TransUnion: Auto Finance Registers Lowest Growth Rate Since Q1 2012

The firm attributed the slowdown to improvements in oil states and tightening underwriting guidelines, which have also helped stabilize delinquency rates.

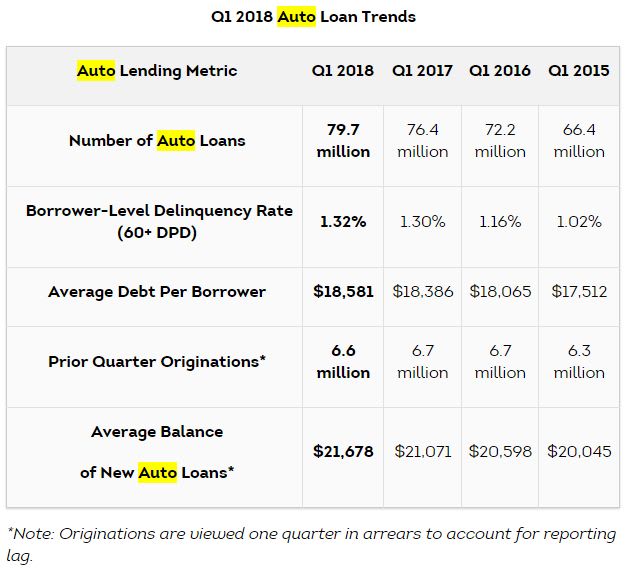

CHICAGO — Tighter underwriting guidelines and better on-time payment in oil states had a positive effect on serious auto delinquency rates per borrower, according to TransUnion.

After growing 1.16% in the first quarter of 2015 to 130% in last year’s opening quarter, the serious delinquency rate — or loans more than 60 days delinquent — stayed relatively flat at 1.32% in the first quarter 2018.

“The first quarter of 2018 was relatively quiet in the auto finance space,” said Brian Landau, senior vice president and automotive business leader at TransUnion. “The most noteworthy change was the stabilization in the delinquency rate, likely due to shifts in the makeup of new auto loan borrowers and continued improvements in oil states.

“Gas prices, as measured by WTI crude, have increased more than 21% in the last year, which has provided a significant boost to the local economies of oil-producing states.”

The top six states with the largest annual decreases in delinquency rates in Q1 2018 — Alaska, Wyoming, Texas, New Mexico, Oklahoma, and North Dakota — are among the eight states where oil, gas, and mining account for 10% or more of gross domestic product. The other two states — Louisiana and West Virginia — also performed better than the national average in terms of annual changes in their serious delinquency rates, according to TransUnion.

The firm also observed a continued shift in the origination makeup of auto loan borrowers, as finance sources continued to migrate to higher credit tiers. This led to the lowest annual growth rate in auto loan balances since the first quarter of 2012. They rose 5.2% to $1.183 trillion.

Overall originations, viewed on quarter in arrears to account for reporting lag, declined 1.5% in the fourth quarter of 2017 — the sixth consecutive quarter of year declines, though the smallest such decrease in 2017.

“Origination mix continues to shift toward lower risk, with superprime and prime plus taking 1.8 points of share from prime, nearprime, and subprime on an annual basis,” Landau said. “This continues the trend from last year, where the shift to the two lowest risk tiers was 1.6 points.

“Finally, we believe the slowdown in auto loan balance growth is largely due to the decline in originations, as lenders continue to tighten their underwriting requirements and rising interest rates put a slight damper on demand.”

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →