Compliance was top of mind at the 2014 NADA Convention & Expo, with product vendors showing the way to a faster, more transparent process in the F&I office and throughout the sales process.

“Accelerate Your Business” was the tagline for this year’s National Automobile Dealers Association (NADA) Convention & Expo, and exhibitors embraced the theme wholeheartedly. Attendees who roamed the aisles of the exhibit hall in New Orleans were met with a swath of offerings meant to speed up the transaction process in their dealerships — without sacrificing customer service or compliance.

In fact, with the Consumer Financial Protection Bureau (CFPB) bearing down on the industry — and the NADA launching a previously unannounced fair lending program and workshop at the show — compliance was already top of mind for most vendors.

Ad Loading...

“Probably the single biggest adversary these days is not the factory,” said Peter Welch, the association’s president, as he welcomed dealers to the 2014 International Automotive Roundtable during industry week. “But it’s the governments that control us and overregulate us and want to put restraints on us and the free markets that we operate in, and … your ability to be profitable and to support the employees that you employ and to sell products that you sell.”

Many of the industry’s leading compliance firms offered straightforward solutions; others sought to provide peace of mind to dealers with tools that increase transparency and provide instant, accurate credit reports, finance quotes and communication with lenders.

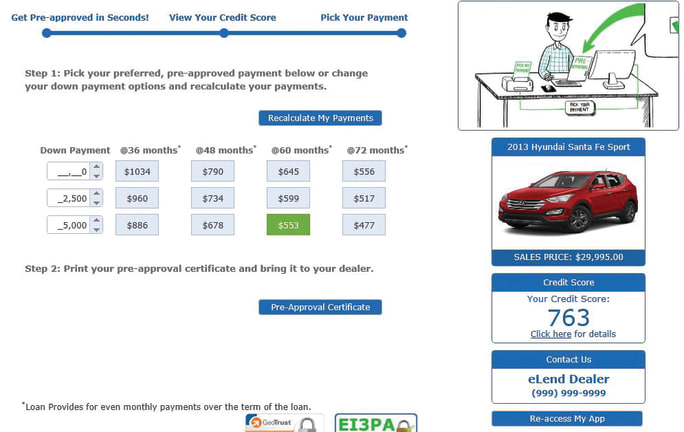

DealerCentric: Remove the Guesswork After a decade in business, DealerCentric is rebranding as E-LEND Solutions amid what Pete MacInnis called a “perfect storm” in the industry. “There’s this collision course between consumer demand … and the potential impact of the CFPB on dealer participation,” said the company’s founder, chairman and CEO. “So you’ve got consumers pushing this way, the CFPB coming this way, and the dealer is stuck right in the middle.”

E-LEND’S loan decisioning engine displays approved financing terms to Internet shoppers by verifying their identity, pulling their credit file and matching the information to the customer’s chosen vehicle, payment or price.

Car buyers also want a more tech-savvy process, MacInnis noted, adding that he hopes the new E-LEND auto finance platform will meet those expectations while also addressing possible compliance issues in the F&I office. The platform is set to be released by the end of the first quarter.

One area MacInnis said dealers need to rethink is how they present rate quotes to customers. “Traditionally, it’s educated guesswork,” he explained. “We’re talking about bringing finance to the front of the sales process. [Dealers] are going to have to know … exactly what rate terms and payments that customer is going to have right at the front end of the deal.”

Ad Loading...

E-LEND’s loan decisioning engine displays approved financing terms to customers online by authenticating their identity, pulling their credit file and matching the information to the customer’s chosen vehicle, payment or price. That data is then compared against rate and rule data from lenders. Dealers then receive a link to a web page that displays all the lender programs the customer qualifies for.

“When that consumer is willing to put his personal information online, he’s really raising his hand and signaling, ‘I’m ready to buy,’” MacInnis noted. “And so the dealer knows, when you think about that from a lead-generation standpoint, those are his highest quality leads.”

The company also sees the E-LEND platform as an opportunity for F&I managers to sell more product, because the system cuts down on the time spent discussing finance terms. MacInnis noted that “the dealer can provide the final terms of approval before the consumer even completes the test drive.”

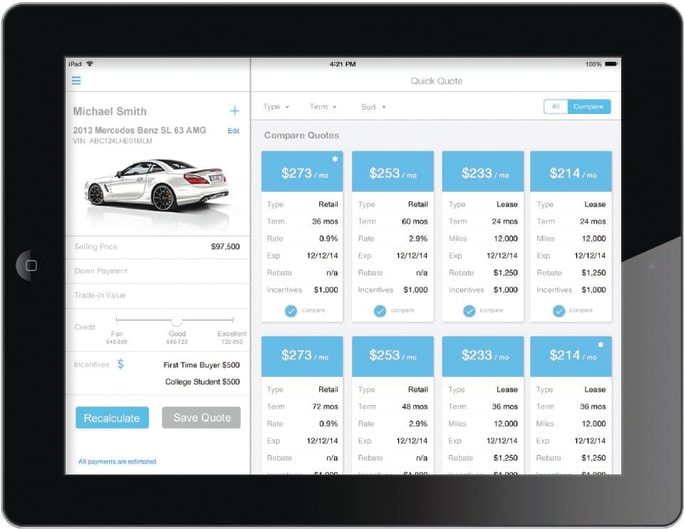

Dealertrack: Shop By Payment Dealertrack Technologies has distilled the car-buying process into what it calls the Dealflow Advantage. For each step in the process — from digital retailing to credit applications to registration and titling — the company touts a solution to help sales and F&I provide a seamless experience to customers. The company’s latest solution is called Quick Quote, which was unveiled at the convention. Housed on a tablet or smartphone, Quick Quote allows salespeople to present finance and lease quotes to customers in real time.

“Like our eMenu for iPad, [Quick Quote] is a dealer-facilitated kind of process that increases transparency,” said Allan Stejskal, vice president and general manager of Dealertrack’s sales and F&I solutions team. “You can show the consumer the different options.”

Ad Loading...

Able to operate on a tablet or smartphone, Quick Quote allows salespeople to present finance and lease quotes to customers in real time.

Quick Quote can calculate a variety of retail and lease options by rate, loan term and more, Stejskal noted, adding that dealers also have the option to integrate inventory information to give them the ability to present vehicle-specific lease and finance quotes. In that same vein, the tool can access incentives and lender programs.

Stejskal added that one of Dealertrack’s objectives is to use accurate, up-to-date data across all of its offerings, which he said will drive a better connection between a dealership’s online and showroom experience. “So [Quick Quote] ties right in, as it uses all the same data so it’s consistent from one place to another,” he explained. “What you saw online is the same you’re going to see in the store. There’s no disconnect for the consumer.”

In the month of December, the company recorded 17 million instances of customers seeking specific payment information on specific vehicles using its digital retailing tools. This trend is on an upward trajectory, Stejskal said, which makes the option to present quotes by monthly payment a no-brainer.

Jason Barrie, senior director of product marketing for the company, agreed. “There’s this consistent theme about all of these presentation tools that we have, whether it’s on the F&I product side or pricing on the website for the dealership — it’s that transparency with the consumer,” he explained. “The greatest reaction we’ve had from dealers on Quick Quote is the simplicity, the elegance, the power for the salesperson to be able to adjust within the boundaries set by the dealership.”

Quick Quote is slated for a July release.

Ad Loading...

Equifax: Improve Credit Reporting During the convention, credit reporting agency Equifax unveiled plans to release a suite of online solutions to help dealers work seamlessly with lenders. Over the past year, the company has shifted its focus to the automotive space by building a team of experts and working to identify “pain points” in the industry.

Jennifer Reid, Equifax’s senior director of product marketing, said one of the first problem areas the company identified was credit reporting. “We started to kind of look at how we could improve that process,” she said. “The dealer would pull one score, the lender would have a different score. This would cause issues, specifically if you spot deliver a car and find out that, ‘Hey, I thought the [customer’s credit score] was 700, but really it’s 660.’”

The company plans to roll out the enhanced credit report to 1,200 dealers by April. It will be housed in Equifax’s eport, an online portal that will eventually house the company’s fraud mitigation and compliance data solutions for dealerships. The portal was recently redesigned to increase efficiency and ease of use. Current users can log in to the portal to perform instant income and employment verifications. “These are all solutions we’ve had from an Equifax perspective. We just haven’t used them from an automotive perspective,” Reid explained. “So we really reconfigured them to bring them into the auto space.”

At the top of the report, dealers will find the customer’s auto tradelines, followed by the three different credit scores that are taken into account by most lenders. “Different lenders are using different versions [of credit scores], and, obviously, dealers don’t stick with one lender,” said Scott McMahon, vice president of marketing for Equifax Automotive Services. “They’ll stick with a handful of lenders that operate off multiple versions [of credit scores] … so the dealer is now empowered to understand exactly what the credit score looks like and ultimately make a decision on which lending opportunity they should be pursuing.”

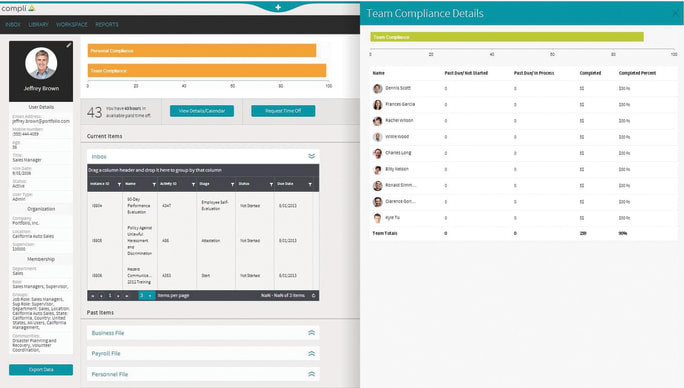

Compli: Compliance Management Compli introduced its Compli Portfolio at last year’s NADA Convention & Expo, but the product is currently in the midst of a soft rollout. David Childers, company CEO, was on the expo floor to discuss the cloud-based compliance obligation management solution with attendees.

Ad Loading...

“Oftentimes, we consider ourselves to be in the litigation preparation business,” Childers said. “We want to inspire our clients to be able to have the confidence that they can demonstrate their compliance veracity — the things that they are doing — to a regulator.”

Compli Portfolio provides dealerships with the ability to build a compliance activity profile for each employee that can change as staffers are transferred or promoted.

Compli Portfolio was designed to allow dealers to house, distribute, track and generate reports on all of their compliance obligations. The system also gives dealerships the ability to build a compliance activity profile for each employee that can change as staffers are transferred or promoted within the organization.

Childers said dealers are right to worry about documentation, especially since federal fines are not scaled to the size of a dealership. “The sad part about it is that, while the impact is great on all organizations, it’s even greater on small to mid-size dealers,” he explained. “The fine structure is the same if you’re AutoNation or if you’re Bob’s on the corner … So if you’re a small dealer, you can get the same $250,000 fine that the large dealer can get.”

Compli Portfolio is intended to work for dealers of all sizes, with customizable workflows and information that can be sorted by rooftop, brand or personnel through the product’s dynamic dashboard reporting tool. There are 47 different customizable workflow templates, which users can populate using the tool’s drag-and-drop capabilities.

“[Dealers] have a tool that they can easily tailor to address new risks,” Childers said, noting that the company has also rebuilt its software platform over the past few years. “If we can provide that flexibility, then we allow dealers to do what they should be doing best, and that’s not push paper but sell cars.”

Ad Loading...

ADP: Get Collaborative At the sprawling ADP Dealer Services booth, Product Marketer Chad Agler demonstrated the newly redesigned ADP Menu powered by MenuVantage, which launched Dec. 21. Agler said the company kept the beloved features of the previous version, but updated them to flow better and help F&I personnel adapt deals more quickly.

There were two key changes, Agler pointed out. First, the ADP menu is now tablet-friendly. Second, users can now customize F&I product columns to meet a customer’s needs. “You work with the customer to peel it down to what they really need,” he explained. “We wanted it to be more collaborative with the customer.”

The company is also halfway done with the development of its digital signing software, tentatively called See What You Sign. While the F&I manager is in ADP’s digital contracting workflow environment, he or she can walk customers through a queue of forms that are available to sign electronically, Agler explained.

ADP showcased a redesigned version of its ADP Menu powered by MenuVantage, which officials said retained the system’s most popular features. The new version is now tablet-friendly and allows users to customize F&I product columns based on the customer’s needs.

The program differs from traditional esign processes because it can be entirely conducted on a digital screen. “I could have swiveled this monitor portrait so we wouldn’t have to scroll at all. It could have been a touchscreen,” Agler said. “And if it were a touchscreen, I could actually touch that and it brings up a signing window and we could sign.” Agler said ADP considers the new program to be the next generation of econtracting, which — in its current state — is “not ideal,” Agler said.

Customers using See What You Sign will approve each signature. The program then takes the identity, the intent and the authorization and seals it in the document. After the signing is completed, the digital deal jacket can be rendered into a flattened PDF, placed on a flash drive and handed to the customer, Agler noted.

Ad Loading...

ADP partnered with Silanis, an e-signature software provider, on the project.

The firm's F&I Insight tie-up with The Impact Group’s ImpactMenu platform is designed to enhance finance-and-insurance transaction recording for auto dealerships.