Market on the Mend

The auto finance market continued to stabilize in the fourth quarter, as the crash of 2008 continues to become a distant memory. New financing, however, will remain the domain of the prime and superprime tiers in the months to come.

The auto finance industry spent most of 2009 on the mend. All lending segments — aside from banks — decreased their exposure from tiers outside of prime. By the fourth quarter of last year, delinquency and repossession rates began to stabilize, with signs of the market’s recovery beginning to emerge after one of the worst periods for the industry since the early ’80s.

Credit scores remained stable throughout the year, and new-vehicle financing became the domain of the prime customer. In contrast, consumers outside of prime were pushed more and more toward used vehicles, but even that side of the market was restricted. Average amount financed, term and rate all showed increases.

The good news is, the industry is no longer seeing the massive tightening that suppressed sales volumes and loan originations in 2009. The hope now is that the dramatic swings in consumer financing are now a thing of the past.

High-Risk Segments a Tough Sell

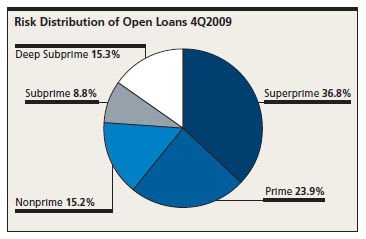

Last year saw only minor shifts in loan distributions between the credit tiers when compared to 2008, with 60.7 percent of all open auto loans falling into the superprime and prime tiers. However, the low-risk tiers grew 1.7 percent from the fourth quarter 2008, when the superprime and prime tiers accounted for 59.7 percent of open loans.

It was clear that finance sources shifted away from the higher risk segments, which experienced a year-over-year decrease in loan distributions. The only segment that remained stable was nonprime, while the subprime group decreased 3.15 percent to 8.8 percent of all open auto loans. Additionally, the deep subprime segment decreased 4.35 percent from the fourth quarter 2008 to 15.3 percent of all open automotive loans by the end of 2009.

Increases in Delinquency Rates Slowing

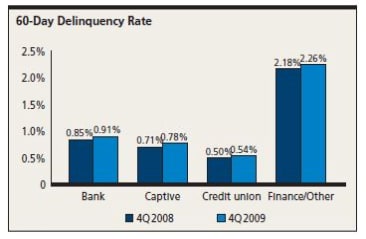

Delinquencies in 2009 continued to show year-over-year increases. However, the rate of increase has begun to slow. In the fourth quarter 2009, the 60-day delinquency rate reached 0.96 percent, a 3.49 percent increase from the fourth quarter 2008. This year-over-year increase, however, is considerably lower than the 11.64 percent increase between the fourth quarters of 2007 and 2008.

The lowest rate of increase was in “finance source or other.” That category’s 60-day delinquency rate was the highest among the lenders at 2.26 percent, but the segment experienced a mere 3.98 percent increase over the fourth quarter 2008. Credit unions held the lowest rate of delinquency at 0.54 percent, a 6.53 percent increase from 2008.

The greatest increase in the 60-day delinquency rate was in the captive auto segment, which increased 9.71 percent from the fourth quarter 2008 to a rate of 0.78 percent. The delinquency rate for the bank segment reached 0.91 percent, a 7.56 percent increase from 2008.

[PAGEBREAK]

Credit Scores Reveal Market Tightness

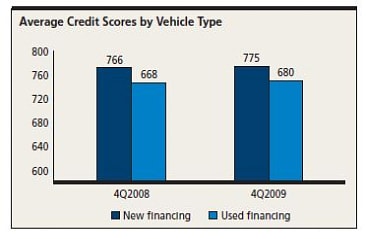

The tightening seen last year was most clearly demonstrated by the increase in average credit scores on newly originated auto loans. That increase is also the main reason why delinquency growth has slowed and overall credit has stabilized.

The average credit score on all vehicles was 715 in the fourth quarter 2009, a 12-point increase from 2008. And despite a nine-point year-over-year increase, credit scores for new financing remained very consistent throughout 2009.

Credit scores for used-vehicle financing realized steady increases throughout 2009, with a slight dip between the third and fourth quarters of 2009. The average used score was 680 in the fourth quarter, a 12-point increase from the fourth quarter 2008.

Amount Financed Rises as Credit Scores Improve

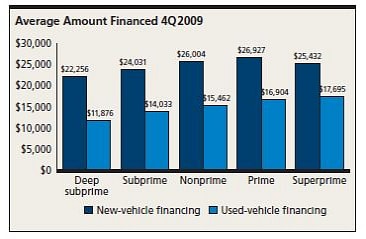

Typically, the amount a consumer finances increases as credit improves, which was the case for the fourth quarter 2009. Overall consumer financing for the quarter increased $766 from the previous year to $20,431.

The greatest increase in the average amount financed was seen in new-vehicle financing. The segment experienced a year-over-year increase of $1,141, resulting in an average amount financed of $25,580. However, stringent lender guidelines caused the average amount financed for the high-risk tiers to fall by $686 from the fourth quarter 2008.

In contrast, the average amount financed for consumers in the prime and superprime segments increased by more than $1,000 ($1,153 and $1,327, respectively) from the year-ago period.

Used-vehicle financing also saw an increase of $375, bringing the average amount financed in the year-end quarter to $16,276. Similar to new-vehicle financing, the average amount financed for used vehicles fell across the high-risk tiers. For instance, the amount financed for the deep subprime category fell by $814 from the fourth quarter 2008. The only segments to experience an increase in loan amounts were the prime and superprime segments, which grew by $241 and $663, respectively.

[PAGEBREAK]

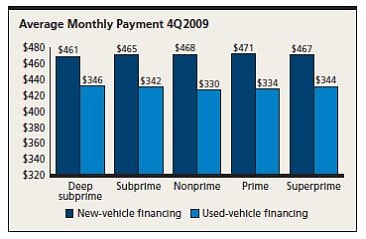

Tiers Outside of Prime See Declines in Monthly Payments

Monthly payments experienced a year-over-year increase for both new and used financing, with the average payment rising $2 to $467 for new and $3 to $340 for used in the fourth quarter.

Looking at financing across all risk segments reveals even more significant changes in payments. For instance, payments on new vehicles decreased for all risk segments outside prime, with the most significant decrease seen in the deep subprime segment. The monthly payment for that tier fell $16 to $461 for the end-of-year quarter.

Payments on used-vehicle financing mirrored the behavior of new financing, with decreases seen on all segments outside of prime. The most significant decrease was in the deep subprime tier, which fell by $6 in the fourth quarter 2009.

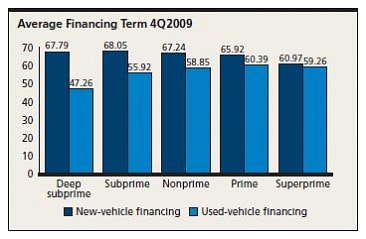

Average Term Appears Stable

A wide view of the market shows that finance term was one data point that changed very little on a year-over-year basis. However, reviewing term by risk segment tells an entirely different story. Overall, the average term remained constant at 60 months for all vehicles, 62 months for new financing, and decreased one month to 57 months for used financing.

Although new-vehicle terms experienced very little change, used-vehicle financing changed considerably for the high-risk segments. Overall used-vehicle terms decreased in the fourth quarter, with deep subprime falling by three months to an average of 47.26 months. The subprime segment dropped 2.46 months to 55.92 months, and nonprime decreased by 1.27 to an average term of 58.85 months.

Market to Remain Tight; Stabilization to Continue

The auto finance landscape continued to shift in 2009 after the market plunged in late 2008, but there were strong signs of overall stabilization. Nonetheless, the market remains challenging for consumers looking to obtain financing,

especially those who fall in the high-risk categories.

Additionally, expect finance amount and loan terms to continue to evolve for the high-risk loan segments as lenders increasingly adopt risk-based pricing strategies. The increasing use of those tactics was one of the main reasons used financing tightened for all categories outside of prime. The combination of auction values holding strong at the end of the year and the deceleration of delinquency rates, however, should help the market going forward.

Dealers should expect the new-vehicle side to remain the domain of prime consumers, with tiers outside of prime gaining some share in the smaller, budget-car categories. The hope is that the whipsaw dealers and auto finance sources experienced at the end of 2008 and into 2009 will become a distant memory, but it’s clear the dramatic swings are behind the market.

Melinda Zabritski is director of automotive credit for Experian Automotive. She can be reached at melinda.zabritski@bobit.com.

More Auto Finance

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →