Black Book: Weekly Market Report

Typically, the last week of the year is strong for retail sales, but this year with high interest rates and used vehicle prices on a steep downward decline so far this quarter, we will have to wait and see how the year finishes.

Typically, the last week of the year is strong for retail sales, but this year with high interest rates and used vehicle prices on a steep downward decline so far this quarter, we will have to wait and see how the year finishes.

Black Book Market Insights – 12/27/23

Wholesale Prices, Week Ending December 23rd

With the holidays in full-swing, activity at the auctions has slowed down as dealers await the 13th month of the year, that final week of the year. The success of the retail sales this week will say a lot about how the new year will start.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -0.51% -1.03% -0.58%

Truck & SUV segments -0.78% -1.06% -0.44%

Market -0.70% -1.05% -0.50%

Car Segments

On a volume-weighted basis, the overall Car segment decreased -0.51%. For reference, in the previous week, cars decreased by -1.03%.

The 0-to-2-year-old Car segments were down -0.52% and 8-to-16-year-old Cars declined -0.91%.

All nine Car segments decreased last week. For the first time in six weeks, none of the segments had depreciation exceeding 1%.

The Sub-Compact Car segment had the largest depreciation last week, declining -0.93%. This compares with the average weekly decline over the last six weeks of -1.29%.

The Compact Car segment had a dramatic decrease in depreciation, 0.30% last week compared with the prior week’s decline of -1.13%. This was the lowest single week depreciation for the segment since late October.

Truck / SUV Segments

The volume-weighted, overall Truck segment decreased -0.78% compared to the depreciation seen the prior week of -1.06%.

The 0-to-2-year-old models declined -0.73% on average and the 8-to-16-year-olds decreased by -0.85% on average.

All thirteen Truck segments declined last week, with only four of the thirteen reporting declines exceeding 1%.

The Compact Crossover/SUV segment had the smallest depreciation last week, declining -0.48%, compared with -0.96% the previous week.

The Sub-Compact Luxury Crossover/SUV segment had the largest decline last week, dropping -1.28%. The segment has averaged a decline of -1.33% per week over the most recent eight weeks.

Weekly Wholesale Index

The graph below looks at trends in wholesale prices of 2 to 6-year-old vehicles, indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Used Retail Prices

Used Retail Prices are more accessible than in years past, due to the proliferation of ‘no-haggle pricing’ for used-vehicle retailing. Transparent pricing upfront makes the car buying process more enjoyable for customers and allows Black Book to accurately measure retail market trends.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graph below looks at 2-6-year-old vehicles. The Index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

The Used Retail Active Listing Volume Index is now below where we started the year.

The Used Retail Days-to-Turn estimate is now sitting around 62 days.

Wholesale

The market was slowing down due to the holidays, with more people traveling and preparing to spend time with family and friends, and this was apparent as we saw auction conversion rates dropping last week. Typically, the last week of the year is strong for retail sales, but this year with high interest rates and used vehicle prices on a steep downward decline so far this quarter, we will have to wait and see how the year finishes. As always, our team of Analysts are focused on keeping their eyes on the market, watching for developing trends, and gathering insights.

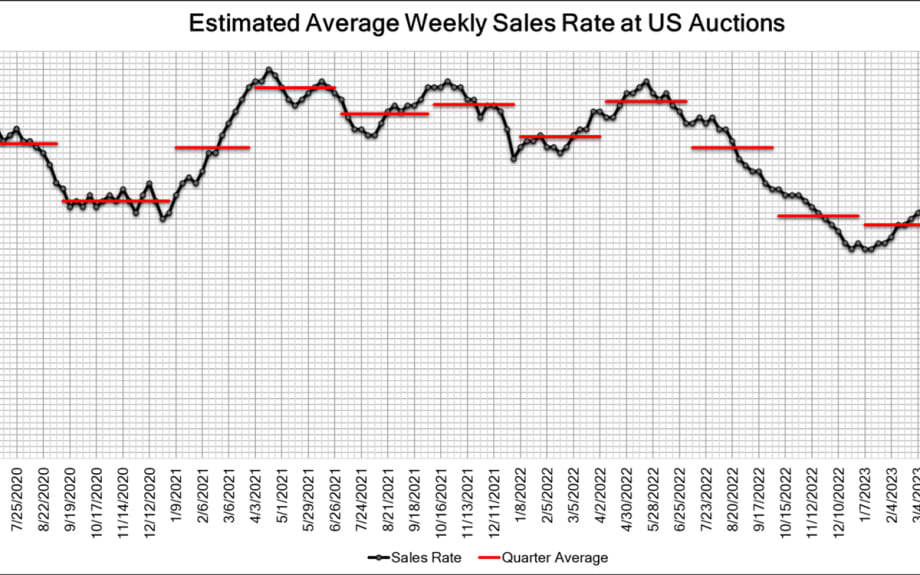

The estimated Average Weekly Sales Rate decreased to 52% last week.

Originally posted on Auto Dealer Today

More Auto Finance

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →