The current market environment will definitely separate the survivors from the victims. F&I expert provides a road map for doing more than just weathering today’s economic storm.

When the car business is

good, it’s great! Right now, however, all we’re talking about is survival. Two

things happen when business is bad. First, a down market separates the

survivors from the victims. Second, it creates tremendous opportunities for the

survivors. In times like these, survivors don’t give up, make excuses, or have

pity parties. They get up every morning looking for ways to turn every

challenge into an opportunity to become better at their craft.

Survival of the fittest is

the ageless law of nature, but the fittest are rarely the strongest. The

fittest are those endowed with the qualities to adapt, the ability to accept

the inevitable, conform to the unavoidable, capitalize on changing conditions,

and turn those challenges into their advantage. When business is good, anybody

can succeed. But in every business downturn, there will be survivors and there

will be victims. Which will you be?

Suddenly, we have fewer

customers walking through the door, subprime lenders who have disappeared, and

more compliance flags than you can possibly wave. We have primary lenders who

won’t consider anyone with a credit score of less than a 700, finance longer

than 60 months, or look at a deal with a loan-to-value ratio of more than 90

percent. We’re seeing fewer finance customers and more cash customers. Credit

unions have become both primary sources and major competitors. So how can we

take advantage of a tough market?

Be Easy To Do Business With

The first way to take

advantage of today’s market conditions is to be easy to do business with. Is

your F&I process treating customers the same way you would treat your

mother? If not, then you need to change your process! Selling is not about

outsmarting customers, it’s about helping that human being on the other side of

the desk. Customers appreciate having someone help them make an informed

decision.

Remember, every customer

still has to buy you first. You must be enthusiastic about the outstanding

value of the products you offer, and share that excitement with your customers.

Every salesperson, every manager, and every customer has to know that you are

genuinely excited to have an opportunity to help customers.

Have fun with your customers!

It ought to be fun to buy a car, and it should be an enjoyable experience in

the F&I office as well. When they leave your office, every customer should

have a smile on their face, and be glad they had a professional take the time

to review their options and help them make the right decision.

Being easy to do business

with also requires that you not fall in love with your process. Processes don’t

sell products, technology doesn’t sell products, and menus don’t sell products.

People do!

F&I Must Operate Separately

To turn up F&I profits in

a down market, the F&I department must be a separate department, not a

secretarial service for the sales department. In many dealerships, salespeople

take the credit application, the sales manager submits the deal to a lender,

negotiates the down payment, monthly payment and the rate before an F&I manager

even talks to a customer. Then the F&I “secretary” is responsible for

typing up whatever the sales department negotiated. That’s not a department,

that’s a secretarial service for the sales department.

The commitment to F&I as

a separate department starts at the top, with the dealer or general manager.

Every dealership needs a checks-and-balances system to ensure the information

on the credit application is correct, and what is being submitted to a lender

is correct. Someone must check every deal to make sure no one is coaching

customers, doctoring credit applications, or power booking vehicles just to get

an approval. Inflating a customer’s income or adding imaginary options to

increase the amount a lender will advance on a vehicle is not fudging the figures,

it’s a felony.

There are also new rules and

risks when it comes to quoting payments. Customers are entitled to accurate

monthly payment quotes. When they don’t get them, it’s deceptive and unlawful.

So, what’s in your deal jacket? Do the payments on the deal sheet or worksheet

bear any resemblance to reality? Who’s making sure no one is packing payments

or creating a legal liability by promising customers they’ll get the best rate

possible?

No deal should ever be

submitted to a lender until a F&I professional confirms all the information

on the credit application, and has interviewed the customer regarding his or

her credit history. Prior to submitting the credit application, a F&I

professional has to learn the circumstances and details surrounding any adverse

credit information disclosed by the customer or revealed by the credit bureau

report. Every customer has a story, and it’s the F&I manager’s job to hear

it, document it, and then paint a picture for a paper buyer as to why he or she

should buy the deal or change a tier level.

[PAGEBREAK]

Keep it Between the Buoys

Turning up F&I profits

also requires that every dealership establish parameters for the sales desk

with regard to quoting payments. These parameters should include the maximum

loan-to-value ratios, term, debt-to-income ratios, and payment-to-income

ratios.

Any payment quoted before

obtaining a credit bureau report should be based on an average rate (a finance

rate grid should be used after obtaining a credit bureau report) to ensure

consistency and compliance. Do not make exceptions. The customer’s actual rate

is provided by the F&I manager once the loan is approved.

Those parameters must also

stipulate that there can be no packed payments by anyone, anywhere, anytime.

There should be no “low-ball” rates, either. A 419 FICO score does not equal a

4.19 percent rate.

The parameters should include

a maximum payment range on any payment quote of $5, taking into consideration

the number of days to first payment. There can be no fudging the figures. Any

payment quote should also include disclosure of the down payment, amount

financed, term, and annual percentage rate. The F&I department should be

solely responsible for converting outside finance and cash customers to

dealership financing. The sales department is responsible for selling the car,

not the financing.

Finally, the F&I

department submits every deal, not the desk. A F&I professional is

responsible for ensuring proper deal structure prior to submitting the

application to a lender, monitoring the dealership’s portfolio mix and

look-to-book ratio, knowing each lender’s scoring system, and utilizing lender

leverage to obtain an approval.

Sell Customers What They Can Afford

When we sell customer’s what

they can’t buy, they don’t buy. Turning up F&I profits requires we go back

to the fundamental concept … sell customers what they can afford. Salespeople

should attempt to switch every customer up front, not after they can’t buy what

they already sold them. Here’s an easy way for a salesperson to switch a

customer:

“We find a lot of customers

who come in looking for a new car decide to buy a certified pre-owned instead,

because they can save $3,000 to $4,000, and have a payment that’s $75 to $100

less per month. Before we drive your new car, is that something you would like

to consider as well?”

Mentally switching customers

upfront allows them to save face when they select more car than they can

afford. It also provides price and payment protection for the salesperson when

the customer objects to the first pencil. If they accept the switch, they

should demo the switch vehicle first. Salespeople have to determine what

customers can afford before they commit to buying what they can’t.

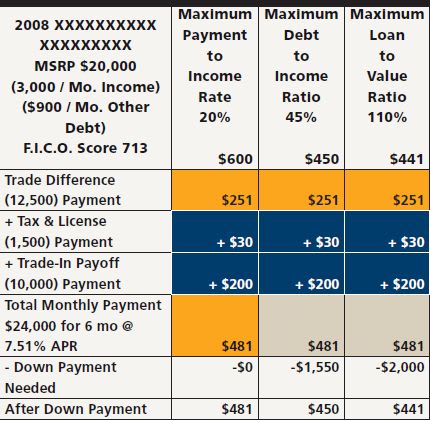

It’s also time to forget the

four-square and give customer’s a three-column (see illustration).

[PAGEBREAK]

We’ve taken the

smoke-and-mirror approach about as far as it will go. Today, we have to educate

customers as to what they can afford, and help them see the benefits of equity.

They also need to see a breakdown of the monthly payment trade difference,

payoff on their trade-in, and tax and license fees. In other words, educate and

inform customers, do not obfuscate and confuse them.

Implement an F&I Wellness Program

Finally, to turn up F&I

profits you must implement an F&I wellness program. Greet the customer in

the salesperson’s office, get involved early in every deal, and manage by

wandering around the dealership.

Add value to the customer’s

purchase experience by educating and informing him orher about their options.

Become valuable by educating and informing customers about financing. Help them

obtain acceptable financing by reviewing their credit application and their

credit bureau report prior to submission to a lender. This will allow you to

paint a clear picture of their financial situation for your lenders. Help them

understand your lenders’ guidelines, their FICO score, and how they can dispute

errors in their credit bureau report.

Use technology to improve

communication and trust. Let your customers see you enter their information

into the computer, submit their deal, and customize a menu based on their

needs. Exceed their expectations by giving customers more than they ask for.

Concentrate on what is best for the customer. Sell products based on their

agenda, not your agenda. Utilize needs-based selling, not greed-based selling.

Require a F&I manager to

talk to every customer with a FICO score below 740 prior to submission to a

lender. The F&I manager must also review the credit application prior to

submission. The F&I manager is solely responsible for selling F&I

products, and financing is a product. And finally, utilize an ongoing training

program that tracks individual training activity.

Survivor or Victim?

If you want to turn up

F&I profits, be easy to do business with. Treat people the way you’d want

to be treated. F&I must also be a separate department, not a secretarial

service for the sales department. Your dealership must also establish

parameters for the desk with regard to quoting payments before and after

obtaining a credit bureau report.

Additionally, salespeople

have to sell customers what they can afford. We must also use a three-column to

educate and inform customers about their monthly payment and the criteria

lenders use to evaluate a deal. Finally, you need to implement an F&I

wellness program to ensure you become valuable to customers, salespeople, the

desk, your lenders, and the dealership.

In a down market, you will

either be a victim or a survivor. You choose.

Ron Reahard is president of Reahard & Associates

Inc., an F&I training company providing F&I classes, as well as

in-dealership and online training. He can be contacted at

ron.reahard@bobit.com.