S&P/Experian: Auto Default Rate Registers Largest Increase Since December 2011

Despite the nine-basis-point increase, the auto loan default rate remains near levels recorded one year ago. However, declining auto sales and the normal end-of-year push to make room for newer models may encourage easier credit conditions and raise concerns about future defaults.

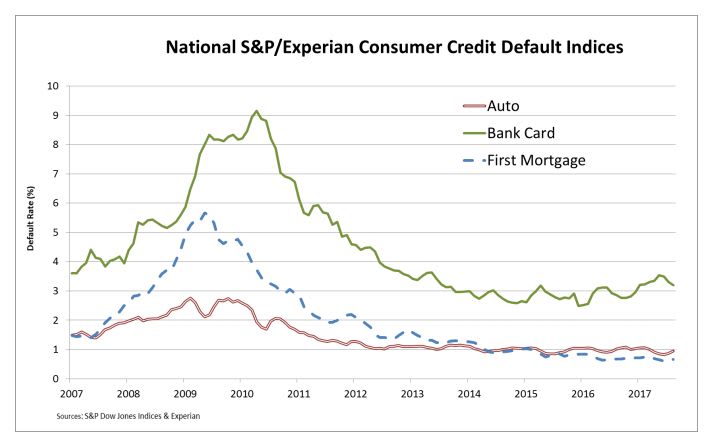

NEW YORK — Auto loan defaults in increased nine basis points from July to August, the largest month-over-month increase since December 2011, according to the S&P/Experian Consumer Credit Default Indices.

Despite the drop, the auto loan default rate remains low relative to historical levels. In fact, the rate is closer to levels recorded one year ago. The same is true for the composite rate for overall consumer defaults and first mortgage defaults, both of which increased three basis points from July.

“Overall, consumer credit defaults show no reason for alarm,” said David M. Blitzer, managing director and chairman of the Index Committee at S&P Dow Jones Indices. “Defaults on first mortgages are flat to down while defaults on auto loans have risen slightly in recent months. Consumer credit defaults on bank cards continue their upward creep since the end of 2015 despite a recent drop. The combination of an improving labor market, low inflation, and low interest rates are the principal factors behind currently favorable consumer credit conditions.”

The bank card default rate fell 12 basis points from July to 3.19% — the lowest level since December 2016. Bank cards were the only loan type to register a decrease in August.

Out of the five major cities analyzed by S&P/Experian, three registered increases in their default rates in August. New York recorded the largest increase, up 13 basis points from July to 0.95%. Los Angeles reported a rate of 0.66% for August, up three basis points from the previous month. Chicago came in at 0.94%, up four basis points from July.

Dallas reported a decrease of three basis points from the previous month to 0.74%, while Miami’s rate fell 10 basis points from July to 1.13%.

“Some future developments could affect consumer credit defaults: Auto sales have fallen since December 2016 and are down 11%. Declining auto sales and the normal end-of-model year push to make room for new cars may encourage easier credit conditions and raise concerns about future defaults,” Blitzer noted. “Hurricane damage in Houston and across Florida is creating substantial financial stress. The impact on mortgages on damaged or destroyed homes is not yet clear. Job losses and rising spending needs could lead to increased consumer credit defaults in coming months.”

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →