Kicking into High Gear: Experian Quarterly Update

Finance companies are buying deeper, and car buyers are rewarding them with timely payments. Credit expert breaks down the numbers for the second quarter.

Legendary thief Willie Sutton was once asked why he robbed banks. His simple, straightforward reply went down in history: “Because that’s where the money is.”

Perhaps a little bit of Sutton’s wisdom has made its way down to today’s car buyers. After all, a record 84.5 percent of car buyers went through a bank, credit union, finance company, captive finance company or buy-here, pay-here operation to finance their new-vehicle purchase during the second quarter of 2013. And with interest rates so low, maybe car shoppers feel like they’re getting a steal of a bargain.

Without question, the second quarter was a great time to get an auto loan. A confluence of factors — lower delinquency rates, lower interest rates, lenders willing to take measured risks — has created a near-perfect environment for lenders, retailers and consumers alike. Here’s a look at some of the factors that made the quarter so fertile for the automotive financing market.

Vehicle Financing Up

The 84.5 percent financing mark recorded during the second quarter was up from 82.6 percent in the year-ago period and up from 76.1 percent at the height of the recession in 2009’s second quarter. That’s when credit availability practically dried up following the market meltdown in late 2008.

Less than three-quarters of all new-vehicle purchases involved a loan in 2009, the same year vehicle sales fell below the 10 million-unit mark. Sales have grown steadily since those dark days, as has the percentage of customers financing their vehicles.

Both trends have led to significant growth in the total volume of outstanding loans, which grew from more than $681 billion in the second quarter 2012 to nearly $751 billion one year later. Leading the way were banks, which increased their total dollar volume by $24 billion, followed by credit unions ($18 million), finance companies ($16 million) and captive fin

ance companies ($11 billion).

Leasing Surge Continues

One of the key factors driving the growth in overall financing is the growth in leasing, which accounted for 27.64 percent of the market in the second quarter. That’s up from 24.4 percent in the same period last year, as payment-conscience consumers continue to turn to the transaction type to fund their new-vehicle purchase. And in the second quarter, the average monthly lease payment was $408, compared to $457 for an average monthly payment on a new-vehicle purchase.

Leasing is driven largely by Japanese manufacturers and their captive finance companies, with Toyota Financial Services and American Honda Finance each capturing a 13.7 percent share of the market in the second quarter. Ford Motor Credit came in at No. 3 with an 11 percent share of the lease market, followed by Ally Financial at 10.8 percent.

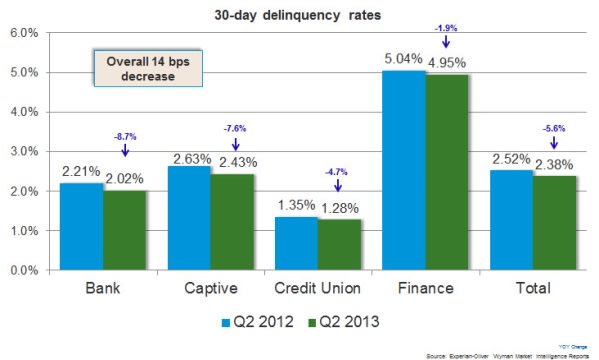

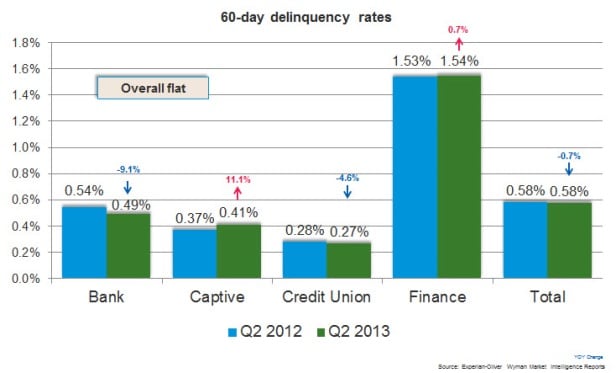

Delinquencies Drop

One of the most surprising trends during the quarter was the strong performance of timely consumer payments. Lenders have been gradually increasing their share of subprime loans. Fortunately, there has not been a corresponding increase in delinquencies.

In the second quarter, 30-day delinquencies dropped to 2.38 percent from 2.52 percent in the same period in 2012. Sixty-day delinquencies remained flat at 0.58 percent.

What did rise during the second quarter was the overall balance of loan dollars 30 days delinquent, which increased by $761 million from a year ago. On a percentage basis, however, delinquencies represented just 1.96 percent of the total loan balance, down from 2.05 percent in 2012. Sixty-day delinquencies accounted for just 0.42 percent of the total loan portfolio dollar value, remaining flat on a year-over-year basis.

Lower delinquency rates also led to lower repossessions. During the second quarter, 0.36 percent of all vehicle loans ended in a repossession, a 14.8 percent drop from the year-ago period. That level also represents a 12.2 percent decrease from the previous low of 0.41 percent, which was recorded in the second quarter 2006.

Gains for Below-Prime Financing

Vehicle sales are also getting a boost from a burgeoning below-prime credit market, as finance sources continue to open their doors to credit-challenged customers. In the second quarter, nonprime, subprime and deep subprime new-vehicle loans captured a 27.45 percent share of the market, up from 25.41 percent in 2012. On the used-vehicle side, nonprime, subprime and deep subprime loans grabbed a 57.31 percent share of the market, up from 56.46 percent in the year-ago period.

These trends pushed average credit scores for auto loans down in the second quarter, with the average score for new-vehicle loans falling from 753 in the year-ago period to 749. For used-vehicle loans, the average score fell two points from a year ago to 660 in the second quarter.

The second quarter also saw an increase in the average amount financed, which rose to $26,526 from $25,714 in the year-ago period. For used, the average amount financed increased to $17,913 from $17,433 in the second quarter 2012. The bad news is average charge-off amounts rose, increasing $6,768 in the year-ago period to $7,218 this year.

The Payoff

The automotive lending market continues to be remarkably strong. Even with the rise in subprime lending in recent months, consumers are doing an excellent job of paying back their loans in a timely fashion. And with lower repossessions and delinquencies, the risk finance sources are taking seems to be paying off.

As new-vehicle sales continue to exhibit strength and interest rates remain relatively low, car shoppers, much like Willie Sutton, are likely to go where the money is. If payments stay strong and interest rates stay low, the automotive finance market should continue its positive momentum. Of course, lenders and dealers will need to keep a close eye on delinquencies and unemployment statistics moving forward. An uptick in either area would be the first dark cloud the industry has seen in a few years.

Melinda Zabritski serves as director of automotive credit for Experian Automotive. E-mail her at melinda.zabritski@bobit.com.

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →