Inventory Shortage Inspires Fraudsters to Inflate Incomes

Financial crises have long served as a catalyst for fraudulent activity in the automotive industry.

Frank McKenna

Point Predictive

Across the economy, U.S. consumers are experiencing a surge in the price of new vehicles. The increased rates come as the demand for newer models exceeds the current supply. As a result, dealerships across the nation are witnessing a dramatic increase in auto loan fraud as consumers begin to inflate their annual incomes to secure favorable loans following aggressive hikes in interest rates amid the international inventory crisis.

The global shortage of semiconductor microchips has forced automotive manufacturers to halt production on nearly 1.2 million new vehicles since 2020, catapulting the automotive retail industry into an inventory crisis. Although supply chain analysts estimate that global supply-demand levels will reach equilibrium in 2023, the trickle-down effects of the inventory shortage will yield long-term consequences that will impact the automotive and adjacent industries for years to come.

Since its inception, the inventory shortage has driven up the price of new vehicles, increased the price and demand for used vehicles, and surged annual interest rates for auto loans. Consequently, the shortage has stifled consumers’ negotiating and purchasing power at dealerships across the globe.

The financial pressures accompanying the crisis have inspired fraudsters to re-engage fraud schemes that were popularized during the pandemic. Automotive loan fraud has increased by 260% since 2021, and fraud experts believe that this increase will be a long-term side effect of the global inventory shortage.

Automotive dealers were already reporting higher levels of synthetic identity fraud, income misrepresentation, and employment fabrication following the pandemic. However, the reports have reached record highs as consumers struggle to purchase and finance vehicles through honest means. That’s why fraud experts are urging dealers to remain vigilant in their efforts to prevent and combat fraud schemes involving misrepresentation.

History Has its Eyes on Fraud

As history will show, financial crises have long served as a catalyst for fraudulent activity in the automotive industry. During the financial recession of 2008, consumers stopped purchasing new vehicles due to a severe lack of disposable income. This, of course, had a trickle-down effect that closely resembles our current climate. At that time, auto lenders saw a significant spike in the levels of early payment default – much of which was caused by fraud and misrepresentation on applications.

Much like today, the financial pressures of the recession inspired consumers to finance used cars and, simultaneously, forced automotive dealers to drive up annual interest rates. Naturally, this affected loan performance, causing a rise in early payment default, or EPD, and delinquency rates. We are noticing similar trends in loan performance as U.S. inflation rates reach record highs.

In addition to the global inventory shortage, the U.S. is experiencing rapid growth in inflation rates as a result of the supply chain disruptions. Together, the global crises are creating economic challenges that are known to activate fraud. We turned to consortium data to determine the true relationship between ongoing global crises and recent fraud activity.

To What Degree is the Inventory Shortage and Inflation Impacting Fraud?

Using our consortium data, Point Predictive has identified a strong correlation between growing inflationary pressures, the ongoing inventory shortage, and fraudulent activity in the auto lending market. In our analysis, we found that loan applications are more likely to contain fraud during periods of economic instability. We discovered this using Point Predictive’s Auto Fraud Manager solution, which leverages loan-application data to generate a risk score that reveals an application’s likelihood of containing misrepresentation or early payment default risks. The higher the score, the greater the risk of misrepresentation or default.

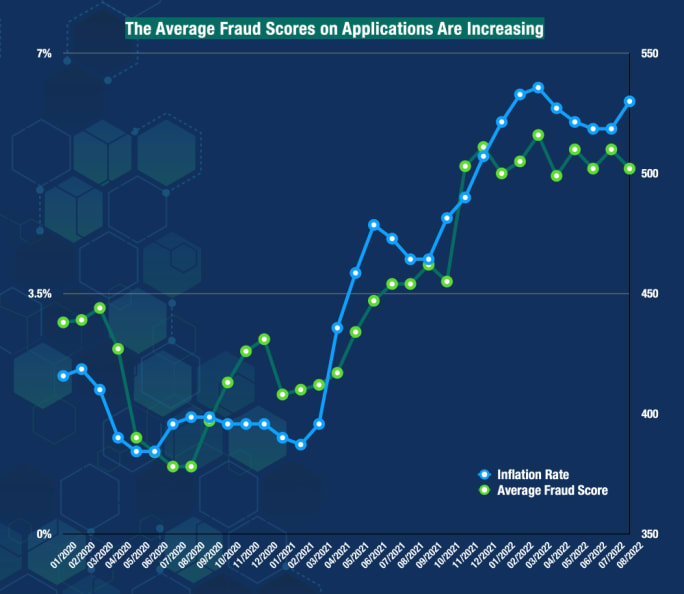

Inflation and average fraud scores

Point Predictive

To best understand the combined impact of inflation and the inventory shortage on fraud risks, we assessed the relationship between interest rates and EPD rates across the industry. Data from our analysis revealed a 0.76 correlation between EPD rates and inflation, meaning rising inflation rates are impacting consumers' ability to meet payment deadlines.

Further analysis indicated that climbing EPD rates are being driven by misrepresentation on loan applications. Evidence suggests that borrowers are marginally inflating their incomes to keep up with inflation rates and appear more attractive to sellers. The fact is that EPDs linked to income inflation have grown from 8% to 23% since March 2021.

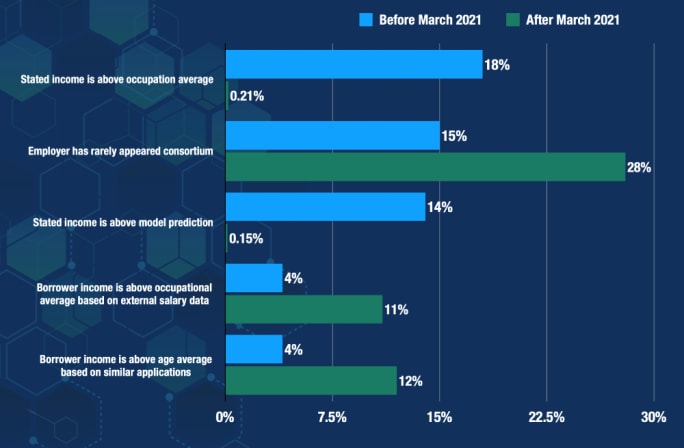

EPD and income misrepresentation

Point Predictive

Although it's among the most popular forms of misrepresentation, our analysis shows that income fraud is not the only type of fraud increasing with inflation and contributing to higher EPD rates. Data reveals that synthetic identity fraud, employment fabrication, pay stub falsification, straw borrower fraud, and collateral fraud are also on the rise.

Fraud is growing at an alarming rate, and dealers have to combat suspicious activity to avoid costly buybacks from lenders. Being proactive and eliminating potential fraud risk could make the difference between a dealership keeping its doors open long after the inventory shortage has passed, or going out of business.

McKenna ischief fraud strategist at Point Predictive.

Originally posted on Auto Dealer Today

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →