In the second quarter, finance sources continued their drive down into the high-risk credit tiers and consumers continued to pay on time. But the magazine’s resident finance insider wonders how long those trends can continue in this month’s review of quarterly auto finance trends.

by Melinda Zabritski

October 7, 2011

4 min to read

A few bumps in the road may have slowed the economic recovery, but that wasn’t the case for auto finance, especially in the second quarter. Dealers were able to find more sources for their credit-challenged customers, with Experian Automotive’s quarterly auto finance data showing a significant increase in loans made to below-prime car buyers.

That segment represented 22.29 percent of all new-vehicle loans originated during the second quarter, an 18.21 percent increase from the year-ago period. This was welcome news to both dealers and manufacturers, especially with half of all potential consumers falling into the high-risk credit tiers.

Ad Loading...

For their part, consumers continued to improve their loan repayment patterns, and their good behavior is driving the push into the high-risk credit tiers on the part of finance sources. That pattern also is driving down delinquencies, repossessions and dollar volumes of at-risk loans. The uptick in average loan amounts for new ($17) and used ($476) vehicles also served as an indicator of the auto finance industry’s improving health and appetite.

Delinquencies Continue to Fall

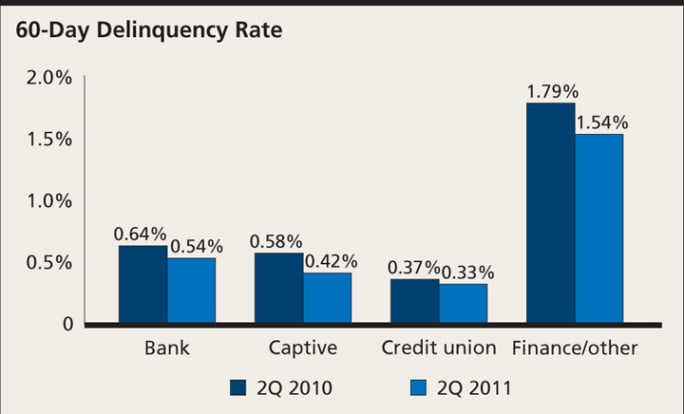

As previously mentioned, consumers continued to make their payments on time and gave finance sources every reason to delve deeper into the lower credit tiers. The 30-day delinquency rate, for instance, declined by 10.39 percent in the second quarter, falling from 2.89 percent to 2.59 percent of all open automotive loans. Additionally, the 60-day delinquency rate fell by 14.46 percent, with finance companies experiencing the largest rate decline.

The decreases in the 30- and 60-day delinquency rate led to a nearly 20 percent decline in overall dollar volume of at-risk loans, which fell from $21 billion a year ago to $16.9 billion in the second quarter.

Below Prime in the Fast Lane

Ad Loading...

The most positive sign for dealers was the 22.4 percent year-over-year jump in new-vehicle loans made to credit-challenged customers. That increase shouldn’t be a surprise, given the improvements in delinquencies and dollar volumes of at-risk loans.

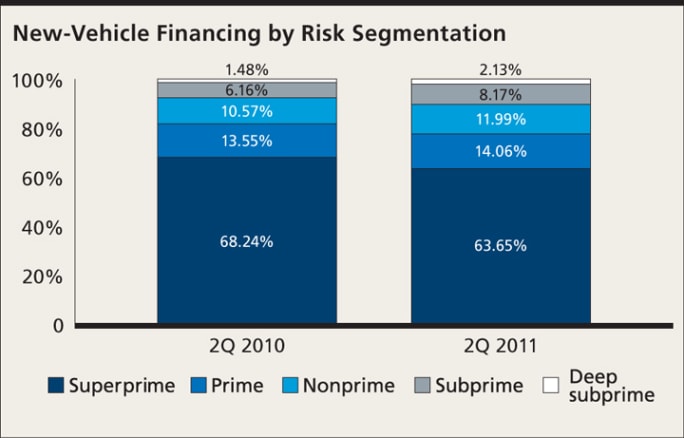

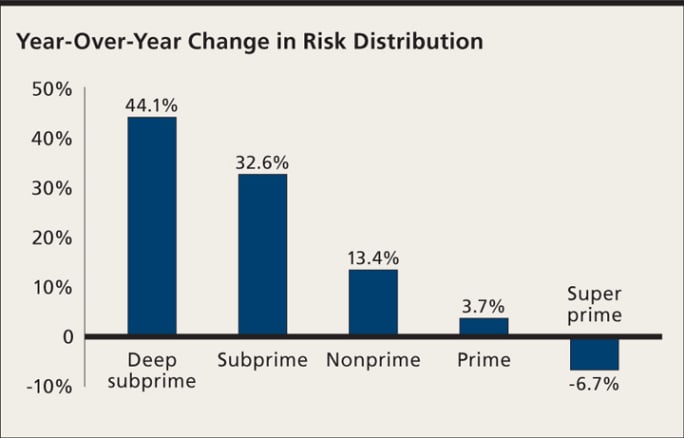

Breaking down the high-risk segment, the share of auto loans made to nonprime customers rose from 10.57 percent a year ago to 11.99 percent. The share of loans for subprime customers rose from 6.16 percent in the year-ago quarter to 8.17 percent. The biggest jump in share was made by the deep subprime category, which rose 44.1 percent year over year to 2.13 percent.

Loans made to the below-prime risk tiers also jumped in the used segment, increasing by 7.7 percent year over year. Overall, 52.7 percent of used-vehicle loans were made to nonprime, subprime or deep subprime car buyers, up from 48.93 percent in the year-ago quarter.[PAGEBREAK]

Average Amount Financed Spikes for Used

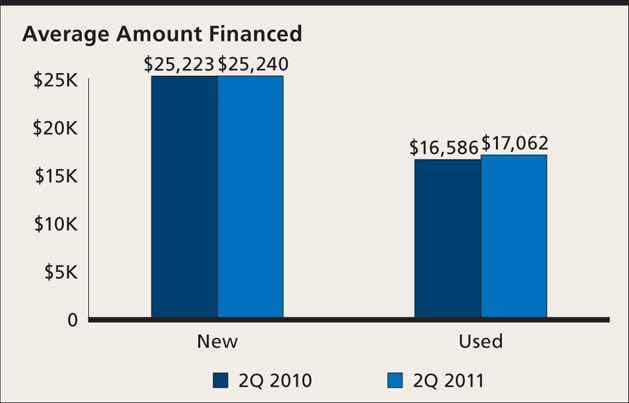

The average amount financed for new vehicles remained relatively unchanged from the same quarter last year. Used-vehicle loans, on the other hand, experienced a significant jump from the second quarter of 2010.

Ad Loading...

The average loan amount for a new vehicle increased $17 to $25,240, while the average for used rose by $476 to $17,062. The spike in loan amounts for used vehicles, however, was not a reflection of lenders loosening their credit criteria. The increase could instead be attributed to the rise in used-vehicle pricing during the quarter.

Average monthly payments for new vehicles were flat as well, with the average payment decreasing $5 to $450. The average payment for used, however, jumped by $347.

Loan terms showed little movement, with new-vehicle terms rising just one month to 63 months. Used terms increased from 58 months in the year-ago period to 59 months.

3 Potential Threats to Industry’s Good Health

Finance sources are feeling a lot better these days, but will it last? Consumers are getting better at paying off their loans, which is causing delinquencies and dollar volumes of at-risk loans to fall. But this renewed stability could also lead to higher risk taking on the part of finance sources.

Ad Loading...

The auto finance market also is operating in what remains a relatively flat retail market. The danger here is that a battle for deals could fuel a return to the prerecession race for market share. That wouldn’t be a bad thing for dealers in areas with a large pool of nonprime customers, but it would not be good for the long-term health of the industry.

The other threat is the teetering economy. If the country were to fall into another recession, there’s no telling what strategies lenders will employ for the remainder of the third quarter and beyond. There is a possibility that they might continue to reach deeper into nonprime, but they could just as easily pull back in the face of high unemployment and the roller-coaster ride the stock market has been on in recent months.

If we can avoid a double-dip recession, finance sources will be well positioned going forward. If not, the spike in riskier loans could turn into a slippery slope for the industry.

Melinda Zabritski serves as director of automotive credit for Experian Automotive. E-mail her at melinda.zabritski@bobit.com.

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.