CFPB Needs a New 'Tool,’ Study Finds

F&I and Showroom delves into a new study commissioned by the American Financial Services Association. It concludes that the CFPB’s use of the BISG proxy method is “conceptually flawed” and could lead to overstatement of alleged harm to consumers.

WASHINGTON — Almost a year after making the pledge, the American Financial Services Association (AFSA) delivered this week a study that addressed the Consumer Financial Protection Bureau (CFPB)’s concerns regarding dealer participation. Its conclusion: The bureau needs a new “tool” for examining disparities in dealer markups.

Commissioned by the AFSA, the study characterized the bureau’s use of the Bayesian Improved Surname Geocoding (BISG) proxy method to measure disparities in dealer reserve as “conceptually flawed,” with the authors, Boston-based Charles River Associates (CRA), adding that the potential biases and estimation errors could contribute to the overstatement of alleged harm to consumers.

“Our research concludes there is very little evidence that dealers systematically charge different dealer reserves on a prohibited basis,” the study, “Fair Lending: Implication for the Indirect Auto Finance Market,” concluded. “Rather, variations in dealer reserves across contracts can be largely explained by objective factors other than race and ethnicity.

“In addition, the use of race and ethnicity proxies creates significant measurement errors, overestimates the population counts and results in overstated disparities.”

The CFPB began regulating the auto finance industry in March 2013. That’s when it issued guidance stating that finance sources that offer auto loans through dealerships will be held responsible for discriminatory rate markups on retail installment sales contracts. But since auto finance sources are prohibited from collecting race and ethnicity data, CFPB examination teams must rely on the proxy method to identify a consumer’s race and national origin when evaluating a finance source’s compliance with fair lending laws.

To proxy for race and national origin, the bureau relies on data associated with consumers’ last names and places of residence. Census Bureau data is first used to calculate the probability that an individual belongs to specific race and ethnicity based on their last name. Exam teams then update that probability based on the demographics of the area in which the person resides using the same Census data.

That was the formula used when the bureau and the Department of Justice alleged last December that Ally charged 235,000 African-American, Hispanic and Asian/Pacific Islander borrowers between $200 and $300 more in interest charges over the term of the loan. Ally agreed to pay $98 million to settle those charges.

“Ally does not engage in or condone violations of law or discriminatory practices,” the finance source said at the time. “And based on the company’s analysis of it business, it does not believe that there is a measurable discrimination by auto dealers.”

The CRA’s study seemed to back the finance source’s claim.

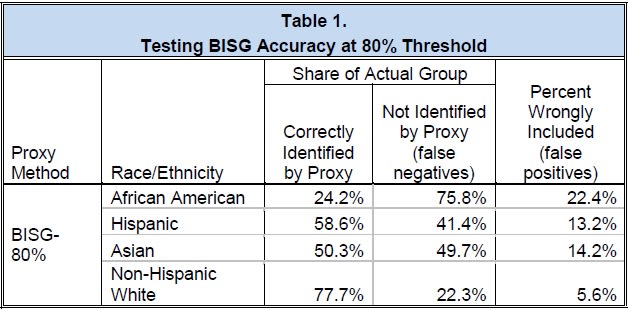

To measure the accuracy of the BISG proxy method in determining race and ethnicity, authors of the CRA’s study tested it against a sample population of mortgage data that included race and ethnicity. And even with an 80% probability that a person belongs to an African-American group, the proxy correctly identified race less than 25% of the time. And when used to identify disparities in interest paid, the BISG methodology inflated disparities for African-Americans by 87%, the study noted.

The study also tested the CFPB’s proxy methodology on more than 8.2 million new- and used-vehicle finance contracts issued between 2012 and 2013. The average amount financed of those contracts was $25,525 for new vehicles and $18,753 for used. Dealer reserve on those deals averaged 110 basis points for new and 132 basis points for used.

Ignoring proxy bias and other market factors that might influence reserve, the firm estimated that disparities in the contracts were 17 basis points for African Americans, 9 bps for Hispanics and 13 bps for Asian Americans. Adjusting for proxy bias and including observable factors impacting reserve, rate disparities fell to a range of 6-9 bps.

“Given the average amounts financed and contract terms in our data, this equates to less than $1 of monthly payment, or approximately 0.2% of the average monthly payment amount,” the study stated, noting that even that conclusion doesn’t consider unobservable factors that could influence reserve, such as beating a competitive rate.

But when the firm removed all contracts with zero reserve, adjusted for proxy bias and included observable factors that could influence rates, disparities fell even further. “Once we applied the same controls … we identify disparities of 5, 6, and 6 [for African Americans, Hispanic and Asian Americans], respectively,” the authors noted. “Disparities at this level are in the range of 50 cents to 60 cents per month and economically de minimis as a share of the average monthly payment.”

AFSA President and CEO Chris Stinebert added: “Alleged pricing discrepancies between minorities and nonminorities for auto finance rates are simply not supported by data. We have reviewed our study results with the CFPB and look forward to continuing our work with the bureau to address the issues we raised and to ensure consumers have access to affordable credit.”

The CRA’s study also looked at alternative dealer compensation structures such as flats, which the CFPB strongly recommended in its March 2013 guidance. The report concluded that about a third of all consumers would face higher costs of credit, regardless of race and ethnicity.

“If a compensation structure required flats, financial institutions would likely directly set the contract rate they offer to dealers,” the report stated. “The contract rates would have to be substantially higher than current buy rates in order to pay flats on every contract.

“Dealers would have an incentive to assign a given contract to the financial institution offering the highest flat rate,” it added, noting that market competition and rate caps employed by finance sources already incentivize dealers to collect their reserve on the lowest buy rate they can obtain.

Earlier this year, the NADA offered another option to address the CFPB’s concerns: the Fair Credit Compliance Policy & Program. Based on a fair credit risk mitigation model the U.S. Department of Justice developed in 2007 to resolve two dealer investigations, the program calls for dealers to document legitimate business reasons, such as beating a competing rate, for discounting interest rates from markup caps set by the finance source or state regulations.

“The way forward,” NADA President Peter Welch added, “is for the government to promote broad industry adoption of the NADA’s fair credit program, which would address fair credit risks where they matter — at the retail level.”

As for the study, Welch added: “The study shows the CFPB’s attempt to upend the auto lending process is insufficiently informed and the victim of flawed assumptions and inadequate peer review. Allegations of potential discrimination are explosive and certainly should not be made without a reliable foundation in data.”

Responding to a request for comment, the CFPB issued the following statement to F&I and Showroom: “We received the AFSA-commissioned report and will review it carefully. The CFPB is always interested in relevant data regarding important issues like discrimination in auto lending.”

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →