Wholesale Prices, Week Ending August 28th

The rate of depreciation has been slowing in recent weeks and this past week, the overall Car segment week-over-week change crossed back into positive territory, with six out of the nine Car segments reporting gains. Additionally, seven Truck segments also reported week-over-week gains. Compact and Full-Size Vans continue to lead with the largest increases.

This Week Last Week 2017-2019 Average (Same Week)

Car segments +0.06% -0.12% -0.10%

Truck & SUV segments -0.14% -0.48% -0.14%

Market -0.07% -0.36% -0.12%

Car Segments

On a volume-weighted basis, the overall Car segment increased +0.06%. For reference, the previous week cars decreased by –0.12%.

Compact (+0.22%) and Mid-Size (+0.29%) segments had the largest gains last week, increasing their appreciation compared to the prior week’s changes of +0.17% and +0.07%, respectively.

The Sub-Compact Car segment declined for a fourth week in a row, but the rate of decline did lessen this past week (-0.32%) compared to the week prior (-0.74%).

Truck / SUV Segments

The volume-weighted, overall Truck segment declined -0.14%, significantly less than the previous week’s decline of -0.48%.

Compact (+1.26%) and Full-Size (+0.83%) Vans increased again this past week. Full-Size Vans have increased thirty out of the last thirty-one weeks.

Full-Size Trucks continue to decline, but the rate of decline is slowing down. This past week, they fell -0.74% compared to the previous week’s decline of -1.48%.

Weekly Wholesale Index

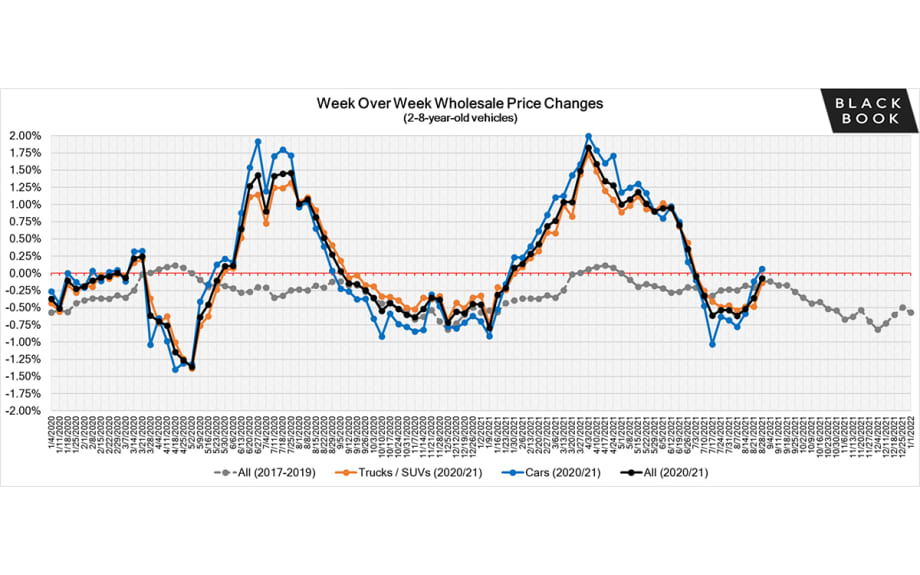

Calendar year 2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 has not had typical seasonality patterns as the market has had rapid increases in wholesale values for the majority of the year. After reaching record heights at the end of June, wholesale prices began to decline at a rate higher than the typical seasonal decline. Last week the trend changed with the rate of decline leveling off.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year.

Retail (Used and New) Insights

Honda is the latest manufacturer to announce cuts to production. Honda sent letters to their dealers last week letting them know how new vehicle deliveries would be impacted, with a warning that production cuts could be by as much as 40%.

General Motors is now requiring all salaried U.S. employees to report their COVID-19 vaccination status to help them plan their safety protocols. There is no official return-to-work plan yet for GM.

Ford announced more plant closures and reduced shifts at three of their North American facilities, two of which produce their top-selling F-150 pickup. Ford Edge and Lincoln Nautilus are also impacted by this announcement.

In an effort to keep production going, OEMs have been altering their build combinations. Ram is the latest to make this decision with their 2022 Ram 1500. The truck will lose the Quad Cab option on all but the two base trims as well as some changes to the availability of options such as air ride suspension and the multifunction tailgate on select trims.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices for the last several weeks of 2020. As demand rebounded, retail prices have lagged slightly behind wholesale prices, but March had an accelerated growth in retail prices. In April and May, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. In June, retail prices continued to rise. After strong Spring and Summer months, retail listing prices seemed to stabilize at a level more than 24% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles.

Inventory

Used Retail

Current used retail listing volume is about 14% below the start of the year. Used inventory is now starting to decrease again due to slow down of trade-ins and lease returns.

Days-to-turn for used retail listings have been increasing, as retail demand softened over the last few weeks. The days-to-turn now sits just below 34 days, which is still lower than what is typically expected in a normal year.

Wholesale

Sales rates increased again last week. Consignors have been lowering their floors and experiencing a high level of success with bids regularly soaring well over those floors.

Many dealers are reporting retail demand to be relatively soft, but with the continued announcements of disruptions to new car production that seem to have become the norm each week, they are continuing to seek out inventory in the wholesale market. The expectation is that with no clear picture on when new inventory levels will return to “normal” the demand will remain strong for used vehicles for the foreseeable future.

Newer used units are seeing considerable strength as they provide dealers with new car substitutes for their customers. The overall wholesale market for 2-8 year old vehicles declined by -0.07% last week, but 0-2 year old increased +0.07%.