Automotive Industry Sees New Vehicle Finance Shift Back to Pre-Pandemic Levels in Q2 2021

Overall, the data shows encouraging signs for the automotive finance market.

Overall, the data shows encouraging signs for the automotive finance market.

IMAGE: Getty

The automotive finance market performed admirably during the pandemic, aided by strong incentives that kept it moving forward. Now, with Q2 2021 data, we can see a clearer picture of how COVID-19 impacted the market and the beginning of the return to more normal levels.

The most notable shifts were in new vehicle financing. In 2020, there was a large spike in the average new vehicle loan amount caused by a higher percentage of full-size trucks being financed, likely because of the heavy incentives that were offered. This leveled out in Q2 2021, as SUVs and crossover vehicles once again became the top segment financed. The average new vehicle loan amount was $35,163 in Q2 2021, down from the record high in Q2 2020 of $36,121.

To better understand the impacts of the pandemic, it’s helpful to not only do year-over-year comparisons, but to also look at Q2 2019 for context. Understanding the full context will be key to making the most strategic decisions as the market faces current challenges, such as the microchip shortage.

Two other areas returning to pre-pandemic levels are average interest rates and loan terms, which saw notable impacts from OEM incentives. The average new vehicle interest rate saw a notable drop between Q2 2019 and Q2 2020, from 5.7% to 3.95%, year-over-year. In Q2 of 2021, this saw a slight uptick, reaching 4.09%.

Looking at loan terms, the distribution is an indicator of the market returning to pre-pandemic levels. In Q2 2020, as part of incentive packages, we saw a notable increase in the percentage of loans falling into the 73- to 84-month category, with those terms making up 33.77% of new vehicle loans, compared to 30.28% in Q2 2019. We saw this diminish, coming in at 31.99% of loans in Q2 2021. Overall, the average loan term in Q2 2021 was 69.36 months, compared to 71.31 months in Q2 2020.

Consumer Preferences and Finance Trends

IMAGE: Experian

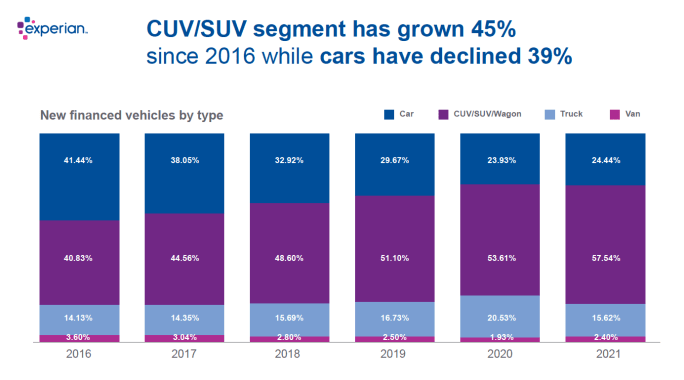

For some time now, the industry has been discussing affordability, and pointing to changing consumer preferences as one of the roots of the rising average vehicle loan amounts. The data demonstrates just how true this is for new vehicles. In Q2 2016, cars made up 41.44% of new vehicle financing, compared to 40.83% for SUV/CUVs, 14.13% for trucks, and 3.60% for vans. Since then, the most notable shift was in the SUV/CUV category, which now comprises 57.54% of financing, as of Q2 2021, while cars made up just 24.44%. The truck segment also saw some growth, reaching 15.62%, while vans decreased slightly to 2.4% in the same time frame.

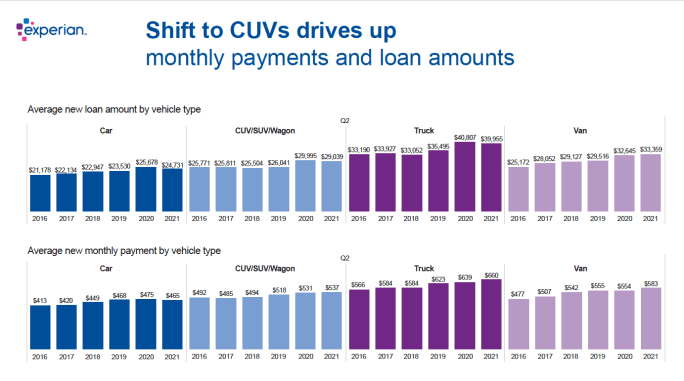

Looking at the average vehicle loan amount for these segments gives further context for the rising average vehicle loan amounts. In Q2 2016, the average loan amount for a car was $21,178, while an SUV/CUV was $25,771, and $33,190 for a truck. As of Q2 2021, the average new loan amount increased most notably for the truck segment, with the average new truck loan reaching $39,955. Cars and SUV/CUVs have seen increases in the same time frame, with the average car loan increasing to $24,731 and the average SUV/CUV loan reaching $29,039 as of Q2 2021.

IMAGE: Experian

In Q2 2021, the Honda CR-V was the most financed vehicle (2.93%), followed by the Chevrolet Silverado 1500 (2.6%) and the Honda Civic (2.51%). It’s important to keep in mind that these trends will continue to impact the used vehicle market for years to come, as the larger vehicles enter the used market.

Finance Market Share Levels Out

One of the biggest trends to come out of the pandemic was a significant jump in captive lenders’ market share of vehicle financing, as incentives helped keep the market moving forward. Now, this has shifted for both new and used financing, and we’re seeing things level out.

In the second quarter of 2021, all lenders saw increases in new vehicle financing market share, compared to captives, with the most significant growth occurring for banks. Banks increased from 22.81% in Q2 2020 to 27.28% in Q2 2021, while captives decreased to 55.33% in Q2 2021, from 62.21% in Q2 2020. Rounding out lender market share is credit unions (11.16%) and finance companies (4.77%). The alterations in captive and bank market share is another indicator of the market returning to more normal levels, which can be seen by comparing to Q2 2019, when captives comprised 54.34% and banks made up 27.64%.

For the used market, banks and finance companies saw growth vs. captives, with banks growing to 33.91% of financing, compared to 32.5% in Q2 2020. Finance companies increased market share from 16.04% in Q2 2020 to 16.48% in Q2 2021.

Overall, the data shows encouraging signs for the automotive finance market. As we face ongoing and new challenges, data will be crucial for enabling lenders to understand the market and make the most informed decisions for the future.

Melinda Zabritski is Experian’s senior director of automotive financial solutions.

More Auto Finance

Mastering Credit Friction

In this video, Josh Krach explains how to turn credit friction into an advantage.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Auto Lenders, Consumers on a Tightrope

April borrowing data shows that more consumers are bending over backward to buy vehicles, though subprime lending cooled off for the month.

Read More →

Toyota Financial Services President Replaced

Scott Cooke has served in various roles with Toyota Financial Services for over 20 years, including president and CEO, which he retires from on June 30.

Read More →

Permission or Approval: When to Notify Finance Sources

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Read More →

At-Risk Auto Borrowers Drive Looser Credit Access

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Read More →

Auto Loan Forecast Bucks Market Trend

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Read More →

Auto Credit More Plentiful

Growing access shows greater lender appetite for risk as consumers take on heavier debt burden in an inflated market.

Read More →

Auto Loans Long as Stretch Limos

More consumers, faced with ever-rising car prices, are adapting by agreeing to longer loan terms despite the cost of added interest payments.

Read More →

AutoPayPlus Launches RePayPlus

The reinsured biweekly payment program offers auto dealers with customer retention and reinsurance structure.

Read More →