Black Book: Weekly Market Update

The fourth quarter is traditionally when the market experiences most of the yearly depreciation, but after just one month in the quarter, values are reporting appreciation of more than 3.0%.

The fourth quarter is traditionally when the market experiences most of the yearly depreciation, but after just one month in the quarter, values are reporting appreciation of more than 3.0%.

BLACK BOOK – Wholesale Prices, Week Ending October 30th

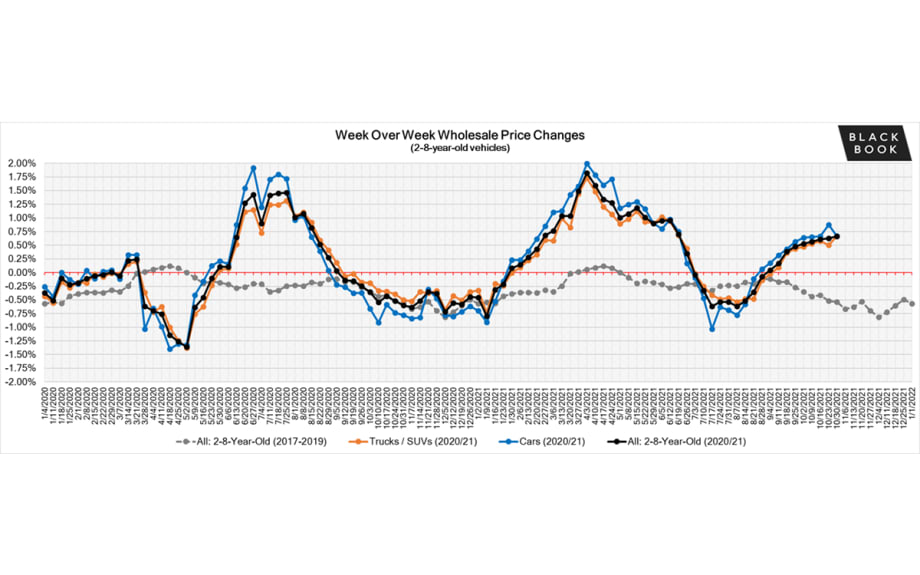

The trend of increasing values continued for a ninth consecutive week, with all segments reporting gains this past week. The fourth quarter is traditionally when the market experiences most of the yearly depreciation, but after just one month in the quarter, values are reporting appreciation of more than 3.0%.

This Week Last Week 2017-2019 Average (Same Week)

Car segments +0.67% +0.87% -0.57%

Truck & SUV segments +0.66% +0.50% -0.51%

Market +0.66% +0.63% -0.54%

Car Segments

On a volume-weighted basis, the overall Car segment increased +0.67%. For reference, the previous week, cars increased by +0.87%.

All nine car segments reported gains again last week.

Mid-Size Cars (+1.08%) increased for an eleventh week in a row for an average weekly increase of +0.76%. Four of the last five weeks of increases exceeded 1%.

Sub-Compact Cars increased +0.62%, compared to the same week in 2019, when the segment had a decline of -1.03%.

Truck / SUV Segments

The volume-weighted, overall Truck segment increased +0.66%, compared to the previous week’s increase of +0.50%.

All thirteen truck segments reported gains last week.

Compact Crossovers reported the largest segment increase last week, +1.46%.

The Compact Crossover segment wasn’t the only one to have an increase greater than 1%, Sub-Compact (+1.13%), Sub-Compact Luxury (+1.32%), and Compact Luxury (+1.03%) also reported large weekly gains.

Weekly Wholesale Index

Calendar year 2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 has not had typical seasonality patterns as the market has had rapid increases in wholesale values for the majority of the year. After reaching record heights at the end of June, wholesale prices began to decline at a rate higher than the typical seasonal decline through July and most of August. As we moved into the Fall season, wholesale prices began to show a positive movement once again and reached the highest point of the year last week, at 1.43.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year.

Retail (Used and New) Insights

Lucid Motors has officially started their first customer deliveries of the groundbreaking and luxurious Lucid Air sedan, which is the longest-range electric car ever produced, with 520 miles/837 km of EPA range.

Toyota Motors announced plans to spend $461M at its Kentucky plant to meet shifting customer demand, reduce their carbon footprint, and advance its future capability.

Amazon disclosed that it owns a 20% stake in Rivian, the electric automaker that filed for an IPO last month.

Nearly nine out of every 10 vehicles (56,000 of ~63,000) cut from global production plans last week, due to the ongoing microchip shortage, were from North American plants, according to the latest estimate by AutoForecast Solutions.

Mercedes-Benz announced that dealer profit margins will be cut half a percent, down to 13%, to help fund EV transition.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices for the last several weeks of 2020. As demand rebounded, retail prices have lagged slightly behind wholesale prices, but March had an accelerated growth in retail prices. In April and May, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but have since picked back up. After continued strong increases, the retail listing prices index has increased to just over 29% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles.

Inventory

Used Retail

Typically, used inventory significantly increases in Q4 as manufacturers and dealers switch over to the new model year. This year, due to the microchip shortage, we do not expect such a high volume of used vehicles. In the last four weeks, used inventory stopped declining and stabilized at around 16% below where we started the year.

Days-to-turn for used retail listings decreased over the last month, after a few weeks of slight increases. The days-to-turn now sits just above 36 days, which is lower than what is typically expected in a normal year.

Wholesale

Activity in the auction lanes continues to be strong, particularly on later model year / low mileage inventory. Not only are the big franchise and independent buyers active, but rental companies have been actively competing in attempts to seek out inventory to replace their aging units, as new inventory continues to be in short supply. While manufacturer auction lanes have seemed to dwindle over the last few months, with fewer lease returns and repossessions, dealer lanes have thrived with consistently high volume across the country.

The overall wholesale market for 2-8-year-old vehicles increased by +0.66% last week, and 0-2-year-old vehicles increased +0.61%. Demand remains strong for the newer used units, but values on many models are already exceeding new car pricing.

More Auto Finance

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →

Permission or Approval: When to Notify Finance Sources

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Read More →

At-Risk Auto Borrowers Drive Looser Credit Access

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Read More →

Auto Loan Forecast Bucks Market Trend

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Read More →

Auto Credit More Plentiful

Growing access shows greater lender appetite for risk as consumers take on heavier debt burden in an inflated market.

Read More →

Auto Loans Long as Stretch Limos

More consumers, faced with ever-rising car prices, are adapting by agreeing to longer loan terms despite the cost of added interest payments.

Read More →

AutoPayPlus Launches RePayPlus

The reinsured biweekly payment program offers auto dealers with customer retention and reinsurance structure.

Read More →