I am usually a guy who believes that if you get stale bread, you make toast instead of throwing the bread away. I know that today’s increasingly regulatory and litigious times continue to create compliance challenges. Implementing a compliance checklist can help to demonstrate your dealership’s commitment to transparency and compliance.

Elements of a Compliance Checklist

When putting your checklist together, consider the following elements.

ELEMENT #1: Two-people Review

The compliance checklist should be completed by the F&I Manager who completed the deal and reviewed by the Billing Clerk. This places the responsibility on the professional being paid the higher buck to say to the organization, “I did this deal right.” It also subconsciously says to the F&I Manager, “You are signing your name saying you did this deal right.” Just as the F&I Manager is the deal backstop to ensure Sales did its job correctly, the Billing Clerk is your control checkpoint to further help with your compliance.

ELEMENT #2: Areas to Review

In today’s environment, the three biggest risks dealers face today are credit application fraud, identity theft, and potentially deceptive practices including discriminatory pricing. The checklist should require the F&I Manager and the Billing Clerk to review items in your Sales and F&I processes that help you mitigate these risks and document your compliance with State, Federal, and Dealer laws. Some examples of items to include on a checklist:

Credit Application Process – The Federales remain vigilant in pursuing dealers for credit application fraud. A good compliance checklist will check to ensure the five key credit determinants (time on job, time at address, occupation, income, and housing expense) are consistent between the credit application received from the customer and the one your dealership submitted to the finance source. This can help mitigate your risk of an allegation of credit application fraud.

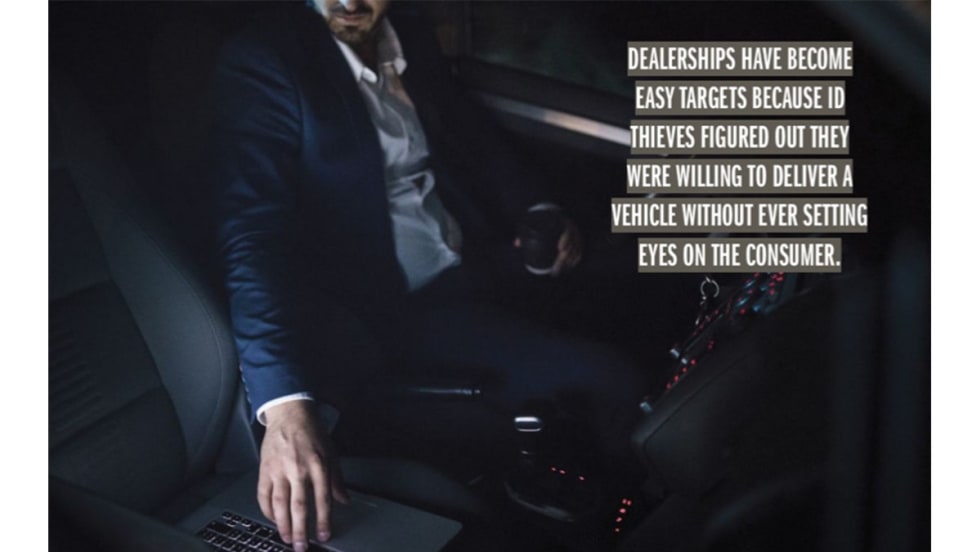

Know Your Customer – The Federales have at least five requirements that dealerships must demonstrate compliance with when it comes to knowing your customer. Four address identity theft (FTC Privacy Rule, FTC Safeguards Rule, FTC Disposal Rule, and FTC Red Flags Rule), while the fifth (OFAC) is designed to stop enemies of the state launder money. Additionally, a current, legible government issued ID must be in the file From a transactional perspective, the checklist must confirm any Red Flag or OFAC hit has been properly cleared on or before the date of delivery. Any third party down payments or trade must also be vetted against the OFAC list. Through the pandemic, many dealerships quickly implemented processes to sell and deliver vehicles to consumers who never stepped foot into the dealership. Known as digital deliveries, or out of area deliveries, identity thieves quickly jumped on some loopholes in processes that had not been well thought out. If your dealership continues to sell vehicles via a digital delivery process on some transactions, the requirements should be part of your checklist.

Transparent Paper Trail – Potentially deceptive sales practices or discriminatory pricing is easy to allege and difficult to defend. Often the allegations come months or years after the transaction and unless your manager has an incredible memory, she or he won’t remember the transaction. The defense must be the paper trail of documents that are executed in a standard financed deal. This paper trail includes desking worksheets, menu, contracts, and Voluntary Protection Product Registration forms. The checklist should require the reviews to confirm the prices and terms are consistent on every document.

Other Document Compliance – the Federales, or state agencies, or Dealer Law require dealerships to demonstrate compliance in many more areas such as a Used Car Buyer’s Guide, Credit Score Disclosure Notice, Privacy Notice, Prior History Disclosure, FINCen 8300, product pricing guidelines, finance source stips, and receipts to name a few. Your compliance checklist must both confirm the form is and file and it was properly completed.

Benefits of a Checklist

You must process the deal to get paid for the deal. The use of a checklist places the accountability on the F&I Manager to have the deal right when it gets to Accounting. This should reduce the number of times the deal is kicked back to Finance to get something right before billing the deal.

The effective use of a checklist improves the deal processing and can improve your CITs. The consistent use of a checklist will help with your compliance controls.

Continued Good Health, Good Luck, and Good Selling.

Gil Van Over is the Executive Director of Automotive Compliance Education (ACE), the Founder and President of gvo3 & Associates, and the author of Automotive Compliance in a Digital World.