Black Book: Market Insights Report

Franchise dealers have started noticeably competing against large independent dealers for desirable units, but rental partners have really shown their dominance in many lanes, especially for cleaner, low-mileage vehicles.

Franchise dealers have started noticeably competing against large independent dealers for desirable units, but rental partners have really shown their dominance in many lanes, especially for cleaner, low-mileage vehicles.

BLACK BOOK Market Insights – 3/22/2022

Wholesale Prices, Week Ending March 19th

With fuel prices rising, the Sub-Compact Car segment moved into positive territory and Compact Cars slowed the rate of decline last week. However, the overall market continues to decline, but the pace of the declines has been slowing in recent weeks. In the pre-Covid market, we would expect the spring market / tax season increases to start around this time of year.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -0.52% -0.81% +0.20%

Truck & SUV segments -0.51% -0.56% -0.17%

Market -0.51% -0.64% -0.01%

Car Segments

On a volume-weighted basis, the overall Car segment decreased -0.52%. For reference, the previous week, cars decreased by -0.81%.

Eight of the nine Car segments declined last week.

After six weeks of declines, Sub-Compact Cars increased +0.07%, the only Car segment to increase last week.

Compact Cars continue to slow their rate of declines each week, with last week softening -0.13%, compared to -0.38% and -0.72% in the first two weeks of March.

Sporty Car (-1.49%) reported the largest decline, but Prestige Luxury Car was not far behind at -1.39%.

Truck / SUV Segments

The volume-weighted, overall Truck segment decreased -0.51%, compared to the prior week’s decrease of -0.56%.

Twelve out of the thirteen Truck segments reported declines.

Full-Size Vans continued to increase with an additional gain last week of +0.71%.

Sub-Compact Luxury Crossovers (-1.64%) and Small Pickups (-1.31%) were the only Truck segments with declines exceeding 1%.

Fuel-efficient crossovers are continuing to decline, but the rate of decline has lessened with Sub-Compact Crossovers declining -0.46%, compared to -0.98% the week prior and Compact Crossovers declining -0.46%, compared to -0.76% previously.

Weekly Wholesale Index

Calendar year 2020 and 2021 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the last 2 years. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 did not have typical seasonality patterns as the market had rapid increases in wholesale values for the majority of the year. The Wholesale Weekly Price Index reached the highest point of the year at the end of December, reporting over 1.51 points. Now, in calendar year 2022, the index has been reverted back to the 1.00 mark and overall wholesale prices have remained relatively stable in the month of January (green line). As we moved into March, the Wholesale Weekly Price Index continued to decline and is now just below the 2019 trend line, around 0.97.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Retail (Used and New) Insights

GM announced that they will discontinue both the Chevrolet Trax and Buick Encore subcompact crossovers in August.

Cadillac will begin taking orders for their first EVs – the 2023 Lyriq and Lyriq Performance AWD – on May 19th of this year.

Honda is planning to spend $1.1B to retool Ontario factories for hybrid vehicles as part of their shift towards fully EV product line by 2040.

Toyota will suspend operations at 11 factories in Japan and is studying potential disruption to overseas production because of supply chain interruptions triggered by a large earthquake in Japan last week. Affected models include RAV4, C-HR, Land Cruiser, and Lexus LS and NX.

Maserati announced they will be going fully electric by 2030, with all vehicles having a battery electric version by 2025.

Infiniti revealed plans for a new two-row crossover in 2025, based on the same platform of the midsize QX60; the new crossover fills a space between Infiniti’s three-row QX60 and its compact two-row QX50 crossovers. Competitors will include the Lexus RX and Mercedes GLE.

Audi is expanding their EV lineup; they previewed a spacious battery-electric station wagon concept – the A6 Avant e-tron – last week.

Used Retail Prices

Used Retail Prices are more accessible than in years past, due to the proliferation of ‘no-haggle pricing’ for used-vehicle retailing. Transparent pricing upfront makes the car buying process more enjoyable for customers and allows Black Book to accurately measure retail market trends.

At the on-set of the pandemic, in CY2020, used retail prices increased slightly, following typical seasonal patterns, and then began dropping in April, finally hitting a low point in the late spring months. By late summer of CY2020, Used Retail Prices increased as supply of new vehicle inventory started to become scarce, but retail demand slowed down at the end of CY2020, resulting in declining retail asking prices for the last several weeks of the year. When CY2021 kicked off, demand rebounded while retail prices lagged slightly behind wholesale prices; March of 2021 started the dramatic increases in Used Retail Prices, fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up the pace once again to start the fourth quarter. In Q4, prices on retail listings steadily increased week after week. As CY2021 came to an end, the retail listing price index closed 36% above where the year began.So far in 2022, the Retail Listings Price Index has remained relatively unchanged (green curve on the graph below), the Index sits around 0.99, indicating a very slight decrease in retail pricing. Typically, there is a lag between changes in wholesale prices and retail prices.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graph below looks at 2-6-year-old vehicles. The Index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

Used Retail Listing Volume has dropped again this week, and now sits below where we started the year. The Index for CY22 is beginning to mirror CY20 with similar week over week declines.

Used Retail Days-to-Turn dropped this week as well – from above 45 days to just below 44 days.

Wholesale

Heated competition has led to increased prices in some lanes – many segments showed less severe overall depreciation this week and Sub-Compact Cars even increased in value for the first time since January. Franchise dealers have started noticeably competing against large independent dealers for desirable units, but rental partners have really shown their dominance in many lanes, especially for cleaner, low-mileage vehicles. With a spring / tax-season market essentially here, franchise and independent dealers alike need inventory to entice customers. Not to mention, with covid restrictions rolling back, travel plans have significantly increased domestically for spring and summer breaks, so rental companies are more than happy to pay top price for cleaner, low-mileage vehicles as they turn over their high mileage inventory. It seems the real winners right now are the sellers that still have inventory.

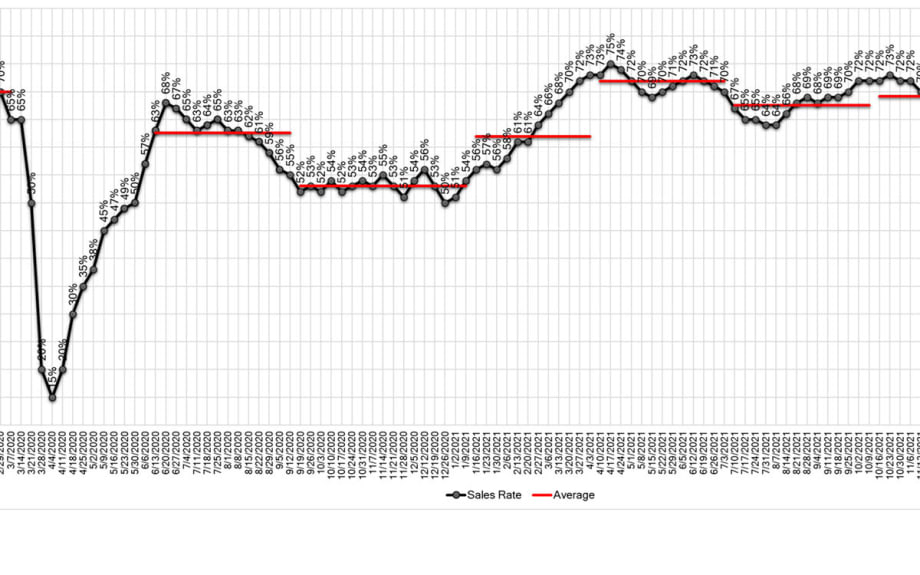

The Estimated Average Weekly Sales Rate has started to pick up over the last few weeks but remains at 65% again this week. March is nearly over, and the Estimated Average Weekly Sales Rate has not had a large increase like CY21.

More Auto Finance

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →

Permission or Approval: When to Notify Finance Sources

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Read More →

At-Risk Auto Borrowers Drive Looser Credit Access

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Read More →

Auto Loan Forecast Bucks Market Trend

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Read More →

Auto Credit More Plentiful

Growing access shows greater lender appetite for risk as consumers take on heavier debt burden in an inflated market.

Read More →

Auto Loans Long as Stretch Limos

More consumers, faced with ever-rising car prices, are adapting by agreeing to longer loan terms despite the cost of added interest payments.

Read More →

AutoPayPlus Launches RePayPlus

The reinsured biweekly payment program offers auto dealers with customer retention and reinsurance structure.

Read More →