Market Insights from Black Book

The lack of new inventory is continuing to drive up the demand for used vehicles, which in turn is forcing buyers to pay more week after week and leaving sellers wishing they had more to offer.

The lack of new inventory is continuing to drive up the demand for used vehicles, which in turn is forcing buyers to pay more week after week and leaving sellers wishing they had more to offer.

BLACK BOOK – Wholesale Prices, Week Ending October 23rd

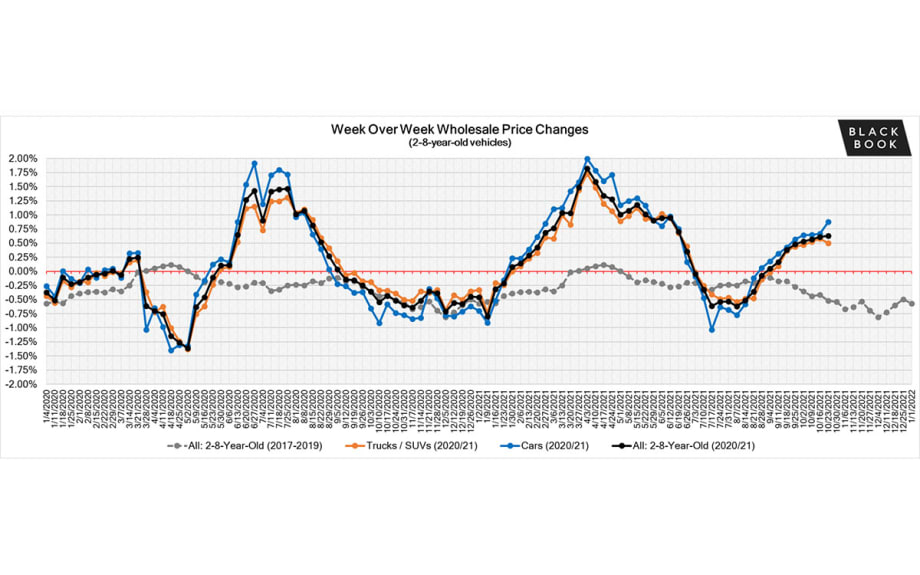

Availability of inventory continues to be a challenge for both buyers and sellers. The lack of new inventory is continuing to drive up the demand for used vehicles, which in turn is forcing buyers to pay more week after week and leaving sellers wishing they had more to offer. The market has now reported eight consecutive weeks of overall increases in wholesale values.

This Week Last Week 2017-2019 Average (Same Week)

Car segments +0.87% +0.67% -0.57%

Truck & SUV segments +0.50% +0.58% -0.48%

Market +0.63% +0.61% -0.52%

Car Segments

On a volume-weighted basis, the overall Car segment increased +0.87%. For reference, the previous week, cars increased by +0.67%.

All nine car segments reported gains again last week.

Mid-Size Cars increased for a tenth week in a row with a gain of +1.29% last week, an increase from the prior week’s already large gain of +1.11%.

Compact Cars have also now reported ten consecutive weeks of increases for an average weekly increase of +0.68%.

Truck / SUV Segments

The volume-weighted, overall Truck segment increased +0.52%, compared to the previous week’s increase of +0.58%.

All thirteen truck segments reported gains last week.

Full-Size Van values continue to push higher, now reporting increases thirty-eight out of the last thirty-nine weeks. The average weekly increase is +0.56%.

Compact Vans have also had consistent week-over-week increases, with gains reported in thirty-six out of the last thirty-eight weeks, for an average weekly gain of +0.65%.

Weekly Wholesale Index

Calendar year 2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 has not had typical seasonality patterns as the market has had rapid increases in wholesale values for the majority of the year. After reaching record heights at the end of June, wholesale prices began to decline at a rate higher than the typical seasonal decline through July and most of August. As we moved into the Fall season, wholesale prices began to show a positive movement once again and reached the highest point of the year last week, at 1.43.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year.

Retail (Used and New) Insights

North American factories cut 26,000 more vehicles from their production plans last week, because of the global microchip shortage per AutoForecast Solutions.

After cancelling plans to bring the EQC stateside last year, Mercedes-Benz has announced that the EQC electric compact crossover will arrive in the US after all, in 2025, with the addition of a battery-powered C-Class sedan.

Tesla rolled back the latest version of its Full Self-Driving (FSD) beta software, less than a day after its release, after users complained of false collision warnings and other issues.

Rivian expects Q3 losses of up to $1.28 billion due to higher production costs for the debut of their EV pickup truck, the R1T.

The 2022 GMC Sierra is expected to arrive at dealerships in the first quarter, with new higher-end trims, completely redesigned interior, and hands-free Super Cruise driving as part of a mid-cycle refresh.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices for the last several weeks of 2020. As demand rebounded, retail prices have lagged slightly behind wholesale prices, but March had an accelerated growth in retail prices. In April and May, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. In June, retail prices continued to rise at a slower rate. After strong increases during the Spring and early Summer, the retail listing prices index has increased to around 29% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles.

Inventory

Used Retail

Current used retail listing volume is about 17% below the start of the year. Used inventory is now starting to decrease again due to a slowdown of trade-ins and lease returns.

Days-to-turn for used retail listings have been increasing, as retail demand softened over the last month. The days-to-turn now sits just above 36 days, which is still lower than what is typically expected in a normal year.

Wholesale

Activity on the lanes continues to be strong, particularly on anything that is a late model year with low mileage. Not only are the big buyers active, but the rental companies have been seen actively seeking out inventory due to the lack of new inventory to replace their aging units. While remarketing and OEM auction lanes have seemed to dwindle over the last few months, dealer lanes have had consistently high volume.

The overall wholesale market for 2-8-year-old vehicles increased by +0.63% last week, and 0-2-year-old vehicles increased +0.61%. After many weeks of the late model units reporting higher gains than the older, that trend has slowed over the last couple of weeks with the older segment of the market reporting larger gains. Newer used units have already been higher than new vehicle pricing levels, so it is not surprising that the rate of gain is beginning to slow.

More Auto Finance

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →

Permission or Approval: When to Notify Finance Sources

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Read More →

At-Risk Auto Borrowers Drive Looser Credit Access

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Read More →

Auto Loan Forecast Bucks Market Trend

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Read More →

Auto Credit More Plentiful

Growing access shows greater lender appetite for risk as consumers take on heavier debt burden in an inflated market.

Read More →

Auto Loans Long as Stretch Limos

More consumers, faced with ever-rising car prices, are adapting by agreeing to longer loan terms despite the cost of added interest payments.

Read More →

AutoPayPlus Launches RePayPlus

The reinsured biweekly payment program offers auto dealers with customer retention and reinsurance structure.

Read More →