Q4 Revisited: Affordability, Not Delinquency, Is Cause for Concern

Thirty- and 60-day delinquencies remained fairly stable in the fourth quarter, while affordability rightfully remains a key point of discussion among dealers and auto finance sources.

A look back at the state of the auto finance market in the final quarter of 2018 proves the affordability gap will be far more likely than portfolio performance to affect new-car sales and financing in 2019.

Photo by EmirMemedovski via Getty Images

There has been much discussion around delinquent automotive loans, with many saying that an uptick in delinquency foreshadows an impending downfall of the automotive industry. However, these statements lack a larger industry context.

The fact is, delinquencies were relatively stable in Q4 2018, according to Experian’s latest “State of the Automotive Finance Market” report, with 30-day delinquencies dropping year-over-year and 60-day delinquencies seeing only a small increase. But it’s important to remember that delinquencies are just one indicator of the automotive finance market, and it’s equally important to look at the whole story to truly gain insights from the available data.

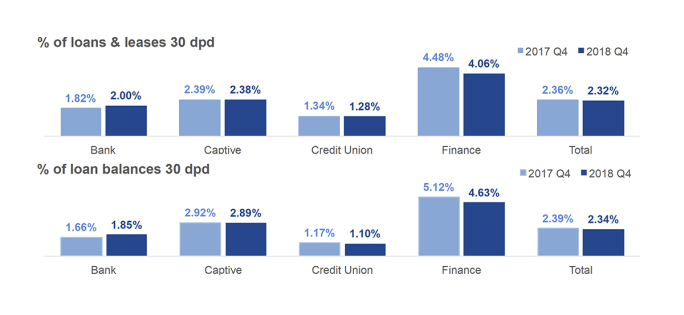

Delinquencies Are Relatively Stable

The overall rate of 30-day delinquencies fell from 2.36% in Q4 2017 to 2.32% in Q4 2018. Sixty-day delinquencies saw a slight uptick, from 0.78% to 0.76% year over year. These numbers reflect relative stability, as there has been an increase in the amount of consumers relying on automotive financing: In Q4 2010, 81.4% of consumers new financed vehicles, and just eight years later, in Q4 2018, 85.1% of all new-vehicle purchases were financed.

Source: Experian Automotive

Total automotive loan balances grew to a record-high $1.178 trillion in Q4 2018, a 4.4% leap from a year earlier. The total number of open automotive loans grew by 3% to more than 89 million in Q4 2018.

Average Dollar Amounts, Monthly Payments Hit Record Highs

In addition to delinquency chatter, affordability continues to be a topic of industry interest. In Q4 2018, average amounts for new- and used-vehicle loans and monthly payments for new- and used-vehicle loans reached record highs. The average amount for a used-vehicle loan reached $20,077 — the first time average used-vehicle loans surpassed the $20,000 threshold. New-vehicle loans also reached a record high of $31,722, up $623 from Q4 2017.

Source: Experian Automotive

Some of the factors impacting vehicle loans have been consumer preferences. Many car buyers have leaned toward more expensive vehicles, like crossovers and pickup trucks. Additionally, interest rates have been increasing, which can be a contributor to both the record monthly payments and loan amounts. The average interest rate for a new-vehicle loan was more than 6% in Q4 2018 — hitting 6.13%, up from 5.11% the previous year. For used-vehicle loans, the average interest rate was 9.59%.

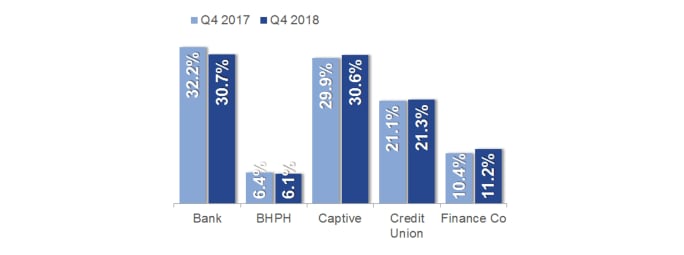

Market Share Is Shifting Away From Banks

In Q4 2018, the market share of total automotive financing shifted away from banks and buy-here, pay-here dealerships, while captives, credit unions, and finance companies all gained share.

Source: Experian Automotive

Credit unions experienced the most growth among automotive lenders, with a 10.7% increase in total loan balances. Captives and finance companies also exhibited strong growth. Captives jumped from $258.2 billion in Q4 2017 to $262.1 billion in Q4 2018, while finance companies grew from $189.3 billion to $201.7 billion in the same time frame.

Overall, banks still held the highest volume of loans. However, they had a slight drop from $368.3 billion in Q4 2017 to $368.2 billion in Q4 2018.

Average Credit Scores Continue to Rise as Market Growth Continues

A positive trend that continued in Q4 2018 is increases in average credit scores for borrowers. Average used scores increased two points from Q4 2017 to Q4 2018, from 713 to 715, while average scores for used vehicles saw a three-point increase in the same period, from 656 to 659. Credit scores can be an indicator of consumers doing their due diligence and taking steps to actively improve their credit.

The past several years have seen a steady boom in the automotive finance market as total lending volumes have consistently reached record levels. But vehicle affordability continues to present a potential challenge for the industry. Can consumers sustain such large increases in vehicle payments?

Overall, many indicators signal relative stability in the market. Despite rising automotive loan amounts and monthly payments, the data shows consumers appear to be making their payments on-time, though lenders will want to continue to keep a close eye on all facets of car buyers’ payment performance moving forward.

When looking at the market, context is key. A clear understanding of these trends will better position lenders to make the right decisions when analyzing risk and provide consumers with comprehensive automotive financing options. For now, the market continues to move along at a healthy clip. That’s good news for lenders, automakers, and consumers alike.

Melinda Zabritski serves as senior director of automotive credit for Experian Automotive. Email her at melinda.zabritski@bobit.com.

More Auto Finance

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →