With New-Vehicle Prices Climbing in April, Affordability Declines Further

New-vehicle affordability declined slightly in April despite revised data indicating stronger income gains, according to the latest Cox Automotive/Moody’s Analytics Vehicle Affordability Index.

New-vehicle affordability declined slightly in April despite revised data indicating stronger income gains, according to the latest Cox Automotive/Moody’s Analytics Vehicle Affordability Index.

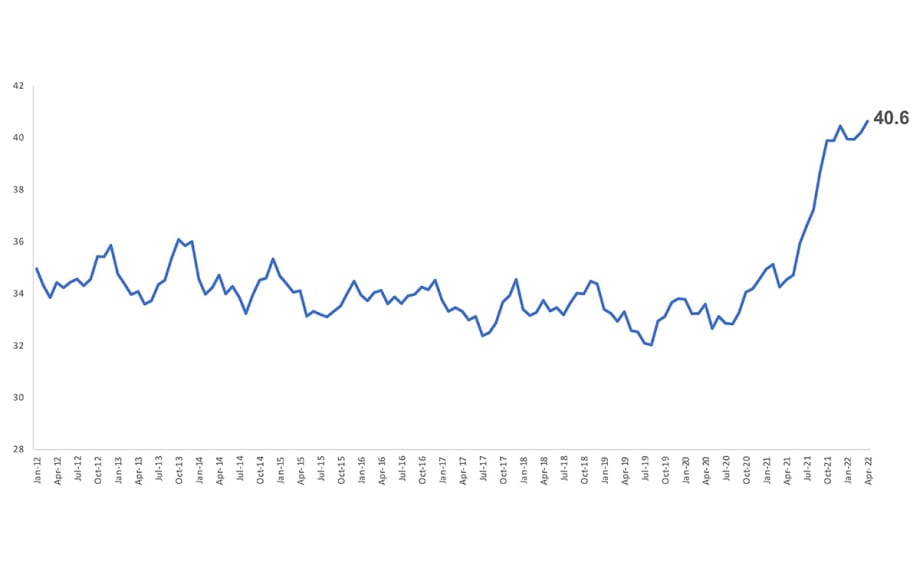

COX AUTOMOTIVE – New-vehicle affordability declined slightly in April despite revised data indicating stronger income gains, according to the latest Cox Automotive/Moody’s Analytics Vehicle Affordability Index. The inputs to the index again moved in differing directions in the month. The number of median weeks of income needed to purchase the average new vehicle in April increased to 40.6 weeks from a downwardly revised 40.2 weeks in March.

COX AUTOMOTIVE/MOODY’S ANALYTICS VEHICLE AFFORDABILITY INDEX: APRIL 2022

Supporting affordability, median income in the U.S. grew 0.3% in April The revisions in the data for prior months were driven by updated data from the 2020 American Community Survey’s median household income estimates. The revisions to that data show income growth higher than previous estimates used to infer more recent median income data.

All other factors moved against affordability last month. The price paid moved 0.7% higher, due in part to incentives declining further. The average interest rate on a new-vehicle loan increased another 20 basis points. As a result of these moves, the estimated typical monthly payment increased 1.4% to $698, which was a new record high.

Even with the data revisions, the top-line story remains the same. New-vehicle affordability continues to be much worse now than a year ago when prices were notably lower and incentives were higher. The estimated number of weeks of median household income necessary to purchase the average new vehicle in April was up 18% from last year.

The next update of the Cox Automotive/Moody’s Analytics Vehicle Affordability Index will be published on June 15, 2022.

Originally posted on P&A Magazine

More Auto Finance

Automotive Consumers Sink Further in Debt

Most financing metrics hit records in the second quarter as more buyers locked themselves into long terms and high monthly payments.

Read More →

Porsche Financial Services Shifts Structure

After 36 years with Porsche, the Financial Services Chief Financial Officer Konrad Riedl is retiring, and the department is realigning its management structure.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →