Tracking F&I Performance

The magazine’s reader survey reveals that average profit per new vehicle retailed still hovers around $800, and that F&I managers are averaging approximately two products per deal.

In an informal study, the magazine sought to benchmark F&I performance last year, and asked readers in October to provide their performance data for the first three quarters of 2011. Results showed that F&I managers performed slightly better than the year-ago period.

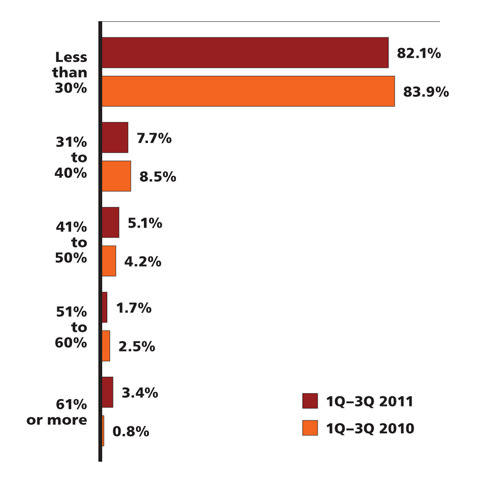

The average interest rate during the reporting period stood at 4.84 percent (median was 4.90 percent). Readers also listed Chase, Ally, Wells Fargo, Fifth Third Bank, Capital One, Bank of America, US Bank and TD Auto Finance as their top finance sources.

As for F&I tools used, 89.2 percent of respondents said they use a menu, while 48.6 percent said they also used electronic rating capabilities. As for electronic contracting of F&I products, 36.2 percent said they e-contract, while 35.2 percent said they’ve never used electronic contracting and rating tools.

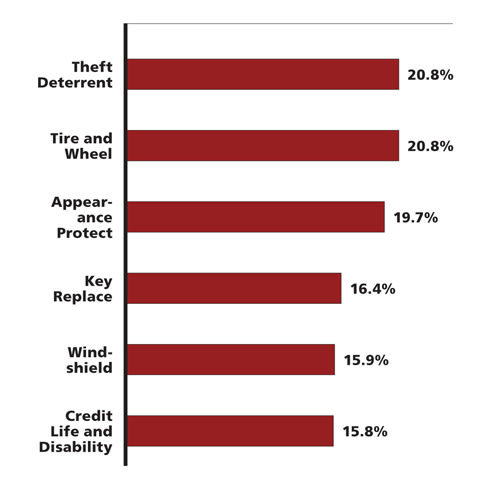

As for acceptance rates, GAP, prepaid maintenance and service contracts made slight gains from the year-ago period, with respondents averaging about 2.09 products per deal (median was 2 products per deal). Theft-deterrent products and tire-and-wheel protection also penetrated well for respondents, with most other products recording acceptance rates below 20 percent.

This snapshot of F&I performance shows that while auto finance continued to loosen up, there were some restrictions. But it appears finance sources are more welcoming of F&I products.

(Click charts for larger image)

1. What Is Your Average Profit Per Retail Unit?

The average profit per new vehicle sold was $804.82, compared to $883.05 for used. The median average profit per vehicle retailed for new was $875.50 vs. $1,000 for used.

2. What Is Your GAP Penetration Rate?

The average acceptance rate for GAP among respondents was 34.9 percent for the first three quarters of last year vs. 32 percent for the first three quarters of 2010.

3. What Is Your Vehicle Service Contract Penetration Rate?

The average acceptance rate for service contracts increased from 35 percent for the first three quarters of 2010 to 46 percent for the first three quarters of last year.

[PAGEBREAK]

4. What Is Your Prepaid Maintenance Penetration Rate?

Customers accepted prepaid maintenance plans at a 21 percent clip for the first three quarters of 2011 vs. 19.1 percent for the same period in 2010.

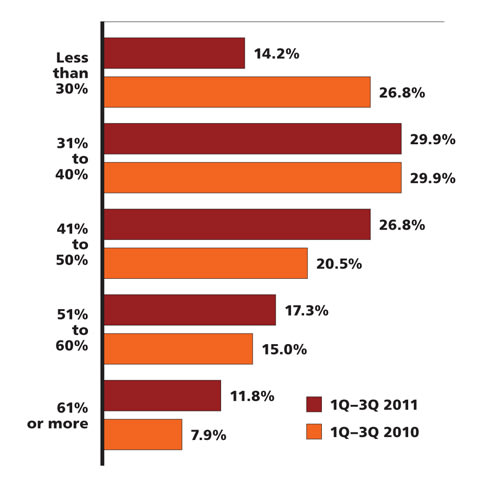

5. What Is Your Penetration Rate for All Other Products?

Theft-deterrent products and tire-and-wheel led the way for F&I managers last year, with appearance protection falling just below the 20 percent penetration mark.

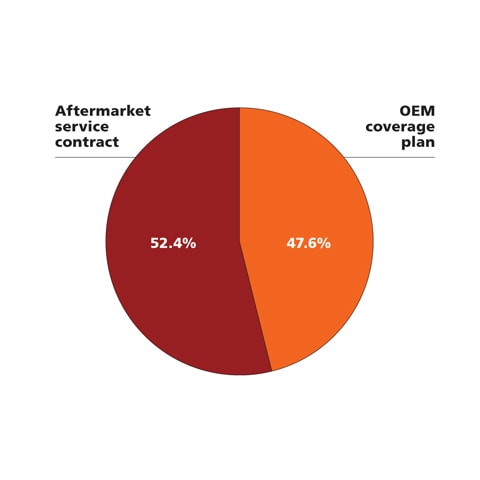

6. Which Sell Better, Aftermarket VSCs or Your OEM’s Coverage Plan?

The disparity between aftermarket VSC plans and OEM plans wasn’t much. In last year’s study, 54 percent of respondents said aftermarket plans sold better vs. 46 percent for captive plans.

7. What Types of Plans Are You Currently Selling?

The breakdown virtually mirrored what was recorded in last year’s study, which had 91.4 percent of respondents indicating that they offer bumper-to-bumper plans.

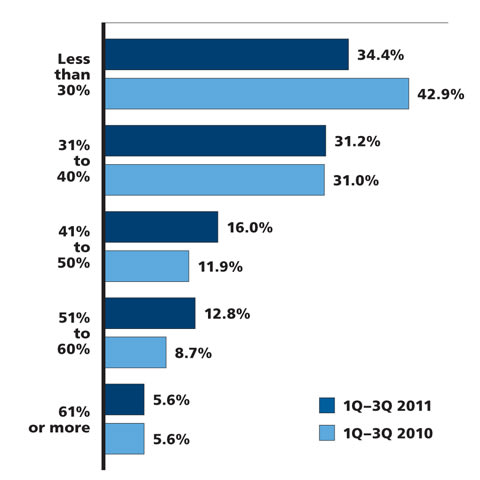

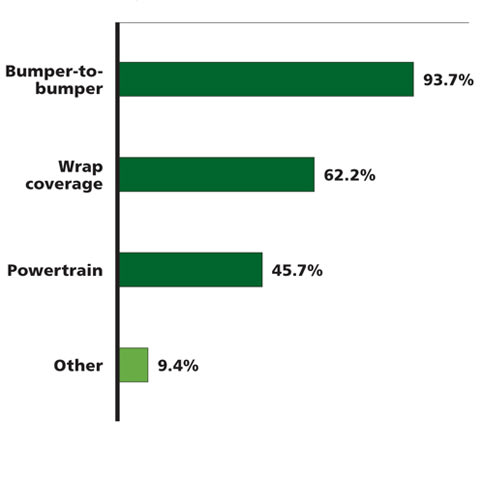

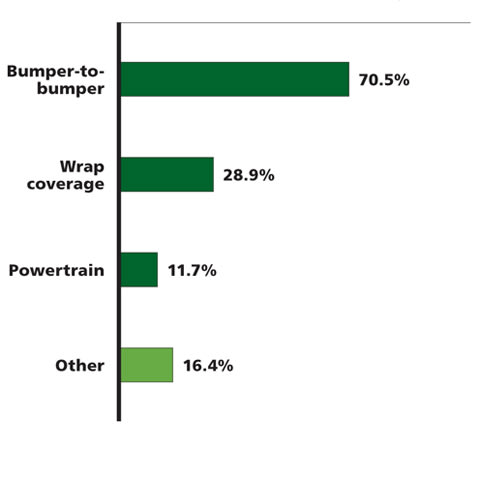

8. What Is Your Penetration Rate for Each Type of Plan?

The percentages were virtually identical to what was recorded in last year’s study, although powertrain acceptance rates dropped from 17.1 percent to 11.7 percent this year.

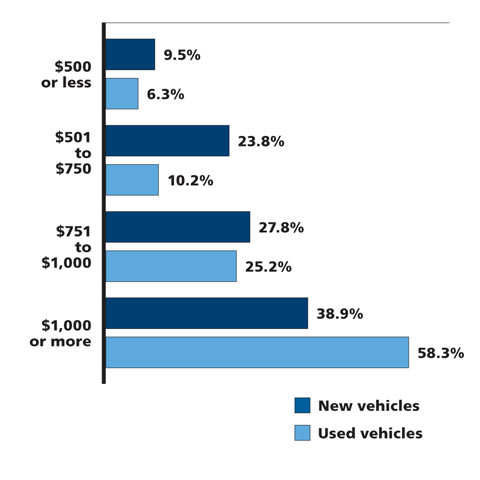

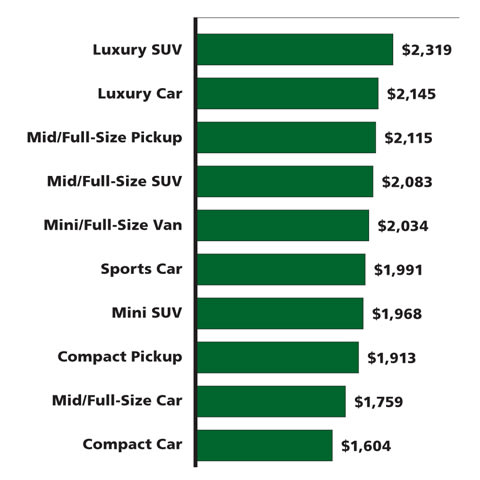

9. What Is the Average VSC Price New-Car Customers are Paying?

The study also asked readers about popular terms. Five-year, 100,000-mile plans led the way for new, followed by six-year, 75,000-mile and seven-year, 100,000-mile plans.

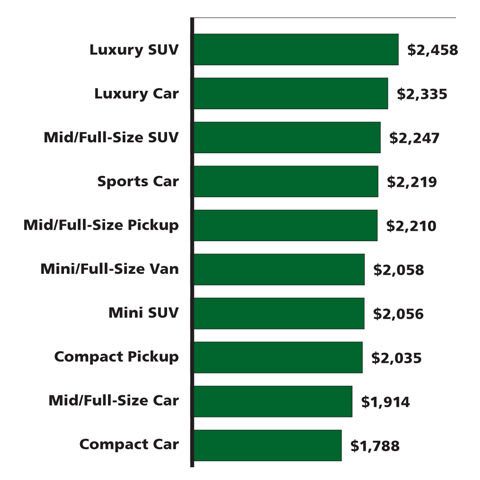

10. What Is the Average VSC Price Used-Car Customers are Paying?

The study also looked at popular terms for used. Three-year, 36,000-mile plans led the way, followed by four-year, 48,000-mile and five-year, 100,000-mile plans.

More Auto Finance

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →