Black Book: Weekly Market Report

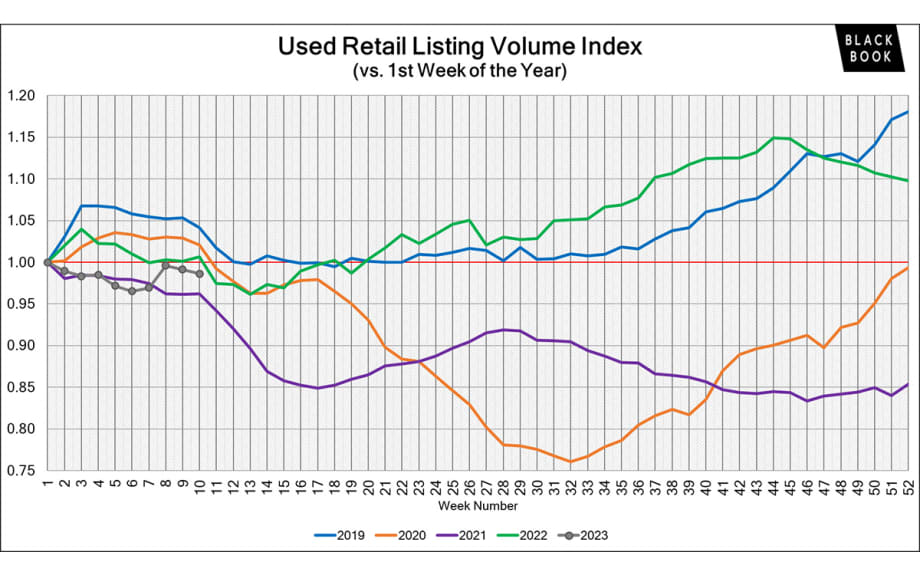

Used-retail active listing volume index index sits at 0.99 points.

The used retail active listing volume index sits at 0.99 points.

IMAGE: Black Book

Wholesale Prices, Week Ending March 11

The market reported the largest single week increase in quite a while last week. The Last time we had a similar gain in the market was November 2021. Activity at the auctions continues to be abundant with no-sales on vehicles, not from a lack of bidding, but instead due to sellers holding firm to their floors.

This Week Last Week 2017-2019 Average (Same Week)

Car segments +0.46% +0.46% -0.12%

Truck & SUV segments +0.43% +0.30% -0.34%

Market +0.44% +0.35% -0.25%

Car Segments

On a volume-weighted basis, the overall Car segment increased +0.46%. For reference, the previous week, cars increased by +0.46%.

Seven of the nine car segments increased last week.

Sporty cars had been on a hot streak, with seven consecutive weeks of increases that averaged +0.47% gain each week. However, last week the rate of gains finally slowed down to +0.14%.

Subcompact car was the only segment to have a gain exceeding 1%. This is the first time this segment has had more than a 1% increase in a single week since May 2021.

Prestige luxury car depreciation has slowed to the lowest the segment has seen since July 2022.

Truck/SUV Segments

The volume-weighted, overall truck segment increased +0.43%, compared with the prior week’s increase of +0.30%.

Eleven of the 13 truck segments reported increases last week.

Compact crossover has been increasing for six consecutive weeks, for an average weekly gain of +0.46%. Last week, the segment far exceeded that, with a single week increase of +0.92%.

Full-size trucks are still in positive territory, but the rate of gain slowed last week to +0.10%, compared with the week prior at +0.15%.

Weekly Wholesale Index

The graph below looks at trends in wholesale prices of 2- to 6-year-old vehicles, indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Calendar years 2020 and 2021 ended with used wholesale prices at elevated levels. With economic patterns including the automotive market driven by the pandemic, normal seasonal patterns in the wholesale market, for example, 2019 calendar year, were not observed for most of the last three years. We saw a similar picture in 2009 at the end of the Great Recession. Calendar year 2021 did not have typical seasonality patterns, as the market had rapid increases in wholesale values for most of the year. The Wholesale Weekly Price Index reached the highest point of the year at the end of December 2021, reporting over 1.51 points. In 2022, the price index was on a mild rollercoaster until July, after which point prices were on a continuous decline until the end of the year.

Retail (Used and New) Insights

Volkswagen confirmed that the U.S. will get the long-wheel base version of the much-anticipated ID.Buzz, its all-electric Microbus. The van will be a 2024 model year and is expected to debut in June, but sales will not be until at least the second half of this year.

Mercedes-Benz made headlines last week with the release of pricing for the EQE SUV. The all-electric crossover will have the RWD and AWD entry-level trims with the exact same pricing.

Nissan’s production of the all-electric crossover Ariya is hitting some slowdowns, so the manufacturer has stopped taking reservations until kinks in the assembly process can be worked out.

The Ferrari Purosangue, the brand’s first four-door model, will be available to customers later this year.

Used Retail Prices

Used retail prices are more accessible than in years past due to the proliferation of "no-haggle pricing" for used-vehicle retailing. Transparent pricing upfront makes the car-buying process more enjoyable for customers and allows Black Book to accurately measure retail market trends.

At the onset of the pandemic, in CY2020, used retail prices increased slightly, following typical seasonal patterns, then began dropping in April, finally hitting a low point in the late spring months. By late summer of CY2020, they increased as supply of new-vehicle inventory started to become scarce, but retail demand slowed at the end of CY2020, resulting in declining retail asking prices for the last several weeks of the year. When CY2021 kicked off, demand rebounded while retail prices lagged slightly behind wholesale prices; March of 2021 started the dramatic increases in prices fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up the pace once again to start the fourth quarter, when prices on retail listings steadily increased week after week. As CY2021 came to an end, the retail listing price index closed 36% above where the year began. The index then remained relatively stagnant through most of CY2022. In the fourth quarter, the Retail Listings Price Index declines started but not as steep as the wholesale price index.

This analysis is based on approximately 2 million vehicles listed for sale on U.S. dealer lots. The graph below looks at 2- to 6-year-old vehicles. The index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

The used retail active listing volume index reverted back to one at the start of 2023. Currently, the index sits at 0.99 points.

The used retail days-to-turn estimate is around 51 days.

Wholesale

The market continues to heat up, with values increasing each week at levels well above what is typical for a normal spring/tax season market. Some segments are now reporting single-week increases reminiscent of the market during 2021. Conversion rates have not returned to the same level yet, but it has not been for lack of interest from buyers. Despite very active bidding across the country, the no-sales are due to sellers holding firm on their floors. Despite the positive news from the auction lanes, much of the dealer sentiment is concern for the amount of negative equity that customers have on their vehicles they are looking to trade.

The estimated average weekly sales rate increased to 52% last week.

Originally posted on Auto Dealer Today

More Showroom

State Follows Federal Warning on Auto Ads

The Massachusetts attorney general cautioned the state’s automotive dealers to be upfront with the consuming public about their vehicle prices or risk punishment.

Read More →

European EV Market Hits Record

Seven out of the top 10 electric vehicles sold so far in 2026 in Europe are by European brands, and automakers are seeing the power train fill up their order books.

Read More →

Used EVs Outpace New

While North American electric-vehicle sales remain down year-over-year, May sales saw a 3% increase from April’s numbers as used EVs led the market.

Read More →

New Vehicles Down for Most Brands

Healthy May sales cut into inventory as automakers kept a tight reign on supply, though some brands ended the month with excess units on the ground.

Read More →

Auto Prices Ride May Moderation

Flat ATPs and asking prices clocked in below long-term averages for the month, though some segments saw significant price gains, reported Cox Automotive.

Read More →

Mitsubishi Sets Growth Strategy, Structural Transformation

The Japanese automaker aims to 'strengthen products and technologies that embody its brand identity,' focus on its strongest markets and expand value-chain businesses 'that leverage its unique strengths.'

Read More →

Affordable, Safe Cars for Teen Drivers

Families looking to balance affordability and safety in vehicles for their teen drivers can look to the updated list of recommended vehicles by IIHS and Consumer Reports.

Read More →

Auto Dealers Feel Better But Not Great

A second-quarter Cox Automotive poll of franchised retailers and independents found better views of the current market after a good spring but anticipation of third-quarter storminess.

Read More →

Holman Opens Porsche Dealership in Miami

The North Miami store features the brand’s signature Destination Porsche design concept, combining contemporary architecture and technology to create what the auto group calls an ultra-luxury experience.

Read More →

Chicago to Gain Cadillac Rooftop in 2027

The two-story Cadillac dealership is being constructed at the former Lincoln Yards site, owned and operated by Canada-based Jack Carter Auto Group.

Read More →