F&I pro says there’s no way to avoid those deal-killing situations, but he does offer five strategies for ensuring that your sold and delivered customers stay that way.

by Mick Warshaw

February 6, 2014

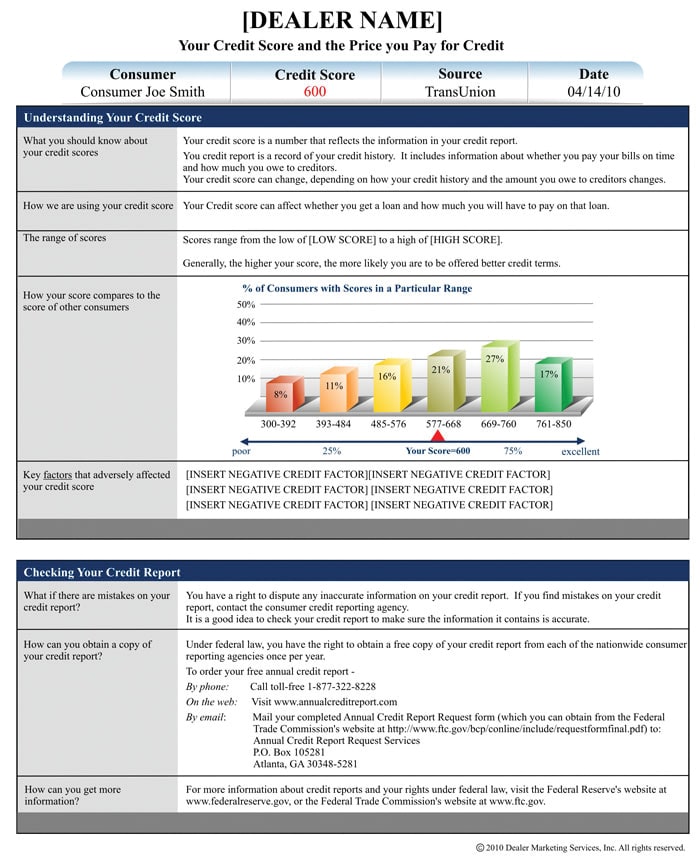

If your customer won’t sign a credit score disclosure, just note the refusal and move on.

7 min to read

Motorcyclists have a saying: It’s not if you lay it (your bike) down, it’s when. We have a similar saying in automotive finance: It’s not if you will lose a deal, it’s when.

Whether miscommunication on the sales floor, numbers fatigue, a confused customer, the push from all sides to speed up the process or the alarming amount of misinformation presented to customers, there is ample opportunity for the finance manager to be caught in a downward spiral. Whatever the cause, the result is no sale.

Ad Loading...

The true F&I professional plans ahead for these potential deal killers and has strategies in place to avoid damaging confrontations and misunderstandings. Here are five ways to make sure your delivered customers stay that way.

1. Get Involved Early While this may seem like a no-brainer, many sales managers have worked deals from start to finish for a long time. This habit can lead to the sales manager bypassing the F&I manager and doing things that should only happen in the finance office. Payment quotes, for example, should be discussed with everyone involved in the deal before they are presented to the customer.

Besides the obvious benefit of the finance manager handling the finance portion of the deal, early involvement allows for greater fact-finding in advance. Many sales consultants and sales managers consider outside liens to be the same as cash. To the experienced finance professional, outside liens represent an opportunity to beat a rate and earn more business. A small flat on a contract written at retention may not do much for the department’s bottom line, but oatmeal is better than no meal!

And, as most veterans know, customers financing through the dealership are far more likely to purchase F&I products at the point of sale. Eligibility for some protections is contingent on the dealership securing the financing as well. And the customer may have included the products in their loan quotes from their credit union or bank. These customers will frequently purchase the same products from the dealership they planned to purchase from their outside lender.

Finally, attempting the “finance switch” before the customer enters the F&I office gives the producer more time to do his or her job. Once customers enter the business office, they feel as if they have completed the process and are less receptive to the switch. Their mental clock leaves the business manager enough time to get through all the paperwork, but not enough time to secure a loan — even if the terms are superior.

Ad Loading...

2. Don’t Hide From the Numbers In the good old days, the auto industry developed quite a reputation for deceptive tactics. The “five-finger close,” for example, had the finance manager use his or her fingers to cover up some of the financial details on the contract. This led to customers paying higher rates to cover products they didn’t agree to.

Today, federal regulators and lenders have put the finance process under a microscope. Customers are also armed with more information, which means the old-school tactics no longer work. Truth is, they are no longer needed to run a profitable department.

See, people like to feel they are dealing with honest sales and finance professionals. They want the employees at their chosen dealership to be credible and the quickest way to build credibility as a business manager is to thoroughly go over all the figures with the customer before you sign a single piece of paper.

Some product administrators (Zurich, for example) include this disclosure process in their menu training. Some directors advocate showing the customer their deal structure as it appears in the DMS. However it is done, the customer should be made aware of the sale price, all the fees and taxes, the rate and the payment before any product is sold. There is no reason to soft-pedal it. Just present the figures as a settled fact, make sure there are no questions and move on.

Remember, the customer’s rate is based on his or her credit, while the customer’s payment is based on the vehicle he or she selected. It is not the business manager’s responsibility to “fix” these things. A simple and professional delivery makes that clear.

Ad Loading...

3. Don’t Take Responsibility for Someone Else’s Numbers Just as the customer’s credit is not the F&I manager’s responsibility, neither are offers on their trade-in vehicle. If a customer says the figures you have are not the figures they agreed to, the first step is to pull the “pencil” from the deal jacket and make sure the figures do indeed match the DMS. If the figures don’t match, find out why. If they do and the customer still insists the figures are not the numbers they agreed to, bring in the person with whom they made their agreement.

Frequently, the customer is just trying to “take a shot” with the business manager and a quick rehash with the salesperson or sales manager will clear up the fake confusion. Sometimes there is genuine confusion. In those cases, the business manager cannot help the situation by assuming ownership of the figures. Departments are separated for a reason. Just as the finance department doesn’t want the used-car manager giving away rate, the used-car manager doesn’t want F&I stepping in on trades.

Blithely adjusting the numbers in the finance office can also have the effect of destroying credibility — not just the business manager’s or the sales staff’s credibility, but the credibility of the entire dealership. If business managers have the authority to do whatever they please, why have other managers?

4. Recognize When It’s Time to Move On The best producers in finance make fantastic product presentations. They can also overcome all manner of objections on the road to a sale. They know it is OK to push a little for a close. When faced with objection sometimes — if you are very careful — it is OK to push a customer right up to their personal “redline” before backing off. In fact, that is the only way to get some deals done and products sold.

Sometimes, though, the customer doesn’t have an objection to overcome, or cannot be closed regardless of the skill of the business manager. Recognizing these circumstances quickly can help business managers maintain a smooth, friendly relationship with each customer. Pushing too hard now may not lose the current sale, but it could push away future business.

Ad Loading...

5. Do Not Respond in Kind Some people just aren’t very nice. They are rude, loud, vulgar, pushy and sometimes hostile. And sometimes these types of people buy cars, bringing their unattractive traits with them. It is tempting to be just as rude, hostile, loud and vulgar as the customer is, but don’t do it. Maintain a professional demeanor at all times. Don’t even tell dirty jokes with the “fun” customers, because sometimes they are just an obnoxious customer in disguise.

Don’t yell and don’t lecture the customer, no matter how bad they get. Treat everyone with respect, and go through the entire finance presentation even when it’s an unpleasant task. Calmly reassure the customer that the paperwork in the business office is legally required documentation and that they are entitled to the same full disclosure as everyone else. Make it clear that the entire purchase is contained in the paperwork and the customer is due copies of most of it.

Occasionally, the customer won’t sign some of the paperwork. If it’s for DMV work or is financial in nature, there is no deal without those signatures. On the other hand, some of the paperwork is simply disclosures. If the customer won’t sign a credit score disclosure form as required by the Risk-Based Pricing Rule, no problem. Note on the signature blank that the customer refused to sign it and move on. The same goes for many other forms, just be sure to check with your dealership’s attorney before doing this.

If all else fails, allow the customer to finish his or her paperwork with another manager. Having someone else sign up the deal is infinitely better than losing the deal. Don’t let a big ego cost the dealership a sale. The tips presented here are not revolutionary. There is no need to reinvent the wheel when the one in use rolls just fine. But when followed, these tips will help the F&I department keep deals on the board. Just like the motorcycle riders, though, the crash will come. At that point, the professional should recognize and take ownership of what he or she did wrong and get back on the road.

Mick Warshaw is a veteran F&I pro from Culpeper, Va., where he serves in the finance department at Battlefield Toyota Chevrolet. Email him at mick.warshaw@bobit.com. No part of this article is intended as legal advice and should not be taken as such.

Talk to F&I customers like you’d talk to a friend, without industry lingo or sales-like questions, and use hard proof to show, not tell, them about a need.

Helping F&I customers understand complementary offerings is likely to lead to more sales, based on the success of a high-performing practitioner of the philosophy.

In this video, Reese Dailey explains how effective follow-up drives better results

across the dealership, including increased sales, higher F&I penetration, and

stronger customer retention.

It may be human nature to back off when a customer seems to say no to a product or service. But experts say F&I managers should operate as though the answer will be the opposite.

Deal volume ebbed and flowed throughout 2025, but product performance remained steady, according to automotive technology and data intelligence solutions provider StoneEagle.