J.D. Power: Wholesale Prices Decline in August

Wholesale prices of used vehicles up to eight years in age fell by 1.2% in August. Over the past five years, however, losses for the period averaged a more significant 2.2%.

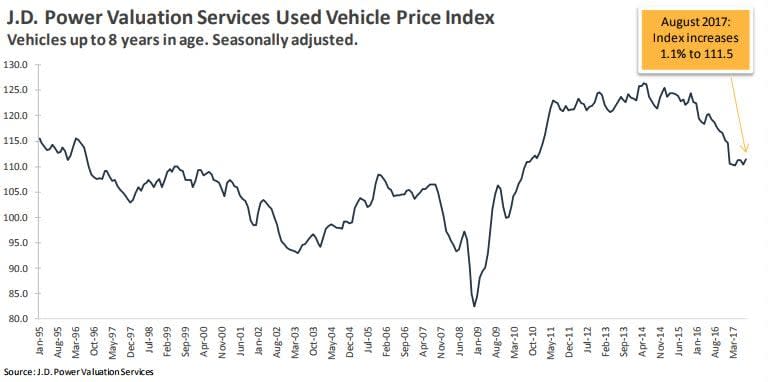

MCLEAN, Va. — J.D. Power’s Seasonally Adjusted Used Vehicle Price Index registered its largest increase in August since May 2016, rising 1.1% to 111.5. That’s 7.2 points lower than August 2016’s 118.7 reading.

According to the firm’s “Used Car and Light Truck Guidelines,” wholesale prices of used vehicles up to eight years in age fell by 1.2% in August. Over the past five years, losses for the period averaged a more significant 2.2%. The lower-than-expected decrease led to the index’s 1.1% increase, closing the year-over-year deficit to 7% vs. the 7.5% year-over-year deficit recorded in July.

“At the segment level, mainstream car segment losses led the industry in August. Similar to July’s month-end result, large car prices fell by 2.6% last month,” the firm stated in its report. “While sizeable compared to the rest of the industry, large car declines were typical for the period, nearly matching the segment’s five-year average decline of 2.4%.”

Following close behind, mid-size van losses reached 2.1% in August. For comparison, the segment experienced smaller declines in value of 1.6% and 1% for the periods in 2015 and 2016, respectively. Remaining mainstream segment losses were all less than what typically occurs for the period.

Compact and mid-size utility prices each fell by 1.3%, down from the pair’s 1.6% five-year average for the period. “As for cars, subcompact, compact, and midsize car prices fell by a combined average of 0.8%, which is significantly better than the group’s five-year average decline of 2.4% in August,” the firm stated in its report. “It’s also worth noting that August’s small and midsize car price losses were the lowest recorded in 2017, aside from March where each increased by a combined average of 3%.”

Mid-size pickup and large utility prices slipped by 0.5% and 0.4%, respectively, which was about 0.5-point better than each segment’s five-year average for the period. The only mainstream segment to experience a price lift in August was large pickups.

“Prices for truck segments continue to be exceptionally strong,” the firm noted. “In particular, large pickup prices have increased for three straight months, the segment’s best showing for the period since 2011.”

On the premium side, luxury large utility (down 2.3%) and luxury midsize car (down 2.2%) losses led price declines in August. Luxury cars, which were up 0.4%, experience their first positive August result since 1998, while remaining premium segment losses were less than what typically occurs for the period.

Looking at auction volume trends, late-model vehicle volume (units up to three years old) in August reached 257,831 units, which is 21.8% more than July’s 211,632 units. Late model volume now sits at 1.944 million units through the first eight months of 2017. In comparison, late-model volume in 2016 sat at a lesser 1.823 million units.

At the segment level year to date, some of the largest volume increases occurred in the truck and SUV segments. Luxury compact utility volume is up 55.3%, followed by a 42.7% increase among mid-size pickups. On the opposite end of the spectrum, luxury midsize car volume has declined 19.6%, and large car volume is down 14.2% so far for the year.

“In terms of volume share, used cars continue to dominate at 54% of the market while truck share lags behind at 46%, which is a reversal of what’s occurring on the new vehicle side of the market,” the firm noted.

Looking at September, wholesale prices of vehicles up to eight years in age are expected to decline by approximately 1.8%. September’s expected loss is significantly less than the 3.4% drop recorded during the period in 2016. The pre-Hurricane Harvey/Irma forecast had prices down 2.8%, however, the reduction in supply and anticipated increase in demand led to the one-point improvement in the September forecast.

“At the segment level, car losses are still excepted to outpace those of trucks and SUVs,” the firm stated in its report. “Midsize and large pickups continue to perform well and are forecast to outperform the industry average. Losses for all premium segments are forecast to fall by slightly more than the industry average for the month.

“In terms of full-year expectations, used prices are expected to decline by 6.2% in 2017. The year’s anticipated result is about two points worse than 2016’s 4.1% loss,” the firm added. “Looking further out, losses in 2018 are expected to decelerate to around 3%.”

More Auto Finance

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →

Permission or Approval: When to Notify Finance Sources

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Read More →

At-Risk Auto Borrowers Drive Looser Credit Access

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Read More →

Auto Loan Forecast Bucks Market Trend

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Read More →

Auto Credit More Plentiful

Growing access shows greater lender appetite for risk as consumers take on heavier debt burden in an inflated market.

Read More →

Auto Loans Long as Stretch Limos

More consumers, faced with ever-rising car prices, are adapting by agreeing to longer loan terms despite the cost of added interest payments.

Read More →

AutoPayPlus Launches RePayPlus

The reinsured biweekly payment program offers auto dealers with customer retention and reinsurance structure.

Read More →