Black Book: Specialty Market Updates

The big picture has not changed much from last month to now; overall prices are increasing, but by much smaller amounts than we have seen since the pandemic began a little over two years ago.

The big picture has not changed much from last month to now; overall prices are increasing, but by much smaller amounts than we have seen since the pandemic began a little over two years ago.

BLACK BOOK Specialty Market Insights – 4/21/2022

Motorcycle and Powersports Market Update

“Gas, cars, houses, food, and Powersports vehicles, these are all items that have continued to increase in price since the start of the pandemic a little over two years ago. Despite record high prices across all segments, values continue to increase month over month for virtually all vehicle types. Personal Watercraft and Jet Boats are seeing particularly large gains this month as warmer weather is just around the corner and many dealers have already pre-sold the majority of their incoming spring inventory.”– Scott Yarbrough, Senior Analyst, Motorcycle & Powersports

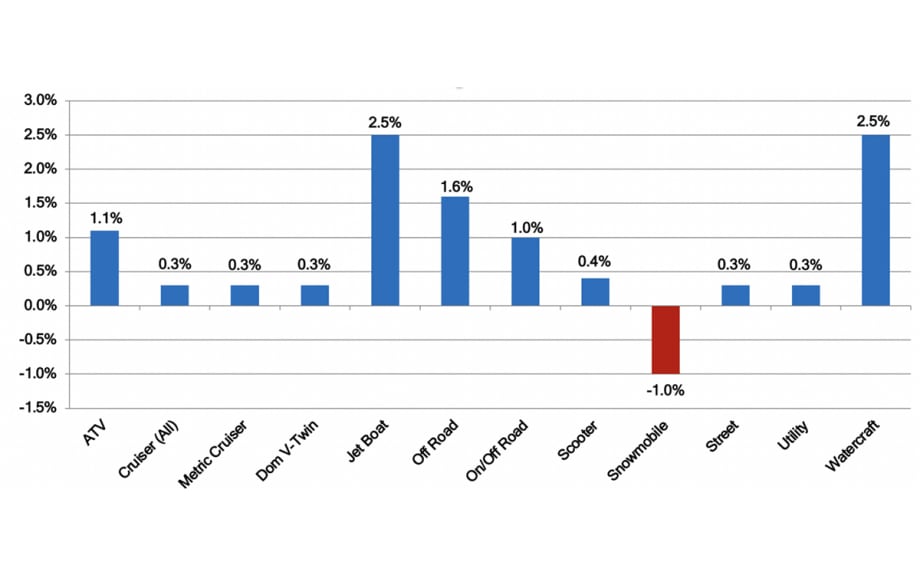

March to April Average Segment Change in Value

The big picture has not changed much from last month to now; overall prices are increasing, but by much smaller amounts than we have seen since the pandemic began a little over two years ago. The water-based segments are currently experiencing the highest levels of appreciation as we have heard from many dealers that they have been very successful pre-selling incoming new units, leaving them on the lookout for quality used inventory, which is reflected in the rising prices. Off-road units continue to see strong demand as well, with the ATVs, Dual Sports, and Dirt Bikes all showing gains of 1.0% or more. All other segments are up by roughly 0.3%, though we expect them to increase by higher amounts as the spring selling season heats up, especially as the supply of new units from the OEMs remains constrained.

Segment Spotlights & Industry News

Street Bike Performance

Street Bike performance is fairly typical for the time of year, though the increases are a bit smaller than would normally be expected. More than making up for the smaller changes in value is the fact that prices are, and have been, significantly elevated from historical averages. Especially when compared with last year, it is easy to see how the market is slowly heading back towards pre-pandemic valuation trends, though we still have a long way to go.

Dirt Bike Segment Performance

The Dirt Bikes, much like the Street Bikes, are showing signs of returning to pre-pandemic valuation trends as can be seen by comparing their performance this year vs last, where they virtually never showed any declines. This year we are seeing some negative months, along with smaller changes in the positive months. Overall prices are still, and we expect them to remain this way for the rest of the year, highly elevated from past levels.

The Bureau of Labor Statistics latest data show an annual inflation rate of 8.5%, the highest in a little over 40 years. Russia’s invasion of Ukraine is the latest shock to our interconnected global markets and supply chains, driving energy prices significantly higher, which accounted for the largest share of the increase, though there were also substantial bumps in housing and food costs as well.

CDK Global, a major provider of retail and DMS systems in the Automotive and Powersports industries, is being acquired by Brookfield Business Partners, a private equity group with nearly $700 billion of assets under management, for $8.3 billion.

The U.S. Government has reinstated exclusions for tariffs on multiple powersports items imported from China. Among the items included are motorcycles, parts, and helmets. These exclusions are retroactive to Oct 12, 2021 and run through the end of 2022.

Cars of Particular Interest

“There’s a lot going in the world right now: Russia has attacked Ukraine, a new Coronavirus variant is making the rounds, gas prices are through the roof, inflation is at a several decade high, and the Fed has been raising interest rates. In spite of all of this, or perhaps because of it, the collectible car market remains very strong. Auctions are seeing increased attendance and record prices are being set seemingly every week.”– Eric Lawrence, Principal Analyst, Specialty Markets

Auction Activity

Returning to the state of Florida after a three-year hiatus, Barrett-Jackson’s Palm Beach auction, held at the South Florida Fairgrounds, was their most successful ever at that location. Total sales came in at $60.7 million, and as this was a “no-reserve” auction, all 676 vehicles that crossed the block were sold to the highest bidder. Eighty of these sales were for world-record amounts, and $3.8 million was raised for charity.

Artcurial’s Retromobile auction in Paris generated sales of $41.7 million with an 82% sell through rate.

RM Sotheby’s 19th annual Fort Lauderdale auction reported just shy of $17 million in total sales. Of the 264 vehicles offered, 171 (65%) went home with new owners. The highlight of the sale was the 2005 Ford GT Coupe that had been owned from new by musician Kid Rock. Painted in Mark IV Red with contrasting white stripes, it sold for $638,000 and included an autographed guitar.

Mecum is off to a strong start in 2022, with total sales of over $300 million. Their fourth annual Glendale, Arizona auction totaled $66.3 million, the highest ever, with 1,285 of 1,657 selling for an impressive sell through rate of 78%. This year’s totals were 53% higher than last year’s Covid limited event, and attendance was up by 37%. Their auction in Houston, Texas also set an event record, with total sales of $34.5 million. 900 of the 1,047 vehicles were sold, for an excellent sell through percentage of 86%. The top three sellers were replicas: an Eleanor Tribute 1968 Mustang Fastback from Gone in 60 Seconds ($253,000), a 1967 Pontiac Monkeemobile from the Monkees TV show ($242,000), and a 1959 Cadillac Ecto 1 ambulance from Ghostbusters ($220,000). Their Gone Farmin’ auction in East Moline, Illinois saw total sales of $7.8 million with a 93% sell through rate.

Notable Recent Auction Sales Include:

2020 Ford GT Carbon Series Coupe $1,540,000 (Barrett-Jackson)

2018 Ford GT 1967 Heritage Edition $1,430,000 (Barrett-Jackson)

1968 Chevrolet Yenko Super Camaro 427 $533,500 (Barrett-Jackson)

1984 Lamborghini Countach LP500 S $632,500 (RM Sotheby’s)

1984 Ferrari 512 BBi Coupe $462,000 (RM Sotheby’s)

1972 Maserati Ghibli SS Coupe $352,000 (RM Sotheby’s)

1996 Ferrari F50 $4,577,760 (Artcurial)

1986 Porsche 911 Turbo Coupe $189,750 (Mecum)

1967 Ferrari 275 GTB/4 Coupe $3,025,000 (Mecum)

1995 Rolls-Royce Corniche S Convertible $412,000 (Mecum)

1929 Duesenberg Model J Murphy Convertible Courtesy of Mecum

Market Trends

The Vintage Exotic segment focuses on high dollar European exotic sports cars produced from the late 1950s up through the mid-1970s. This is without a doubt the top of the market. This segment includes Ferrari 250s, 275s, and 365s, Lamborghini Miuras, Maserati Ghiblis, Mercedes-Benz Gullwings, Porsche Speedsters, and coach-built Bentleys and Rolls-Royces. Although most owners of these vehicles are wealthy individuals, the market can be very volatile and fluctuates quite a bit as they fall in and out of favor, sometimes being seen as a safe haven in which to park money and other times as an out-of-touch extravagance. Values have been generally increasing for about a year, with some more desirable models rising faster than others.

Almost all of the various collectible vehicle segments that we track increased in value last year, including Vintage Muscle Cars, Vintage Pony Cars, American Classics, Vintage Exotics, and Classic Trucks & SUVs. The only segment which declined year over year were the Vintage European Sports Cars. The fact that they declined is not a big surprise. Many of their values, led by early Porsche 911s, had increased dramatically a few years ago, and the market is still finding its equilibirum. In fact, last month we saw that the segment had actually increased month-over-month, so it’s not like they have fallen out of favor with collectors. Although we don’t really have a dedicated segment for them, because by defination they are all different, custom cars and “restomods” have become very popular over the past several years and often bring big money at auction.

“Spring has arrived in most parts of the country and eager customers are flocking to dealers’ showrooms. Motorhome values bounced back this month after three months of declines, but towables gave back some of the gains they notched last month. Inflation and gas prices remain high, and the ongoing war in Ukraine has a lot of people concerned, but dealers are reporting normal showroom traffic.” – Eric Lawrence, Principal Analyst, Specialty Markets

Wholesale RV Values Mixed As Spring Arrives

For Motorhomes (including Class A, B, and C):

The average selling price was $76,332, up $7,490 (10.8%) from the previous month.

One year ago, the average selling price was $59,092.

Auction volume was up 19.1% from the previous month.

The average model year was 2009.

For Towables (including Travel Trailers and Fifth Wheels):

The average selling price was $20,938, down $927 (4.2%) from the previous month.

One year ago, the average selling price was $20,371.

Auction volume was down 3.8% from the previous month.

The average model year was 2016.

Industry Highlights

According to the RVIA, the total number of RVs shipped in February was 53,722, an increase of 11.3% over February 2021. Towables totaled 48,220 units and Motorhomes accounted for 5,502. Truck Campers came in at 374, Folding Camping Trailers reached 691, and Park Models were 309. Class B motorhomes (Van Campers) ended the month with 1,573 shipped, Class A’s totaled 1,342, and Class C’s finished with 2,587.

Megadealer Lazydays reported revenues of $322.5 million for the fourth quarter of 2021, up $126 million (64.1%) over 2020.

Statistical Surveys, Inc. reported that there were 24,637 RV registrations in North America in January 2022, the second-best January ever.

Winnebago announced they built their 500,000th motorhome, the first manufacturer to reach that milestone.

The Baird RV Dealer Survey found that a majority of responding dealers were positive on both current market conditions (55 of 100) and the three-to-five-year outlook (53 of 100). A score over 50 is considered positive.

THOR Industries reported fiscal Q2 2022 Net Sales of $3.8 billion, up 42.1% over 2021.

The RVIA announced that the average buyer is spending $73,115 to purchase a new RV.

Medium and Heavy-Duty Truck & Commercial Trailer Market Update

Commercial Truck Market Update

“Supply chain issues continue to plague new truck production, causing fleets to keep units in service much longer than originally anticipated. Fuel prices have been increasing over the past 12 months and are expected to continue to rise as the conflict between Russia and Ukraine continues. The conflict will likely cause further delays in new truck production; helping to further strengthen new and used Commercial Truck values. As a result, some construction and logistics companies are having to rely on used equipment to try and keep a fresh fleet. Medium and Heavy-Duty Truck and Commercial Trailer values continue a positive trend as we continue through the second quarter of 2022. Used prices will remain strong for the remainder of this year as OEMs work with suppliers to try and meet customer demand; however, it will like likely be the second quarter of 2023 before we see any significant depreciation in any commercial segment. “ – Josh Giles, Principal Automotive Analyst

Medium-Duty Trucks

The chart above illustrates monthly adjustment amounts for Medium-Duty cab/chassis units in classes 3 through 6 for model years 2011-2018.

Heading into April, Medium-Duty truck values between 2011 and 2018 decreased an overall weighted average of $663 (-1.7%) compared to the $54 (+0.1%) increase seen the month prior.

Over the past twelve months Medium-Duty units (2011-2018) have increased $9,142 (+33.7%), from an overall weighted average of $25,338 to $39,256.

Over the past ten years Medium-Duty truck values (4-10 year old) have increased $24,334 (+112.8%), from an average of $18,092 to an average of $39,256.

We expect these averages to continue increasing as new equipment becomes more and more expensive.

Heavy-Duty Trucks and Tractors

The chart above illustrates the average monthly adjustment amount for Heavy-Duty Trucks and Road Tractors within classes 7 and 8 (2011-2018).

From March to April, Construction/Vocational Units increased an overall weighted average of $2,464 (+3.0%) compared to the $605 (+0.7%) increase seen the month prior.

Over-the-Road units increased an average of $1,696 (+3.0%) heading into April, compared to the $214 (+0.4%) average increase seen the month prior.

Regional Tractors followed a similar trend, increasing an average of $1,651 (+3.2%) from March to April, compared to the $227 (+0.4%) average increase seen the month prior.

Over the past twelve months, Construction/Vocational (2011-2018) average values have increased $22,777 (+32.2%), Over-the-Road Tractors have increased $19,141 (+45.3%), and Regional Tractor values increased $19,012 (+51.8%).

Over the past ten years, 4–10 year old Construction/Vocational models have increased an average of $30,715 (+55.8%), Over-the-Road Tractors have increased an average of $25,074 (+74.3%), and Regional Tractors have increased an average of $24,221 (+85.1%).

Commercial Trailer Market Update

Commercial Trailer values continue to increase as freight demand increases and New and Used Commercial Trailer inventory becomes more scarce.

Dry Van values (2017-2021) have increased $10,751 (+37.6%) since the first of the year.

Dump Trailers values (2017-2021) have increase $2,383 (+5.4%) since the beginning of 2022.

Refrigerated Van values (2017-2021) have increased $8,850 (+18.5%) since the beginning of the year.

Lowboy Trailer values (2017-2021) have dropped $500 (-0.7%) since the beginning of 2022.

Retail and Freight Demand

According to Federal Reserve Economic Data (FRED), new retail sales for Commercial units in classes 4 through 8 were reported at 34,863 units in March of 2022. This is up 2,593 units from February.

We expect to see these retail sales figures stabilize and slowly begin to increase towards the fourth quarter of 2022.

ATA Truck Tonnage is one of the many leading indicators when it comes to the strength and stability of the trucking and freight industry.

In February of 2022, ATA Truck Tonnage was reported at 115.1% compared to January’s rate of 115.5%. These figures have been inching up over the past six months, which is wonderful news as distribution companies work to release some of the congested ports.

Freight demand remains strong and continues to trend in a positive direction. However, as the conflict between Russia and Ukraine escalates, we may see ATA Truck Tonnage drop as this conflict will impact importing and exporting from that region.

More Auto Finance

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →

Permission or Approval: When to Notify Finance Sources

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Read More →

At-Risk Auto Borrowers Drive Looser Credit Access

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Read More →

Auto Loan Forecast Bucks Market Trend

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Read More →

Auto Credit More Plentiful

Growing access shows greater lender appetite for risk as consumers take on heavier debt burden in an inflated market.

Read More →

Auto Loans Long as Stretch Limos

More consumers, faced with ever-rising car prices, are adapting by agreeing to longer loan terms despite the cost of added interest payments.

Read More →

AutoPayPlus Launches RePayPlus

The reinsured biweekly payment program offers auto dealers with customer retention and reinsurance structure.

Read More →