Cox Automotive: Wholesale Used-Vehicle Prices Unchanged in First Half of June From Seasonal Adjustment

Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) were essentially unchanged from May after the first 15 days of June.

Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) were essentially unchanged from May after the first 15 days of June.

Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) were essentially unchanged from May after the first 15 days of June. This kept the Manheim Used Vehicle Value Index at 222.7, which was up 11.1% from June 2021. The non-adjusted price change in the first half of June was a decrease of 0.3% compared to May, leaving the unadjusted average price up 12.4% year over year.

The last full two weeks covered the end of May, the Memorial Day holiday, and only the first 11 days of June, so the weekly trends were not as aligned with the half-month performance as is typically the case. Over the last two weeks, Manheim Market Report (MMR) prices saw accelerating declines. Over that time, the Three-Year-Old MMR Index, which represents the largest model-year cohort at auction, experienced a 0.6% cumulative increase. Over the first 15 days of June, MMR Retention, which is the average difference in price relative to current MMR, averaged 98.8%, which indicates that valuation models are slightly ahead of market prices. The average daily sales conversion rate of 53.1% in the first half of June declined relative to May’s daily average of 55.3% and has been lower than the typical conversion rate for this time of year. The latest trends in the key indicators suggest wholesale used-vehicle values should see declines in the second half of the month.

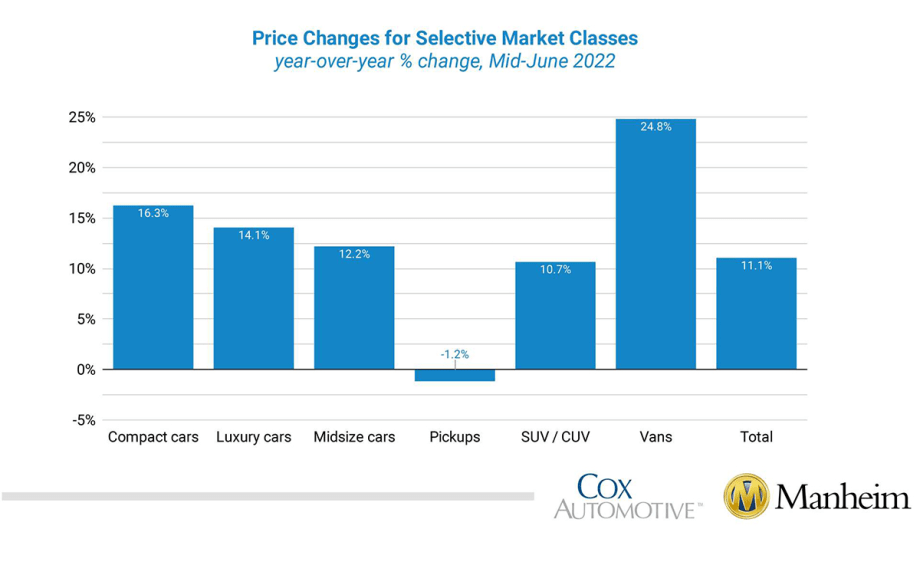

Most major market segments saw seasonally adjusted prices that were higher year over year in the first half of June. Pickups were the exception with a 1.2% decline year over year. Vans had the largest increase at 24.8%, and both non-luxury car segments outpaced the overall industry in seasonally adjusted year-over-year gains. Compared to May, most major segments saw lower performance, except for compact and full-size cars, up 0.5% and 19.9%, respectively. The seasonal adjustment drove the declines, with SUVs having no change from May, while midsize cars and pickups dropped 1.1%.

Retail and wholesale at normal levels in first half of June. Using estimates based on vAuto data as of June 13, used retail days’ supply was 45 days, which was down one day from the end of May. Days’ supply was up seven days year over year. Leveraging Manheim sales and inventory data, we estimate that wholesale supply ended May at 24 days, down one day from the end of April but up five days year over year. As of June 15, wholesale supply was at 25 days, up one day from the end of May and up five days year over year.

Rental risk prices increase. The average price for rental risk units sold at auction in the first 15 days of June was up 30.3% year over year. Rental risk prices were up 1.2% compared to the full month of May. Average mileage for rental risk units in the first half of June (at 59,400 miles) was down 31.6% compared to a year ago and down 6.5% month over month.

Consumer Sentiment declines to start June. The initial June reading on Consumer Sentiment from the University of Michigan declined 14% to 50.2, which was a record low for the index. Consumers’ views of both current conditions and future expectations declined substantially, and the expected inflation rate increased to the highest level since 2008. Consumers’ views of buying conditions for vehicles declined to the lowest reading in the history of the survey dating back to 1978. The daily index of consumer sentiment from Morning Consult also declined in the first half of June. As of June 15, the index was down 5.1% compared to May 31 and was at a new low for the index.

Originally posted on Auto Dealer Today

More Auto Finance

Dealerships Are Paying the Price for Extended Car Loans

Growing negative-equity scenarios mean such lengthy terms should be addressed in a forward-looking way to make them work for the dealer and the consumer down the road.

Read More →

Trade-Ins in Negative Equity Reach New Heights

As such trade-ins rise in frequency, so do monthly loan payment amounts and interest rates, according to second-quarter data compiled by Edmunds.

Read More →

Auto Credit Plentiful

June numbers show lenders are readily granting access, including to risky borrowers, as consumers leverage themselves to take on high prices.

Read More →

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →