Tracking the 2008 Credit Crisis

By the end of 2008, more than $7 billion worth of automotive loans were 60 days delinquent. Experian market analyst tracks the single-most challenging year for auto finance and provides her take on the road ahead.

Marked by slumping vehicle sales, deteriorating credit quality, increases in delinquencies, and a lack of funding availability, 2008 was the single-most challenging year for the automotive finance industry. This month’s quarterly trend report traces when things went wrong and peers into the challenges ahead for automotive dealers and their F&I departments.

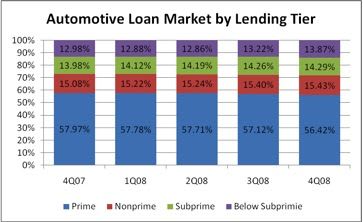

Distribution of Automotive Loans by Lending Tier

Providing a snapshot of the challenges faced last year is the shift in credit quality among all open automotive loans from the first to fourth quarter. Throughout 2008, the percentage of consumers considered prime steadily decreased. By the end of 2008, 56.42 percent of consumers with automotive loans were considered prime. Although still representing more than half of the market, this sector experienced a year-over-year decrease of 2.7 percent.

All of the high-risk tiers experienced year-over-year growth. The most significant increase was in the below subprime tier, which grew 6.85 percent from the fourth quarter 2007.

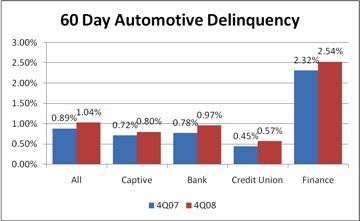

60 Days Past Due Delinquency Rate

Delinquency increases are one of the leading causes of consumer credit shifts. It is also one of the most significant data points on which lenders focus, as it guides credit programs available to dealers.

By the end of 2008, more than $7 billion worth of automotive loans were 60 days delinquent. While delinquency trends are cyclical and tend to increase throughout the year, the greatest quarterly increase occurred between the third and fourth quarters. During that period, the industry realized an end-of-year jump of 8.28 percent. In a year-over-year comparison, the 60-day delinquency rate rose 16.92 percent to 1.04 percent.

While having the lowest 60-day delinquency rate, credit unions experienced the greatest increases. The segment experienced a 28.22 percent year-over-year increase, bringing its 60-day delinquency rate to 0.57 percent.

The second-lowest delinquency rate was held by captive lenders, which ended the year with 0.8 percent of all loans reported 60 days delinquent. This was an increase of 11.98 percent from the fourth quarter 2007.

Banks, which typically have risk portfolios similar to credit unions, experienced the second-highest increase from the fourth quarter 2007 (24.79 percent), resulting in a 60-day delinquency rate of 0.97 percent.

Finance companies recorded the highest 60-day delinquency rate among all segments. These lenders typically have loan portfolios with significantly more high-risk consumers, which is why their 60-day delinquency rate stood at 2.54 percent. Despite this high rate of delinquency, the segment did record the lowest annual increase in delinquency rate at 9.37 percent.

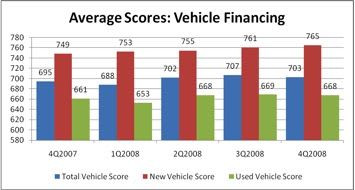

Credit Scores by Vehicle Type

While delinquency rates increased and credit quality decreased across the entire automotive loan market, loans originated in 2008 had higher credit scores. The average credit score for all vehicles financed in the fourth quarter increased 15 points from the beginning of the year, and eight points on a year-over-year basis.

New-vehicle financing saw average scores increase 12 points from the beginning of the year and 16 points on a year-over-year basis. Used-vehicle financing experienced an increase in credit scores of 15 points from the beginning of the year and seven points on a year-over-year basis. However, the segment saw little change in scores in the second half of 2008.

[PAGEBREAK]

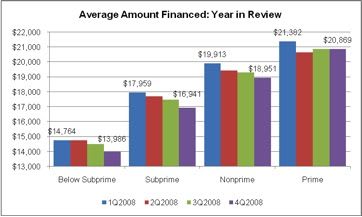

Average Amount Financed

As credit improves, so does the average loan amount financed. On average, consumer finance amounts stood at $19,671 in the fourth quarter, a decrease of $409 from the first quarter of the year.

Below subprime, subprime and nonprime loans all saw steady decreases in the average amount financed throughout the year. The most significant decrease was in the subprime risk tier, which fell $1,018 to an average loan amount of $16,941. Nonprime consumer loans fell $962 to an average loan amount of $18,951. Below subprime loans had the lowest amount financed of $13,986, a decrease of $778. Prime financing decreased $513 to an average loan amount of $20,869.

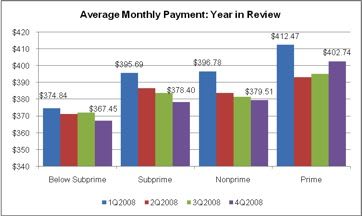

Average Monthly Payments

Average monthly payments on vehicles financed in 2008 also decreased throughout the year. Subprime loans ended the year with an average payment of $378.40, a decrease of $17 from first quarter 2008. Nonprime loans experienced a $17 decrease, ending the year with an average payment of $379.51.

The lowest monthly payments, $367.45, were found among below subprime loans. Compared to the first quarter, payments for this segment were $7 lower by the year-end quarter. Prime consumers had the highest monthly payments of all risk tiers at $402.74. However, monthly payments for this tier fell $10 from the first quarter of the year.

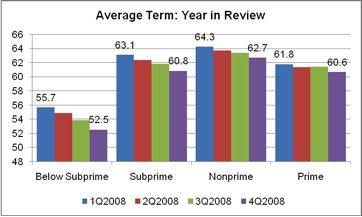

Average Term

While all risk tiers had an average loan term of 60 months in the fourth quarter 2008, each risk group saw decreases in monthly terms throughout 2008. Below subprime financing had an average loan term of 52.5 months in the fourth quarter, a decrease of 3.2 months from the first quarter 2008. Ending the year with an average term of 60.8 months, the subprime risk segment dropped 2.3 months from the first quarter — the second highest reduction of the year. Nonprime consumers had the longest terms at 62.7 months, which was a reduction of 1.6 months from the first quarter. Prime consumer loans saw a reduction of 1.2 months, ending the year with an average loan term of 60.6 months.

Overall

As credit quality shifted and delinquencies increased throughout 2008, lending programs changed significantly, resulting in an overall tightening of the automotive credit market. This was seen with increased credit scores on vehicle financing, along with reduced loan amounts and considerably lower terms.

Because of these shifts, the requirements of the F&I desk have definitely changed. While lenders continue to evolve their loan programs, dealers will continue to face challenges in obtaining financing for their consumers. While financing is still available for high-risk consumers, dealers need to be more aware of their lenders’ changing programs, as well as finding lenders still originating across a wide credit spectrum.

Melinda Zabritski is the director of automotive credit for Experian Automotive. She can be reached at melinda.zabritski@bobit.com.

More Auto Finance

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →