Black Book: Market Insights Report

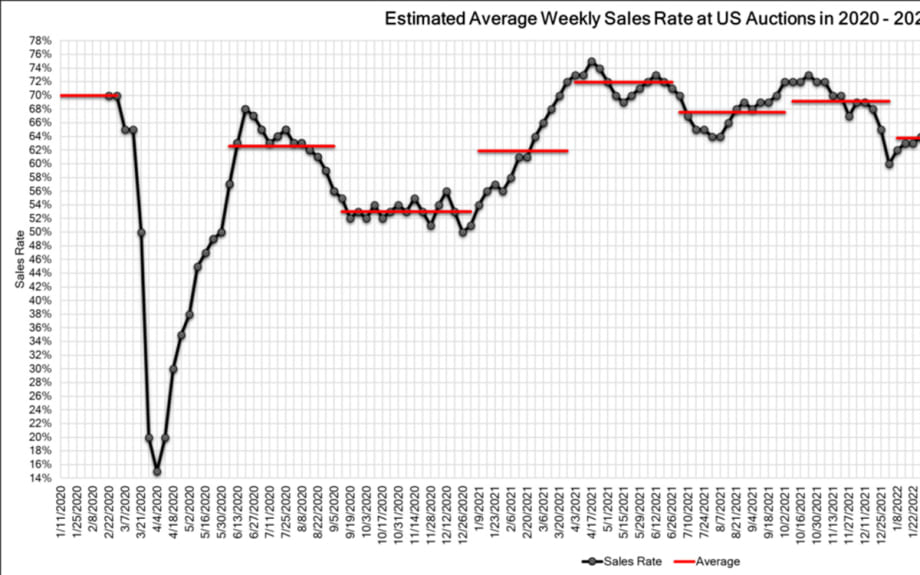

The Estimated Average Weekly Sales Rate dropped to 53% last week.

The Estimated Average Weekly Sales Rate dropped to 53% last week.

Wholesale Prices, Week Ending November 5th

Declines continued to be large last week, although overall, they were slightly less than the prior week’s adjustments. Many Car segments are experiencing some of the largest declines we’ve seen since the early days of the pandemic. Looking back however, Compact Cars experienced record level increases during the pandemic and went higher as fuel prices shot up earlier this year, so while the declines are large now, the values still remain well above pre-COVID levels.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -1.28% -1.47% -0.79%

Truck & SUV segments -0.94% -1.05% -0.60%

Market -1.05% -1.19% -0.67%

Car Segments

On a volume-weighted basis, the overall Car segment decreased -1.28%. For reference, the previous week, cars decreased by -1.47%.

All nine Car segments decreased last week, and six of the nine had declines greater than -1%.

The Car segments have declined on average -1.19% per week over the last four weeks.

Mid-Size Car had the largest decline at -1.63%. Full-Size (-1.46%), Compact (-1.45%), and Sub-Compact (-1.44%) were not far behind.

The luxury segments reported smaller declines than the mainstream segments. Premium Sporty Car had the smallest decline at -0.44%, followed by Near Luxury Car at -0.95%.

Truck / SUV Segments

The volume-weighted, overall Truck segment decreased -0.94%, compared with the prior week’s decline of -1.05%.

All thirteen Truck segments reported declines last week. Seven of the nine segments had declines greater than 1%.

Full-Size Van (-0.15%) continues to experience minimal declines. The segment is averaging a decline of only -0.17% per week over the last 4 weeks, compared to the overall Truck market, which is averaging -0.84% for the same period.

The Minivan segment had a second consecutive week of large declines, at -1.56%, compared with the prior week’s -2.50% drop.

Weekly Wholesale Index

Calendar year 2020 and 2021 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the last two years. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 did not have typical seasonality patterns as the market had rapid increases in wholesale values for the majority of the year. The Wholesale Weekly Price Index reached the highest point of the year at the end of December 2021, reporting over 1.51 points.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Retail (Used and New) Insights

After unveiling the Air Sapphire performance edition in August, Lucid is now planning to launch the Air Pure this month, starting at $89,050.

Ford is expanding their lineup with the new 2023 Transit Trail, which is expected to be customizable and targets the van-life market; this new variant starts at just over $65,900.

Tesla announced that production of its Cybertruck will begin mid-2023 at their Austin, Texas plant. Updated pricing has not yet been announced.

The SEMA (Specialty Equipment Market Association) Show was last week, and vehicle manufacturers did not disappoint, with the unveiling of the Dodge Charger Daytona EV, Ford F-150 Lightning with solar charging, and Volkswagen’s Basecamp concepts, among others.

The European Union has come to an agreement to completely phase out the sale of gas and diesel-engine cars and vans by 2035 – now the agreement needs to be adopted by the European Parliament and Council. Trucks were not included in this agreement.

Used Retail Prices

Used Retail Prices are more accessible than in years past, due to the proliferation of ‘no-haggle pricing’ for used-vehicle retailing. Transparent pricing upfront makes the car buying process more enjoyable for customers and allows Black Book to accurately measure retail market trends.

At the on-set of the pandemic, in CY2020, used retail prices increased slightly, following typical seasonal patterns, and then began dropping in April, finally hitting a low point in the late spring months. By late summer of CY2020, Used Retail Prices increased as supply of new vehicle inventory started to become scarce, but retail demand slowed down at the end of CY2020, resulting in declining retail asking prices for the last several weeks of the year. When CY2021 kicked off, demand rebounded while retail prices lagged slightly behind wholesale prices; March of 2021 started the dramatic increases in Used Retail Prices, fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up the pace once again to start the fourth quarter. In Q4, prices on retail listings steadily increased week after week. As CY2021 came to an end, the retail listing price index closed 36% above where the year began.

Now, in the fourth quarter of 2022, the Retail Listings Price Index has started to decline, but not as steep as the wholesale price index.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graph below looks at 2-6-year-old vehicles. The Index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

Used retail active listing volume increased to 1.15, following a similar trend from 2019.

The Used Retail Days-to-Turn estimate is just under 42 days.

Wholesale

With Halloween now behind us, as we move through November, auction activity seems to still be rather slow. Buyers are still showing up in expected numbers, but the average floor prices remain high. Franchise dealers were unphased by the high floors however, and took control of the lanes last week, showing very competitive activity. Rental companies were noticeably absent along with the large independent dealers. The absence of the large independent dealers and rental companies did not affect sales rates, as they are still continually slowly decreasing. There were lots of if sales, which contributed to the ever-declining sales rates. It seems like buyers still have hope that the market is coming down and that sellers may be more willing to negotiate. Sellers may be holding their vehicles due to low inventory, but if they can negotiate, it is a win for both the buyer and seller. Inventory is still down, and the condition grades of offered vehicles have been lower than normal. Overall, the wholesale market is still following a downward trend.

The Estimated Average Weekly Sales Rate dropped to 53% last week.

Originally posted on Auto Dealer Today

More Auto Finance

Subaru Enters Lending Business

The automaker follows other brands in adding captive financing in the U.S., and says the move will strengthen its position here.

Read More →

Positive Equity Reaches Record High

Mainstream vehicle owners who bought a car seven years ago are likely to have positive equity when trading in for a new vehicle, according to second-quarter Edmunds data.

Read More →

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →