slowed while still remaining at levels that would be record-setting by any historical comparisons.

Wholesale Prices, Week Ending April 17th

The market continues to increase, but the rate of weekly gains has slowed while still remaining at levels that would be record-setting by any historical comparisons. Volume and quality of available units in the wholesale marketplace continue to be a challenge for buyers.

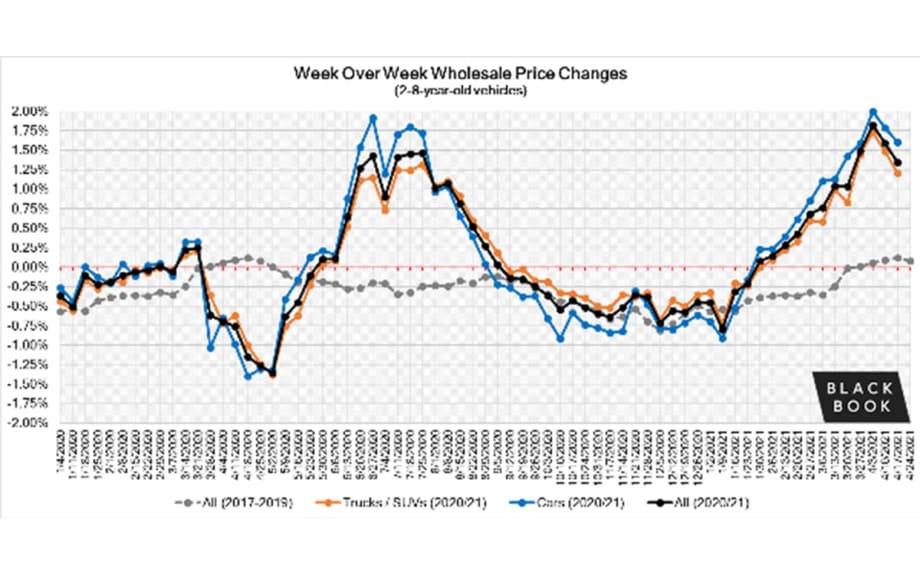

This Week Last Week 2017-2019 Average (Same Week)

Car segments +1.60% +1.78% +0.23%

Truck & SUV segments +1.20% +1.48% +0.04%

Market +1.34% +1.59% +0.12%

Car Segments

Car segments this past week, continued to have large gains (+1.60%), but the rate of increase slowed compared to the week prior (+1.79%).

Eight of the nine Car segments had another week of gains exceeding +1.00%, with Compact (+2.30%) Cars exceeding 2% for a third week in a row.

Compact Cars have had gains exceeding 2% for four out of the last five weeks.

Prestige Luxury Car (+0.72%) was the only segment to have gains below 1.00%, but by comparison, this same week in 2019 had a decline of -0.29%.

Truck Segments

Truck segment gains continued this past week (+1.48%), but it was at a lower level compared to the record setting previous week (+1.73%).

All thirteen truck segments reported gains, with seven exceeding 1.00%.

Sub-Compact Crossovers (+2.14%) had a fourth week in a row of increases exceeding 2%.

Full-Size Trucks continue to see values pushing higher with this past weeks gain growing another +1.75%, compared to +1.57% the week prior.

Minivans increased +1.83%, compared to +1.78% the week prior.

Newer Used Vehicles (0-2-year-old)

Driven by an extreme shortage of rental returns and limited inventory of new vehicles, the price trends of newer used vehicles were experiencing larger weekly gains compared to the older units. Within the last two weeks, newer used units reached levels that, in some cases, exceed new car pricing while the rate of growth has slowed for older units. For example, in addition to F150 Raptor, 2020-21 Chevrolet Corvette, and 2021 Jeep Gladiator and Wrangler, this week, dealers had to pay above the MSRP for 2021 Kia Telluride and Hyundai Palisade.

The table below shows the average weekly price changes for 0-2-year-old vehicles.

This Week Last Week 2017-2019 Average (Same Week)

Car segments +1.28% +1.54% +0.23%

Truck & SUV segments +0.98% +1.37% +0.09%

Market +1.07% +1.42% +0.12%

Weekly Wholesale Index

2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g. 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. It appears that 2021 will not have typical seasonality patterns. The spring market arrived about 7 weeks earlier and with much stronger price increases compared to a typical pre-COVID year. The graph below looks at trends in wholesale prices of 2-6-year old vehicles, indexed to the first week of the year. Last week, we approached the increases that we saw last summer – wholesale prices are almost 20% higher compared to the beginning of the year (adjusted for the mix).

Retail (Used and New) Insights

Supply chain shortages continue to plague the OEMs. Not only is there a shortage of microchips and seat foam, but now OEMs need to worry about the supply of rubber for tires.

Ford announced additional planned downtime for their top selling F150 full-size pickup production. Honda, Volkswagen, and Nissan were just a few more with recent announcements of plant disruptions due to the ongoing supply issues this past week.

New vehicle news was prolific this past week, with the official unveiling of the Hyundai Santa Cruz, the all-electric Mercedes-Benz EQS sedan, and Audi’s latest all-electric crossover, the Q4 e-tron.

Ford announced their version of autopilot, named ‘BlueCruise’. Their hands-free driving assistance system will cost $600 for 3 years. The subscription is in addition to the initial option cost for a vehicle to come equipped with the technology.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices over the last several weeks of 2020. As demand rebounded in January, retail prices seemed to lag wholesale prices – retail asking prices continued to decline throughout January and remained stable in February. March had an accelerated growth in retail prices, but the rate of growth is still lower compared to the increases of wholesale prices. In April, retail prices picked up speed as demand accelerated fueled by stimulus payments, tax season, and shortages of new inventory. This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles (similar to our wholesale price index).

Volume

Used Retail

Used retail listing volume stayed essentially flat since the beginning of the year but remains at levels above where the industry was in January, during the pre-COVID time of 2019.

Days-to-turn have been increasing since November and was approaching a historic average level at the end of February. However, this trend has reversed since the middle of March, as retail demand picks up across the country as a result of tax returns and the additional round of $1,400 stimulus checks being deposited into consumers’ bank accounts.

Wholesale

Volume offered for sale each week remains extremely tight as sellers have little inventory available to offer. The continued tight supply levels and elevated retail demand are resulting in strong conversion rates.

Condition of units is trending toward the “edgier” side with damage, dash lights illuminated, and/or vehicles running on red and yellow lights. There is also a noticeable increase in the number of vehicles being offered for sale with open recalls.

Remarketers are expecting their shortage of available units to last well into the Summer. Reduced rental returns to the market and lack of substantial volume of repossessions continue to have the largest impact on the wholesale supply levels.

More Auto Finance

Positive Equity Reaches Record High

Mainstream vehicle owners who bought a car seven years ago are likely to have positive equity when trading in for a new vehicle, according to second-quarter Edmunds data.

Read More →

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →