Market Insights – 5/17/2022

Wholesale Prices, Week Ending May 14th

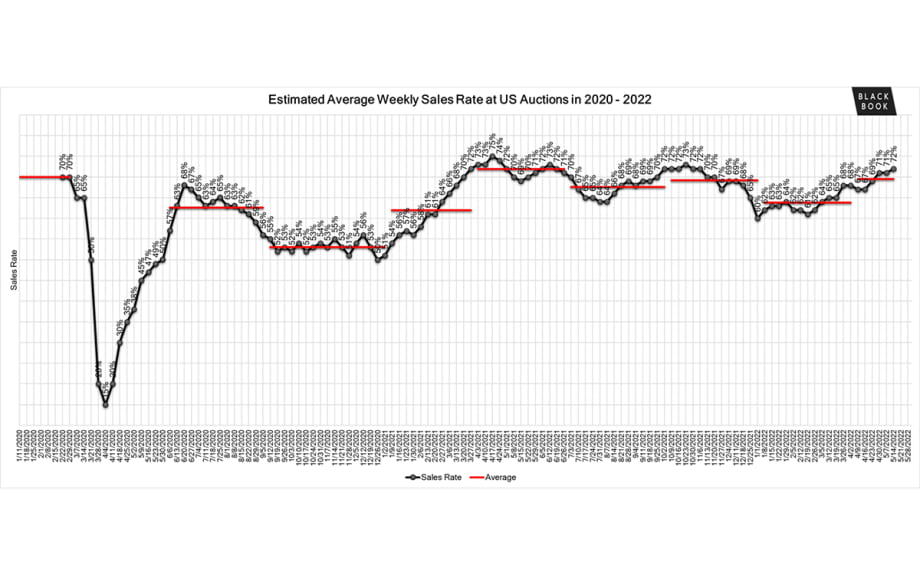

The Estimated Average Weekly Sales Rate continues to increase and now is at 72%.

The Estimated Average Weekly Sales Rate continues to increase and now is at 72%.

Market Insights – 5/17/2022

Wholesale Prices, Week Ending May 14th

Supply chain issues continue to push the “return to normal” new vehicle production levels well into 2023. With these developments, the wholesale price gains continued last week, with the overall market experiencing an acceleration in the positive price movement that started three weeks ago. One of the noteworthy segment changes was the return to positive territory for Full-Size Trucks, a first since the last week of 2021.

This Week Last Week 2017-2019 Average (Same Week)

Car segments +0.44% +0.31% -0.23%

Truck & SUV segments +0.10% +0.05% -0.18%

Market +0.21% +0.13% -0.20%

Car Segments

On a volume-weighted basis, the overall Car segment increased +0.44%. For reference, the previous week, cars increased by +0.31%.

Eight of the nine Car segments increased last week.

Compact Cars have now increased for eight consecutive weeks, for an average increase of +0.59%. Last week, the segment increased +0.92%.

Sporty Cars are finally feeling the effects of warmer weather with values increasing for the last 3 weeks, for an average weekly gain of +0.16%.

Premium Sporty was the only Car segment to decline last week, falling by -0.23%, compared to the prior week’s decline of -0.29%.

Truck / SUV Segments

The volume-weighted, overall Truck segment increased +0.10%, compared to the prior week’s increase of +0.05%.

Eight out of the thirteen Truck segments reported increases.

Full-Size Trucks (+0.08%) returned to increasing values last week, for the first time since the last week of December 2021.

With the exception of Sub-Compact Luxury Crossover, all other Luxury Crossover/SUV segments reported declines last week. Mid-Size Luxury Crossovers had the largest decline at -0.41%.

Full-Size Vans returned to increases last week, with a gain of +0.36%. With the exception of last week’s minimal -0.01% decline, the segment is nearing 70 weeks of increases.

Weekly Wholesale Index

Calendar year 2020 and 2021 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the last 2 years. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 did not have typical seasonality patterns as the market had rapid increases in wholesale values for the majority of the year. The Wholesale Weekly Price Index reached the highest point of the year at the end of December, reporting over 1.51 points. Now, in calendar year 2022, the index has been reverted back to the 1.00 mark and overall wholesale prices are continuing to increase.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Retail (Used and New) Insights

Volkswagen will join the electric off-road market by creating a new company with the Scout nameplate, once used by International Harvester; the Scout brand will begin production in 2026, with an electric pickup truck and SUV duo.

Bollinger Motors has joined forces with Roush Industries to produce electric platforms for commercial fleets, specifically all-electric Class 3 through 6 platforms and chassis cabs.

Volvo recently began accepting orders for the Volvo FH, Volvo FM, and Volvo FMX; these heavy-duty electric trucks will offer battery capacities of up to 540 kWh with deliveries expected to begin later this fall.

After making headlines, Canoo representative, Pawel Zoneff, clarified that Canoo has the capital to begin production of its Lifestyle Vehicle this year in its Arkansas plant.

Fisker is now accepting reservations for the electric SUV, the Fisker Pear. This will be the company’s second model after the Fisker Ocean, and is expected to cost less than $30,000 and be built in Ohio with deliveries starting in 2024.

Used Retail Prices

Used Retail Prices are more accessible than in years past, due to the proliferation of ‘no-haggle pricing’ for used-vehicle retailing. Transparent pricing upfront makes the car buying process more enjoyable for customers and allows Black Book to accurately measure retail market trends.

At the on-set of the pandemic, in CY2020, used retail prices increased slightly, following typical seasonal patterns, and then began dropping in April, finally hitting a low point in the late spring months. By late summer of CY2020, Used Retail Prices increased as supply of new vehicle inventory started to become scarce, but retail demand slowed down at the end of CY2020, resulting in declining retail asking prices for the last several weeks of the year. When CY2021 kicked off, demand rebounded while retail prices lagged slightly behind wholesale prices; March of 2021 started the dramatic increases in Used Retail Prices, fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up the pace once again to start the fourth quarter. In Q4, prices on retail listings steadily increased week after week. As CY2021 came to an end, the retail listing price index closed 36% above where the year began.

So far in 2022, the Retail Listings Price Index has remained relatively unchanged (green curve on the graph below), The Index sits around 0.99, indicating a very slight decrease in retail pricing. Typically, there is a lag between changes in wholesale prices and retail prices.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graph below looks at 2-6-year-old vehicles. The Index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

Used Retail Listing Volume has stayed somewhat stagnant and is just below 1.00, indicating that the used retail listing volume is around where CY22 started. The CY22 trend line has been closely following the CY20 trend line but over the last few weeks, the trend line has shifted to now follow the CY19 line.

The Used Retail Days-to-Turn Estimate remains somewhat stagnant, sitting just below 35 days.

Wholesale

Many new model year launches have been delayed until the second half of the year due to the same supply chain issues that have disrupted the automotive industry over the last 2 years. The scarcity of new inventory continues to fuel increases in volume-weighted used vehicle wholesale values. Fuel prices are up nationwide – nearly 10% in the last month – and consumers may be starting to consider the benefits that both hybrid and all-electric vehicles can offer. Volume in lane seems to be comparatively up but some have speculated that this may be due in part to reruns coming back through. Low mileage, clean vehicles continue to be coveted by larger independent dealers and rental companies while other dealers target older, higher mileage vehicles that can be generally procured at a lower price. Lease returns are showing up from a majority of OEMs, indicating that franchise dealers are no longer purchasing every vehicle they can at grounding.

One thing is certain in lanes today: there is no one-size-fits-all approach for buying inventory and sellers should take note.

The Estimated Average Weekly Sales Rate continues to increase and now is at 72%.

Originally posted on Auto Dealer Today

Electrical systems fell from the leading reason for the first time in over a year.

Read More →

2024 models may have casting issue that can lead to loss of control.

Read More →

Potential short-circuit issue covers many brands from model years 2012 through 2018.

Read More →

Reynolds says new report proves improving operational efficiency, engaging technicians in selling maximize profitability, even for very busy service departments.

Read More →

Probe opened to determine whether steering loss incident pervasive or isolated.

Read More →

The vehicles' cargo rail may come loose in certain collisions.

Read More →

Owners are advised to use emergency brake until the vehicles are repaired.

Read More →

Stellantis warns owners to park them away from structures till it works out a fix.

Read More →

Recent deaths, disfigurements blamed on replacement bags made by disreputable sources.

Read More →