Auto finance sources reveal that they, too, are focused on the customer experience, and say they are ready for what’s expected to be another great year for auto sales.

The auto finance community arrived in San Francisco in January charged up about a year in which new-vehicle sales could match the third highest total in auto retailing history, according to the National Automobile Dealers Association (NADA). They maintained that origination strategies remain unaffected by the current regulatory climate and scoffed at media claims of a forming bubble in the subprime auto finance arena.

The week started on Jan. 20 with the American Financial Services Association (AFSA)’s two-and-a-half-day Vehicle Finance Conference, which fed into J.D. Power and Associates’ one-day Automotive Summit and concluded with the 98th annual NADA Convention & Expo. Even when shown metrics that could indicate a return of the volume race that preceded the 2008 financial crisis, the message from finance execs — and even market analysts — was the same.

Ad Loading...

“There’s a lot of press on that,” said Tim Russi, president of automotive finance for Ally Financial. “I don’t see it as an issue, and I can’t find a colleague who does.”

During the Vehicle Finance Conference’s CEO Panel, Dan Chait, president of World Omni Financial Corp., added, “Before the downturn, it was a race to the bottom. The industry does seem to be showing more discipline now, which is very encouraging.”

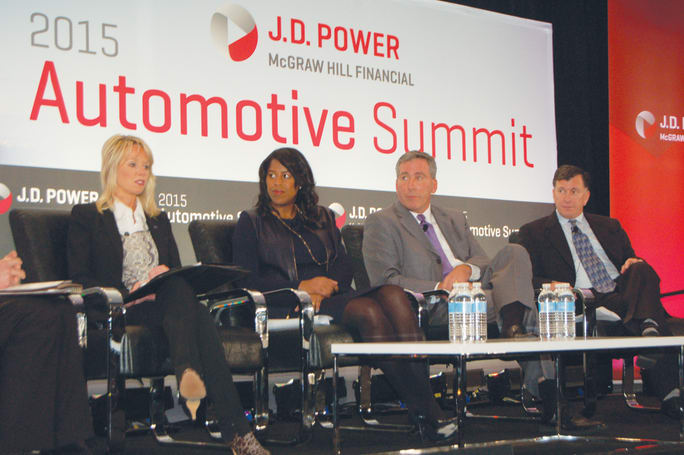

They did acknowledge, however, that the competitive climate is heating up. “Competition is fierce out there,” said Thasunda Duckett, CEO of Chase Auto Finance, as she pointed to Ally’s Russi and Ford Motor Credit’s Joy Falotico during the auto finance panel at the J.D. Power event.

Telling Absence The Vehicle Finance Conference kicked off less than two months after Honda’s and Toyota’s captive finance arms revealed in regulatory filings that they are the latest targets of the Consumer Financial Protection Bureau (CFPB)’s investigation into compensation policies that allow dealers to mark up interest rates on consumer finance contracts in exchange for services rendered. But missing from the AFSA’s 2015 program were bureau representatives, although the association did dedicate a 45-minute general session to “Regulatory and Legal Uncertainties.”

The session, moderated by Bill Himpler, executive vice president of the AFSA, kicked off the same day the U.S. Supreme Court began hearing opening arguments in a housing discrimination case that could result in the high court declaring that the disparate impact theory — the CFPB’s main weapon in its scrutiny of dealer reserve — does not belong in fair lending laws like the Fair Housing Act (FHA) and the Equal Credit Opportunity Act (ECOA).

Ad Loading...

Mark Kenney, chairman of the law firm Severson & Werson, was still checking emails as he provided his analysis of the opening arguments. He echoed what many legal insiders believe — that the five-justice conservative majority on the Roberts Court will not view disparate impact kindly. But with Justice Antonin Scalia signaling, at times, that he might be willing to vote to allow disparate-impact claims, Kenney acknowledged it wasn’t an open-and-shut case.

The American Financial Services Association opened Day 3 of the 2015 Vehicle Finance Conference with its annual CEO Panel. It included Tim Russi, president of auto finance for Ally Financial, Jason Kulas, president and CFO of Santander Consumer USA, Kirk Cordill, president of BMW Financial Services, and Dan Chait, president of World Omni Financial Corp.

“The CFPB is hanging on this just as much as the association is,” Kenney said, noting that a ruling could come as soon as April and as late as June, when the current court session ends. Himpler, however, said he expects a ruling to come sooner rather than later, adding that the justices have been briefed on the issues involved.

Himpler noted that one of his CFPB contacts indicated the day before the hearing that the bureau may “kind of slow things up for the next 45 days” until a ruling is made. And that’s despite CFPB Director Richard Cordray having said there’s no correlation between the ECOA and the FHA, Himpler added.

The case and the CFPB were barely mentioned during the conference’s CEO panel the next morning, although Ally’s Russi, after saying he welcomed the CFPB, admitted that completing the company’s April 2014 initial public offering was behind its decision not to fight the auto-loan discrimination claim made by the CFPB and DOJ in December 2013. Instead, it signed the $98 million consent order to resolve allegations that its dealer participation policies resulted in minorities paying higher interest rates than nonminority customers.

What Bubble? But how finance sources compensate dealers isn’t the only area being scrutinized. Since the summer, state and federal regulators have keyed in on subprime auto originations and securitizations, issuing subpoenas to several finance sources, including Ally, Capital One, Consumer Portfolio Services, Credit Acceptance Corp., GM Financial, and Santander Consumer USA, requesting documents related to their subprime auto finance business.

Ad Loading...

The subpoenas were delivered after a series of articles critical of subprime auto lending appeared in The New York Times — one of which was published online nine days before GM Financial received its subpoena last July. The articles seemed to play off the rise in below-prime financing at the close of 2013, with loans made to credit-challenged consumers accounting for 34.1% and 62.8% of new- and used-vehicle loans, respectively, in the end-of-year quarter, according to Experian Automotive. The reports linked that pickup in share to banks writing off “as entirely uncollectable” an average of $8,541 for each delinquent auto loan during the first three months of 2014, a 15% increase from the year prior.

What the reports didn’t consider was that subprime auto finance began to level off during the first half of last year, with the percentage of new-vehicle loans made to credit-challenged car buyers falling 22.1% during the second quarter to 15.1% — a level that was well below the pre-recession high of 19.9% in the second quarter 2007.

“When you think about subprime and read the headlines, there’s a bubble,” said Peter Turek, president of automotive for TransUnion, during the J.D. Power event’s auto finance panel. “But the numbers in the portfolio just don’t support it.”

Turek acknowledged that delinquency rates for subprime borrowers have risen from 4.2% in the third quarter 2012 to 5.3% in the third quarter 2014, but he noted that the segment’s contribution to the overall delinquency rate was muted because it maintains a very low share of total auto loan balances.

According to Experian Automotive, while the volume of loans in the subprime and deep-subprime risk tiers rose in 2014’s end-of-year quarter — 3.83% and 5.6%, respectively — the combined share of the two segments was down slightly from the year prior. In fact, the only risk tier to show a year-over-year increase in market share was superprime.

Ad Loading...

“So the idea of seeing this big subprime bubble doesn’t hold when comparing the historical trend,” said Melinda Zabritski, Experian Automotive’s senior director of auto finance, during the firm’s NADA press conference on Jan. 23. “We’re not seeing unrestrained growth in subprime.”

Victims of Success What regulators can’t ignore is that auto loan balances approached $1 trillion in the fourth quarter 2014 — Experian Automotive putting the actual number at a record $866 billion, while Equifax, which reported that auto loans now account for 33.2% of total nonmortgage consumer debt, put the total at a record $975 billion.

The 2015 Vehicle Finance Conference featured a general session on “Regulatory and Legal Uncertainties.” Moderated by Bill Himpler (center), executive vice president of the American Financial Services Association, the panel included Dan Soto (left), chief compliance officer for Ally Financial, and Mark Kenney, chairman of Severson & Werson.

Balances could climb even higher this year, with NADA Chief Economist Steven Szakaly citing an expected pickup in the housing market, a strong unemployment outlook and low gasoline prices as reasons for his 16.94 million-unit projection for 2015 new-car sales — a total not realized in 10 years. About the only thing holding back the industry from realizing some of the loftier predictions of 18 million and 20 million units are wages and income, which remain at or below 2007 and 2008 levels.

“We need to see movement in [wages and income] to sustain vehicle growth,” Szakaly noted. “These low gas prices are helping to offset wage growth, but this is not a permanent situation.”

Last year, the industry sold 16.5 million units, with more than 80% of those sales being tied to some sort of financing, according to Experian Automotive. And thanks to low interest rates, stretching terms and leasing incentives, consumers had plenty of options to offset rising transaction prices, which, according to Experian Automotive, were tracking at more than $28,000 for new and $18,000 for used leading into the December sales month.

Ad Loading...

During the Vehicle Finance Conference’s CEO Panel, executives maintained that the market is competitive but disciplined, with Santander’s Jason Kulas noting that the industry seems focused on smart structures.

When the panel was asked if they were concerned about stretching terms, executives said the trend simply mirrors increases in ownership length and improved vehicle quality. “I think term will extend. Vehicle quality supports that,” said Ally’s Russi. “I don’t see it as a nice thing; I see it as a natural evolution of the quality of the vehicle.”

According to Experian Automotive, the 73- to 84-month term band accounted for 25.75% of loan volume during the months of October and November, while the 61- to 72-month term band, which Zabritski noted has always accounted for about 30% of the market, accounted for 40.3%. And with interest rates expected to increase this year — the NADA’s Szakaly predicting that the federal fund rate will rise 50 basis points by Sept. 21 — Zabritski said she expects to see terms stretch even further.

“Everyone’s doing it,” Zabritski said, noting that credit unions and finance companies are the biggest players in the 73- to 84-month term band. “But we’re not seeing people buying a Mercedes when they owned a [less expensive] car before. And we’re not seeing unrestrained growth in subprime.”

Improving the Experience When she described market competition as fierce, Chase’s Duckett noted that pricing is only the first step toward competing in today’s marketplace. “In addition to a competitive rate, dealers are looking for lenders to constantly step up,” she said.

Ad Loading...

Duckett listed faster response times and understanding dealer needs as areas on which finance sources are competing. Auto lenders are also targeting the push to improve the customer experience, specifically transaction times, as an area on which they can compete. As Ally’s Russi noted, the fear customers have of automotive retailers, whether deserved or not, has been a black eye for the industry.

On the J.D. Power auto finance panel was Ford Motor Credit’s Joy Falotico, Chase Auto Finance’s Thasunda Duckett, Ally Financial’s Tim Russi and TransUnion’s Peter Turek.

“As the industry works to solve that, I think the lenders have a role in that,” he said.

In 2013, Ally launched its Relationship Management Center, an online lead-generation platform that doubles as a professional marketing fulfillment service. It was designed to keep dealers connected with finance and lease customers across the life of their contracts. In January 2014, the finance source updated the platform to allow dealers to submit lists of customers for preapproval. Dealers can then use Ally’s RMC to run direct mail campaigns containing firm offers of credit.

Kulas said Santander has made similar investments in technology to improve data flow to streamline the credit application process or to automate employment and income verifications for repeat customers. “We made a very big step forward in trying to reduce the amount of time in that data gathering,” he said.

Kirk Cordill, president of BMW Financial Services, said the captive is piggybacking on its OEM’s “Apple genius” push. Launched last year, the initiative called for dealerships to designate noncommission-based sales representatives to educate consumers about BMW’s products in a no-hassle environment. Cordill said that doesn’t mean the captive will have “BMW Financial geniuses,” however.

Ad Loading...

“We’re trying to move upstream, being able to provide firm offers to those lease-end customers so we can educate them more,” he said, noting that the captive’s self-inspection program for lease-return customers represented another step the captive has taken to improve the experience.

Even credit unions are exploring ways to improve the customer experience. On the show floor at NADA 2015, CU Direct (CUDL), which delivered $22 billion in credit union-originated auto loans last year through its point-of-sale lending platform, showcased a new car-buying site called AutoPremiere. It promises no-haggle pricing for credit union members, offers a call center to set up in-dealership appointments, and has about 10 to 15 committed credit unions in the Utah, Boston and Sacramento, Calif., markets and more than 300 dealers signed onto the program.

“AutoPremiere delivers sort of that millennial experience, where customers can get 90% of the transaction done before they get to the dealership,” said Tony Boutelle, the firm’s president and CEO.

Also on the NADA show floor was Dawn Harp, who heads up Wells Fargo’s dealer services business unit. She said improving the customer experience will be a key focus for the bank this year, starting with its origination system.

“It’s a big initiative right now. How can we enhance our workflow, how can we provide faster service and response?” she said. “Everybody’s looking for ways to make the experience more transparent and streamlined.”

Ad Loading...

But as Ally’s Russi noted, solving the customer-experience puzzle will require an industrywide effort. “The experience starts outside the dealership and comes into the dealership. The real challenge right now is how do you make that experience the same all the way through,” he said. “Over the next couple of years, the industry is going to examine all these touchpoints.”

As for the year ahead, Russi said: “I think 2015 is going to be a very interesting year. Liquidity is strong. And the market is in a good position to take on rising rates at some point. I think we’re all ready for it when it occurs.”

CUDL’s Boutelle added: “It’s a hard market to fail in.”

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.