F&I Showroom Magazine

The auto finance industry broke new ground in several reporting categories in the first quarter. But not all records are meant to be broken.

Read More →

Since 2011, auto loan debt per borrower has increased 13%, according to Transunion. The firm also reported that delinquencies experienced a sharp drop from 2013's end-of-year quarter.

Read More →While 60-day automotive loan delinquencies fell nationally, 22 states experienced increases. The sharpest increase occurred in Delaware, where delinquencies jumped by nearly 10%.

Read More →

The unusually cold weather that impacted much of the economy didn’t slow down the auto finance industry, which reached new highs in several critical metrics.

Read More →According to TransUnion, the auto loan delinquency rate increased to 1.04 percent in the third quarter. However, the delinquency rate is still well below the third quarter average observed between 2007 and 2013.

Read More →In the third quarter, outstanding balances on automotive loans reached $782.9 billion, up $103 billion from the third quarter 2012.

Read More →

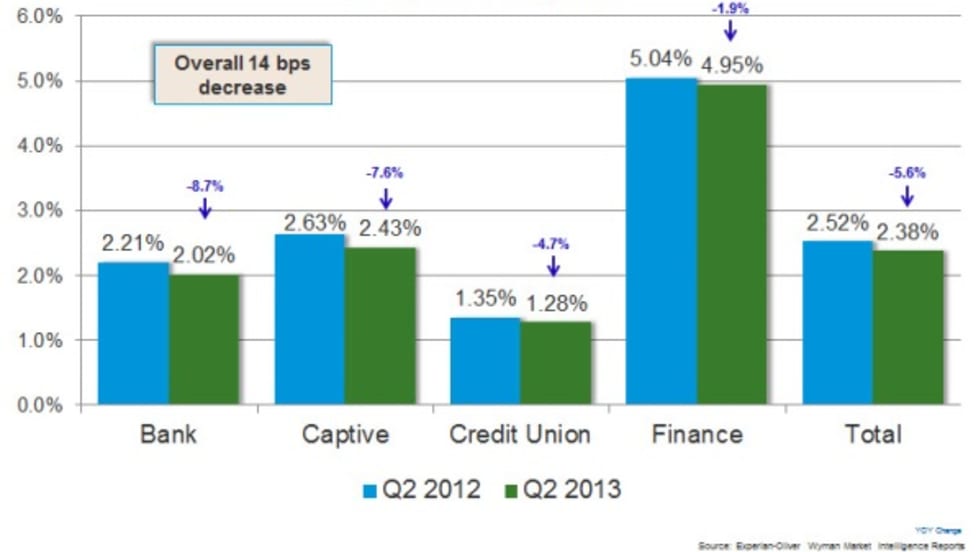

Finance companies are buying deeper, and car buyers are rewarding them with timely payments. Credit expert breaks down the numbers for the second quarter.

Read More →The American Bankers Association found that delinquencies across all credit segments rose six basis points in the second quarter. Overall, delinquencies remain significantly below their 15-year average.

Read More →The balance of auto loans in August increased 9.7 percent from last year, rising from $760.8 billion to $834.4 billion, according to Equifax’s National Consumer Credit Trends Report.

Read More →Auto loan originations totaled more than $196 billion in May 2013, representing more than half of all new non-mortgage consumer credit originated in 2013, according to a new report from Equifax.

Read More →