The Father of the F&I menu lays out a four-step process for converting the cash customer. He even throws in a technique for selling a VSC to those who refuse to convert.

My firm has studied just about every cash-conversion technique that’s popped up in the last 20 years. In fact, every time someone claimed to have a new technique for converting cash customers to dealership financing, somebody from my company was on an airplane to check it out. But the real results were always spotty at best. Why is that?

The reality is a lot of the techniques that have been taught through the years either didn’t work or were so difficult and time consuming that F&I managers didn’t even try them. Here are my Top 3 reasons many of these cash-conversion techniques didn’t pan out:

Ad Loading...

1. They simply weren’t used: A recent poll conducted by my firm showed that less than 15% of cash buyers were offered a finance or lease alternative at the time of sale, which is difficult to understand. But when time-consuming conversion methods don’t produce immediate results, F&I managers just quit using them.

2. Customer resistance to financial advice: Whether we deserve it or not, our customers have been told that dealers are going to try to deceive them and are not to be trusted. Therefore, they are wary of receiving financial advice from dealership personnel. No matter how sensible our approach is, many customers are simply unwilling to listen.

3. Alternative financing: A poll by our research group showed that 19% of customers who say they are paying cash are actually financing somewhere else. They tell us they are paying cash because they think they’ll get a better deal or because they simply don’t want to discuss their personal finances with a dealer. In many cases, the competing lender has counseled them not to discuss financing at the dealership.

The Process OK, so what actually works? Well, we have found that a cash-conversion process has to be easy to do, non-confrontational and simple enough for the customer to understand. It’s also important that you not confuse your customer. Unfortunately, offering financial advice and giving them choices at the same time tends to do just that.

We have had some fairly impressive results using a simple cash conversion technique developed a few years ago in the field by some of my firm’s top F&I managers. These individuals are successfully converting 20% to 25% of cash buyers to dealership financing. And the process takes just a few minutes. Here’s a step-by-step:

Ad Loading...

Step 1: Fill out your menu or whatever type of presentation tool you use to present products to finance customers. Use the most competitive rate you can.

Step 2: Present the financing options just as you would if the customer was already financing with the dealership. That means products should be included. If there is a rebate or trade, use that as a down payment. If there is no down payment, leave that space blank.

Step 3: Review the terms of the deal and ask the customer how he or she wants to handle the balance. When the customer says he or she will pay cash, tell them the total amount of the unpaid balance. Then say, “I’ll need a check for this amount. But before you hand over that check, you have some other repayment options. Of course, you can just pay cash; however, my job is to explain those other options and then you can choose. Would that be OK?”

Step 4: When you get the OK from the customer, begin reviewing the financing options available. Be sure to explain the different products before you let the customer choose. Doing this will allow you to present all of your products — including a vehicle service contract (VSC) — while also converting some of your customers to dealership financing along the way.

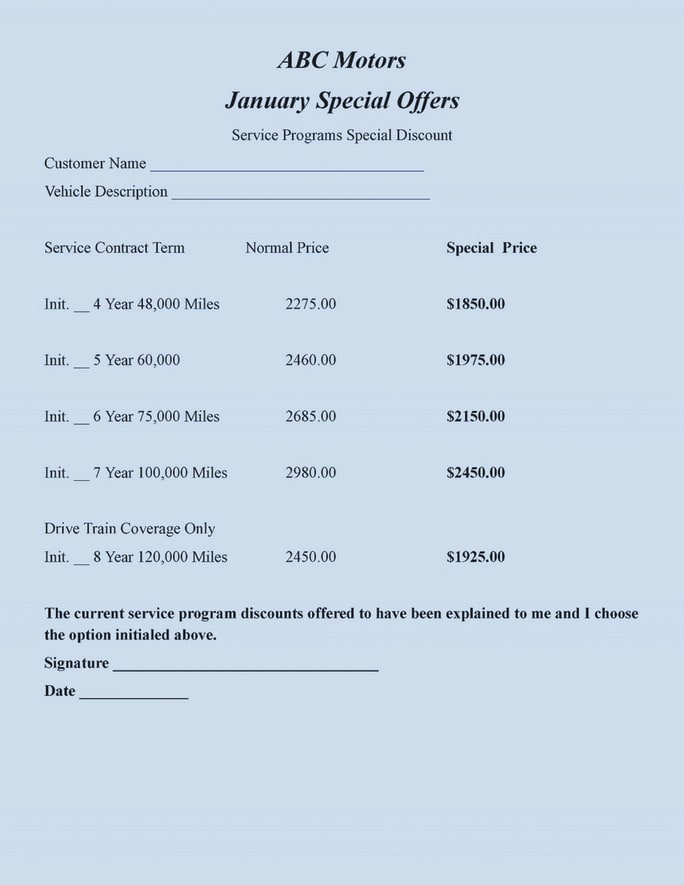

Providing a list of various VSC terms priced at a discount could help you increase VSC penetration with cash buyers.

So why do customers convert? Well, we polled some of the converted and they overwhelmingly cited low interest rates as the reason for saving their cash and choosing dealership financing. Hey, we have access to some of the lowest interest rates in our industry’s history. So be sure your customers are aware of that, because being able to secure a low interest rate is a prime motivator for cash customers to convert.

Ad Loading...

The key to making this technique work is discipline. In other words, you need to present all options to every cash customer, because you never know which ones will convert. So give it a try. You will find that simply informing customers of their options will be the best conversion tool in your arsenal.

VSCs and Cash Customers I know what you’re thinking. What about the other 70% to 80% who can’t be converted? Is it possible to sell them a VSC? The answer is “Yes.” See, there is a technique that’s working for several of our top-performing F&I departments that I’d like to share with you. This technique requires a little preparation and some creativity on your part, but our F&I managers are reporting an average of around 30% VSC penetration on “true” cash buyers using this approach.

To make this technique work, it is critical you run through the steps I outlined for converting cash customers to dealership financing. One thing to note, this process for selling VSCs to cash customers does not work in states with pricing controls on service contracts. Also make sure to run this by management before attempting this process.

F&I managers who are having the most success with this approach say they are conducting the entire cash-conversion presentation with the service contract included in the finance options presented. For managers using our Package Option menu, I’m referring to Step 2 on the menu.

Once the customer has clearly decided to stay with cash and has chosen whatever tangibles they do or don’t want, the F&I manager will offer one more option: a list of various VSC terms priced at a discount. One of our dealer clients uses a separate sheet to present his various VSC terms. It looks a lot like something a restaurant would use to display the day’s specials. Check out the example on this page. If you’d like to download a Microsoft Word version of this sheet, go to www.teamonegroup.com/freecashprocess.html. There you’ll find an accompanying video detailing how to properly use the form.

Ad Loading...

Now, the dealership that employs this special offer sheet simply runs through several term and mileage options before letting the customer choose. Remember, if you have already used the cash-conversion process properly, you have already explained the benefits of your VSC to the customer. So the presentation should be brief.

So give the processes I detailed a try and you may be surprised by how many customers will pick at least one option. It’s easy, simple and fast.

George Angus is the training director for Team One Research and Training, a company specializing in scientific, research-based program development and training. Email him at george.angus@bobit.com.

Credit card down payments, multiple vehicle purchases and even straw purchases can be completed without committing bank fraud, as long as you tell the bank first.

Cox Automotive’s index shows the subprime segment, long loan terms, negative-equity borrowers and down payment amounts all grew in February despite ever-higher vehicle prices.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.