Consumer Advocacy Group Calls for Regulatory Review of F&I Product Pricing

The National Consumer Law Center is calling on lawmakers and regulators to investigate how dealers price F&I protections, claiming that an analysis of approximately 1.8 million vehicle transactions revealed inconsistent and discriminatory price markups over a span of six years.

WASHINGTON, D.C. — A consumer advocacy group is calling on lawmakers and state and federal regulators to investigate how dealers price F&I protection, claiming that an analysis of approximately 1.8 million vehicle transactions revealed inconsistent and discriminatory price markups over a span of six years in all 50 states and the District of Columbia.

The National Consumer Law Center (NCLC)’s findings — including that some dealers charged different consumers different prices for the exact same product purchased on the same day — are contained in a 58-page report titled, “Auto Add-Ons Add Up: How Dealer Discretion Drives Excessive, Arbitrary and Discriminatory Pricing.” The report also offers several recommendations, including that the Equal Credit Opportunity Act (ECOA) be amended to require documentation of a customer’s ethnicity for non-mortgage credit actions.

“These fixes are good for the market, for dealers, and finance entities themselves,” said John Van Alst, an attorney for the NCLC. “We certainly found that finance entities had an interest in limiting or stopping interest rate markups because it really hurt them. It increased the likelihood of default; it raised all sorts of problems. And those are things that both dealers and finance companies should want to avoid if we really want to have a healthy market in the long run and have people compete on a fair basis.”

Alst said the study’s findings are based on unprotected data posted online by a national F&I product provider. The data set included information on vehicle transactions from September 2009 through June 2015, which resulted in the sale of almost 3 million add-on products by more than 3,000 dealers.

Since the NCLC published its findings on Oct. 11, however, the unnamed product provider’s data has been taken off the web. Van Alst said the NCLC is not going to name the provider, because the group wants lawmakers and industry officials to focus on the study’s overall conclusion: that “inconstant pricing for the same add-ons leads to pricing discrimination.”

“This provider is representative of this market as a whole, and we’re really anxious to focus on the market rather than individual market rather than individual providers,” Alst said. “We aren’t naming dealers, either, for the same reason.”

The study offers several examples to back the group’s arbitrary markup claims.

There’s the Connecticut dealer who sold more than 1,000 window etching products with a dealer cost of $16 each. The dealer charged customers $189 for the product— a markup of $173, or 1,081%. Then there’s the dealer in Kentucky who charged most customers $69, $99, $199, or $299 for an etch product with a dealer cost of $55. Another dealer in Virginia charged customers between $1 and $1,995 for an etch product with a dealer cost of between $35 and $65.

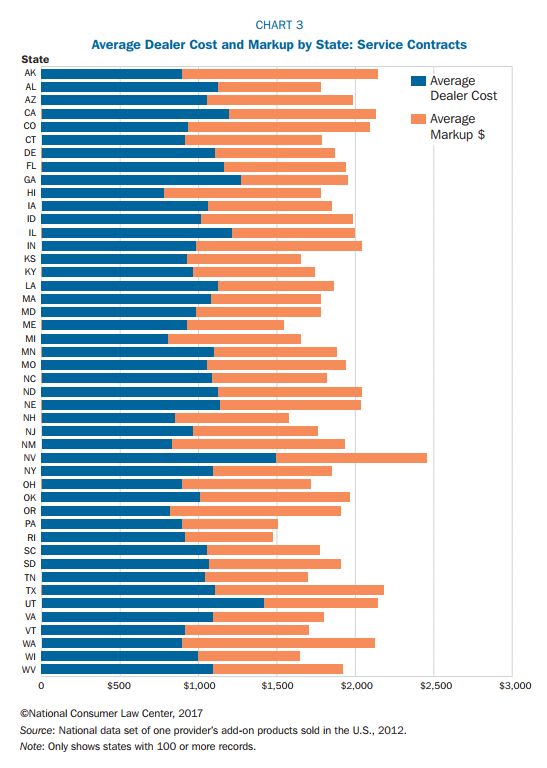

For GAP and service contracts, according to the study, 38 dealers averaged markups of 300% or more. Alst said NCLS focused more on the markup from dealer cost vs. pricing disparities when it came to products such as service contracts because it was difficult to account for different options and terms.

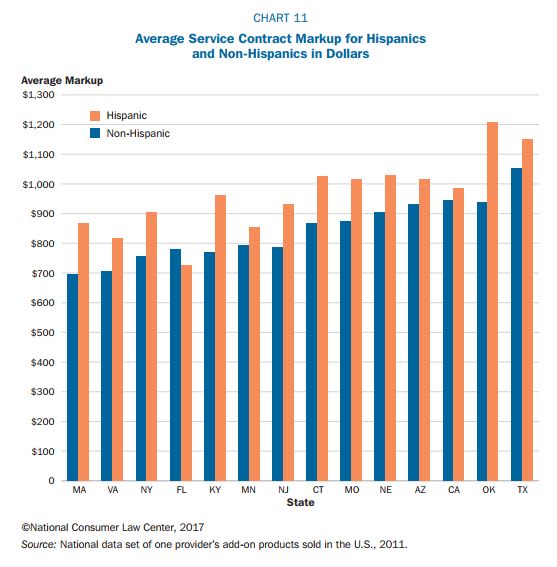

And since dealers and finance sources are prohibited by the ECOA from collecting race and ethnicity information on non-mortgage credit applications, the NCLS was limited to checking for pricing disparities between consumers with Latino surnames and non-Latinos. According to the report, the group found significant differences in what Latinos were charged in terms of percentage and dollar amount compared to non-Latinos.

In Oklahoma, for example, the average markup for a non-Latino was around 125%; for Latinos, it hovered around 170%. In Kentucky, non-Latinos averaged a markup of about $750; for Latinos, the average markup was around $950.

Alst admitted the group took some queues from the proxy methodology the Consumer Financial Protection Bureau (CFPB) used to examine rate markups, but said focusing on pricing disparities for Latinos only made the study’s methodology less susceptible to error.

“It would be more problematic if we used it as a proxy for African Americans, which is why we didn’t do that,” Alst said. “But, certainly, from everything we’ve been able to gather, it is relatively accurate.”

The NCLC called for more transparency, recommending that dealers post on their vehicles non-negotiable product prices along with the vehicle’s price. His group, however, also recommended that the CFPB, the Federal Trade Commission, the Federal Reserve Board, and state attorneys general mount an investigation into product pricing similar to the bureau’s examination of dealer rate markups.

Mentioned in the group’s report was U.S. Bank’s May 2015 decision to monitor its dealer partners’ “unexplained differences in pricing or excessive add-on product pricing.” Also cited was the Center for Responsible Lending’s now-discredited study on rate markups.

Alst said he has yet to hear from policymakers about any specific actions they’ll take based on the report’s finding, but noted that they have expressed interest in its conclusions. At the very least, he said, posting non-negotiable pricing for add-on products would reduce the likelihood that a regulator would take action against a dealer for discriminatory pricing. The National Automobile Dealers Association disagreed.

“Voluntary protection products are incredibly valuable for millions of consumers — just ask consumers who were made whole by GAP insurance on the total loss of their vehicles due to hurricanes Harvey and Irma,” the association said in a statement issued to F&I and Showroom. “But the NCLC’s approach of limiting consumer discounts on these products would only make them more expensive and harder to obtain for many consumers.

“When six in 10 Americans don’t have enough savings to cover a $500 emergency expense, we should be working to make these voluntary products more accessible and affordable, not less,” the NADA added.

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →