A reinsurance veteran reminds dealers that business partners are best judged by the companies they keep, and details an incident that should serve as a warning to all.

by Gary Vucekovich

May 14, 2012

6 min to read

Well, I recently earned another honorary degree from the school of hard knocks, this one in insurance studies. I thought my other degrees from that school were expensive until now. Acquiring this B.S. (and that doesn’t stand for “Bachelor of Science”), required learning a lot of big words like “insolvency,” “co-mingling of funds,” “special deputy receiver,” and “liquidator,” who, it turns out, is sort of like “the Terminator.”

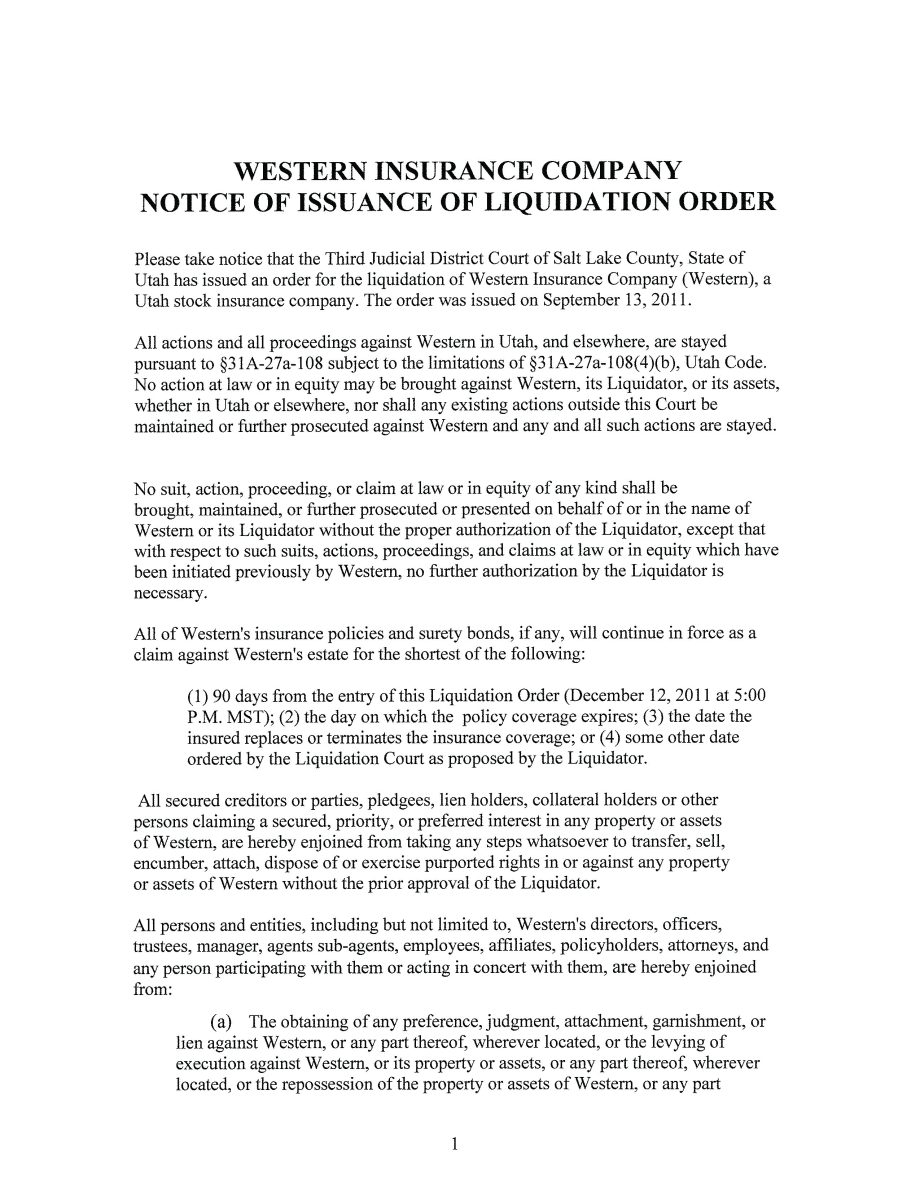

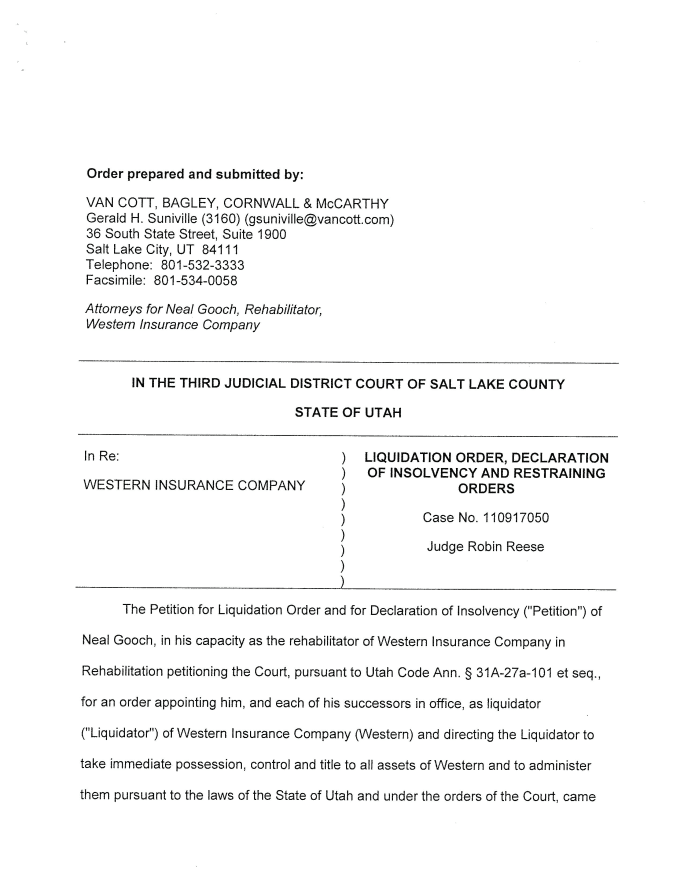

It started one day, late last year, as I was going through my mail in my office here at ForeSight Services Group (FSG). The first letter was from the Third Judicial District Court of Salt Lake City. It screamed at me in bold print: “WESTERN INSURANCE COMPANY NOTICE OF ISSUANCE OF LIQUIDATION ORDER.”

It was quite a contrast to my first meeting less than five years ago with the senior management and officers of Western Insurance Company Co. (WIC). At the time, they sported an impressive A.M. Best rating of “A-.” I distinctly recall us gathering in the company’s conference room — much fancier than the one I have at FSG — to discuss a possible business relationship.

My company reinsures mechanical breakdown service contracts at 100 percent for auto dealers, and I insisted that, under any agreement, all monies would flow directly from dealers to FSG. We would remit fronting fees to WIC and the dealer’s premium would go straight into a fully segregated trust account held by a dealer-owned reinsurance company, one with its own Federal Tax ID and was managed by a non-affiliated national bank. Over the course of the full-day meeting, we hammered out the details.

Ad Loading...

Four years later, WIC was declared insolvent and ordered into liquidation. By then we had set up 17 separate reinsurance custodial trust accounts totaling millions of dollars on behalf of our dealer clients. What would be the fate of these accounts? Might they be added to WIC’s general assets? Would FSG and our clients be made to circle around with other claimants like sharks, waiting for the Terminator to dole us out a morsel?

The decision came down on Dec. 29, 2011. The liquidator’s investigation had found that our dealer clients’ assets were indeed in properly segregated accounts held pursuant to tri-party agreements. Western did not control but could only seek distributions from these accounts. As such, they should not be considered part of the general assets of WIC’s estate. The court agreed and released the funds to their proper owners.

[PAGEBREAK]

No Winners, Just Bigger Losers Cue the scene at the end of one of those big courtroom dramas, where everyone runs out of the courtroom cheering. It was, indeed, a big victory for FSG and our dealer clients. You may even be thinking: “Gary, that lesson wasn’t expensive at all. You came out unscathed.” Unfortunately, the story doesn’t end there.

Just prior to leaving that fine conference room at WIC, I was asked to deposit $100,000 as good-faith security. Fair enough, I thought, but insisted the money be placed in a CD earning interest for FSG. I guess I should have been suspicious when they responded by offering me a CD with a great interest rate through Western Thrift & Loan, a bank associated with — you guessed it — WIC!

But hindsight is always 20/20. And I certainly don’t recall giving WIC permission to cash the CD and deposit the money in their own account in 2010, which, according to the Special Deputy Receiver’s attorney, is exactly what they did. As I understand it, the individual responsible is now retired and living a life of luxury.

Said attorney also mentioned that I was “not the first Western customer who has experienced this type of loss due to Western’s failure to segregate funds.” My only course of action was “to file a claim with the liquidator.” In other words, start circling with the sharks.

Despite this, I still feel fortunate. There was another company in the WIC liquidation that operates similarly to FSG. They did everything above board and proper, with the exception of having premiums sent directly to WIC. Ouch!

Retro vs. Dealer-Owned When choosing between retro participation agreements and a dealer-owned reinsurance company, it’s a no-brainer for most dealers.

I have more than 30 years of experience in the automotive industry, 15 years of which were spent reading various retro participation agreements. These started as an ingenious scheme to allow insurance companies to expand their market share while allowing dealers to share in back-end profits. But today, whether the agreement is provided by an administrator or insurance company, there is simply a better wealth-building structure available: It’s called a “dealer-owned reinsurance company.”

My cell phone may start ringing like crazy for saying this, but it’s my opinion that retro agreements have outlasted their value for all but the smallest of dealers, for whom maintaining a dealer-owned reinsurance company would be cost-prohibitive.

Given my experience with WIC, the most glaring concern of retro agreements is the co-mingling of premiums and reserves to pay future claims. I do not know of a single retro agreement available that would prevent a liquidator from grabbing funds and giving them out at pennies on the dollar if the administrator or insurance company is declared insolvent.

[PAGEBREAK] Having survived 2008 and 2009, I’ve become more skeptical of companies who tout their history of financial strength and A.M. Best ratings. Remember AIG? No company can stay on top forever.

In the case of WIC, their undoing had nothing to do with the auto industry. That was the most profitable part of their business. The problem was the surety bonds they were issuing for construction projects in states like Nevada and California.

Who has time to audit every aspect of the insurance companies they do business with? That was what ratings were supposed to be for!

Fifteen years ago, I didn’t even know how to spell retro agreement. But I entered into one anyway. The $21,000 in back-end profits sure looked like a fine number, but it eventually evaporated into the “terms and conditions” spelled out in the agreement. In my opinion, stipulations such as minimum production, loss ratios, notice of termination and lapse in production often hold the dealer captive or open loopholes that swallow the dealer’s share of profits.

I learned my lesson and, five years ago, I got to apply it by insisting on a full reinsurance structure for my clients as we began our relationship with WIC. I hate to think where I would be now if I hadn’t done that. It shows that “honorary degrees,” while expensive, can turn out to be worth every penny.

Ad Loading...

Gary Vucekovich

Gary Vucekovich is president of ForeSight Group Services Inc., a provider of long-term revenue strategies for auto dealers. Contact him at gary.vucekovich@bobit.com.

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.