Black Book: Weekly Market Insights

The Mid-Size Car segment had the largest decline last week, at -0.76%, compared with the prior week’s decline of -0.64%, marking the third consecutive week the segment has reported the largest segment decline.

The Mid-Size Car segment had the largest decline last week, at -0.76%, compared with the prior week’s decline of -0.64%, marking the third consecutive week the segment has reported the largest segment decline.

BLACK BOOK – Wholesale Prices, Week Ending February 5th

The declines accelerated last week with all segments, except Full-Size Vans, reporting decreasing values. Buyer attendance at auctions remains strong, but bidding activity is slowing as dealers are reporting weaker consumer demand for used vehicles.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -0.53% -0.35% -0.32%

Truck & SUV segments -0.47% -0.34% -0.40%

Market -0.49% -0.34% -0.37%

Car Segments

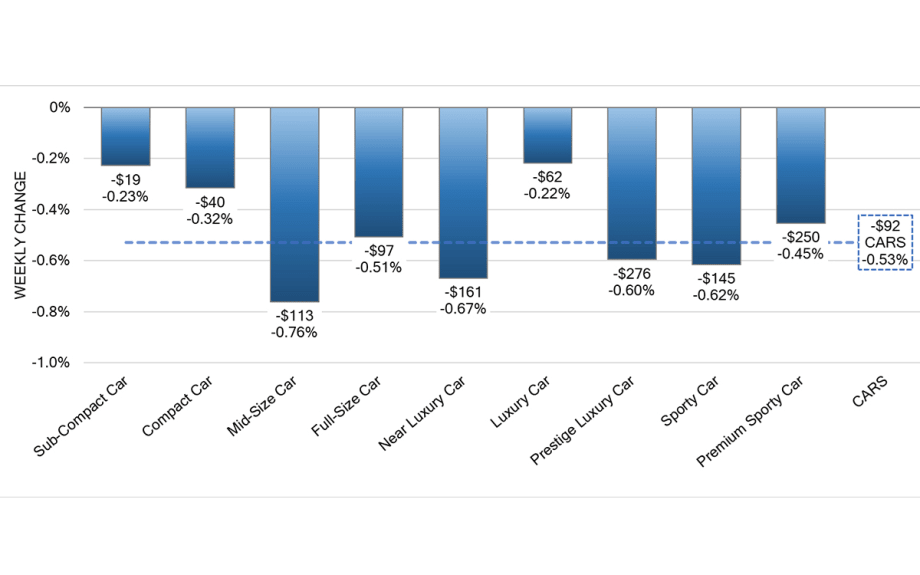

On a volume-weighted basis, the overall Car segment decreased -0.53%. For reference, the previous week, cars decreased by -0.35%.

All nine Car segments declined last week.

The Mid-Size Car segment had the largest decline last week, at -0.76%, compared with the prior week’s decline of -0.64%, marking the third consecutive week the segment has reported the largest segment decline.

Sub-Compact Cars previously had three consecutive weeks of increases, leaving us wondering if that was an early sign of the spring market, but the segment reversed direction last week and declined -0.23%.

Truck / SUV Segments

The volume-weighted, overall Truck segment decreased -0.47%, compared to the prior week’s decrease of -0.34%.

Twelve out of the thirteen Truck segments reported declines.

Full-Size Vans (+0.53%) reported another increase last week, but the rate of gain slowed compared to the prior week’s increase of 1.36%.

Sub-Compact and Compact Crossovers had the largest declines, -0.90% and -0.86%, respectively.

Minivans ended their twenty-five-week streak of increases with a decline of -0.30%.

Weekly Wholesale Index

Calendar year 2020 and 2021 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the last 2 years. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 did not have typical seasonality patterns as the market had rapid increases in wholesale values for the majority of the year. The Wholesale Weekly Price Index reached the highest point of the year at the end of December, reporting over 1.51 points. Now in calendar year 2022, the index has been reverted back to the 1.00 mark and overall wholesale prices have remained relatively stable in the month of January and into the beginning of February (green line).

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Retail (Used and New) Insights

GM announced that they will discontinue the Chevrolet Spark – their smallest offering – after this summer, but the brand has racked up over 110,000 reservations for the upcoming Chevrolet Silverado battery electric truck, scheduled to arrive next year.

Ford will be partnering with Google to use their cloud-based technological services at the Ford mobility innovation campus – Michigan Central.

The semiconductor chip shortage continues to be an issue with several manufacturers making cuts this week. According to AutoForecast Solutions, the number of vehicles trimmed from production plans worldwide has surged 61% from a week earlier. Subaru downgraded their global sales outlook again, now at 740,000 vehicles from the original 1.0 million planned. Ford will suspend or cut production at 8 NA assembly plants affecting the F-150, Range, Bronco, Explorer, and Mach-E.

Used Retail Prices

Used Retail Prices are more accessible than in years past, due to the proliferation of ‘no-haggle pricing’ for used-vehicle retailing. Transparent pricing upfront makes the car buying process more enjoyable for customers and also allows Black Book to accurately measure trends in the retail space.

During the on-set of the Covid-19 pandemic in CY2020, used retail prices increased slightly, following typical seasonal patterns, and then began dropping in April, finally hitting a low point in the late spring months. By late summer of CY2020, Used Retail Prices increased as supply of new vehicle inventory started to become scarce, but retail demand slowed down at the end of CY2020, resulting in declining retail asking prices for the last several weeks of the year. As CY2021 kicked off, demand rebounded while retail prices lagged slightly behind wholesale prices; March of 2021 started the dramatic increases in Used Retail Prices, fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up the pace once again to start the fourth quarter. In Q4, prices on retail listings steadily increased week after week. As CY2021 came to an end, the retail listing price index closed 36% above where the year began.

Now, in calendar year 2022, the index has been reverted back to the 1.00 mark. In the first part of 2022, the Retail Listings Price Index remains relatively unchanged.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graph below looks at 2-6-year-old vehicles. The index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

Used Retail Listing Volume returned to where CY2022 began. We anticipate that used retail listings will increase in the coming weeks as dealers attempt to stock their lots.

Used Retail Days-to-Turn now sits just above 44 days, up 2 days from last week. While a spring market is still expected, it is worth noting that the Consumer Confidence Index fell in January with the short-term outlook for income, business, and labor market conditions declining from 95.4 to 90.8.

Wholesale

Auction sales continue to be hit or miss with witnessed sell rates ranging from 27% to 91% last week. Large independent dealers seem to be making a comeback in the lanes and not just the near-prime and subprime sellers. Their resurgence is a good sign for the upcoming spring market, although it adds additional competition among rental companies, smaller independents, and franchise dealers. It is still normal to see a portion of damaged vehicles in each sale and now repossessions have started to pop up a little more frequently. Wholesale values are waning, but floor prices are still being held high in hopes that scarcity in the market will entice buyers to make the leap.

The Estimated Average Weekly Sales Rate has dropped to 62% this week, down 2% from last week’s estimated average of 64%. If-sales have been more prevalent than usual. At this point in CY2021, we were at a similar place just before sales rates significantly increased, jumping from low-60% to mid-70% in a matter of weeks.

Originally posted on Auto Dealer Today

More Auto Finance

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →