Connection Commerce

The editor goes one-on-one with MakeMyDeal founder Mike Burgiss, who says his company is making progress in its drive to connect car buyers to dealers online. Can he do the same for F&I?

Mike Burgiss admits he’s more techie than car guy, but he believes tech firms attempting to transform car buying into a one-click, ecommerce experience have it all wrong. As he says, the future of car buying isn’t an Amazon-like shopping-cart experience.

Burgiss is general manager of MakeMyDeal, a Cox Automotive company he founded on the belief that car sales remain a relationship business that must be built on trust. He’s even given a name to that philosophy: Connection Commerce. To make it a reality, he developed an online communication platform where dealers and car buyers can connect and develop a relationship.

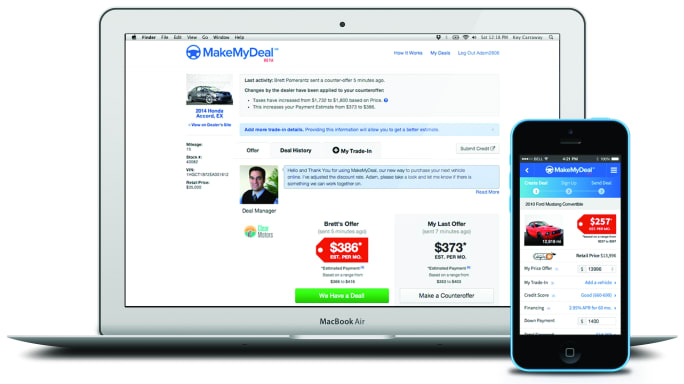

In simple terms, MakeMyDeal is an online deal-making tool that allows Internet shoppers to structure their deal on the dealer’s terms. Car buyers simply click on the “Start My Deal” tab on a participating dealer’s vehicle details page (VDP) to begin communicating with the dealership. They then calculate their monthly payment based on the price they negotiated online, their credit tier, desired term length, down payment, negative equity, and taxes and fees.

Burgiss describes a “typical” scenario in which the deal conversation begins on Tuesday, with the customer coming into the dealership the following Friday to confirm, not negotiate, the deal he or she structured online. He believes this process will address the issues detailed in Autotrader’s Car Buyer of the Future Study, results of which were released last April. The report found that only 17 out of the 4,002 car buyers polled preferred the current car-buying process. But it also revealed that 84% of respondents still want to buy a car in person.

But Burgiss notes the same study found consumers would like to negotiate on their own terms (56%) and want to do so anonymously until their deal is locked in (45%). As a 17-year veteran of ecommerce, display advertising and mobile technology, Burgiss admits he didn’t always subscribe to his own trust-based retailing philosophy.

In fact, Burgiss is listed as an inventor in 13 patents, 12 of which were the result of his work in voice-enabled mobile ecommerce — the same type of technology that allows Apple iPhone owners to ask Siri to pull up directions for nearby restaurants. In 2007, he was named director of advertising technology for Autotrader, where he earned his 13th patent. He also led the reengineering of the company’s website, as well as the creation of Autotrader’s big data and web analytics platforms.

Along the way, Burgiss hooked up with vAuto founder Dale Pollak, whom he credits with schooling him on the car business. In fact, it was at the National Automobile Dealers Association (NADA)’s 2013 convention in Orlando, Fla., that the two sketched out on a napkin the fundamental issue dividing consumers and dealers: Dealers want to maintain control while consumers simply want to know what their deal is.

That conversation led to the launch of MakeMyDeal in December 2013, with the beta platform becoming commercially available in June 2014. Since then, the firm’s dealer count has grown tenfold to 575 dealers.

Posing with staffers at his firm’s Atlanta offices, MakeMyDeal’s Mike Burgiss is a 17-year veteran of ecommerce, display advertising and mobile technology. He founded MakeMyDeal as an incubator business inside Cox Automotive. In December, the company graduated out of Cox’s New Ventures Group and is now aligned with the Dealertrack and Dealer.com part of the organization.

The platform continues to evolve as the provider tests new features. The company’s second product, which is currently in beta, is F&I Connect, an online self-penciling tool that allows car shoppers to calculate the monthly impact of an F&I product purchase. The system, which has the backing of several big-name agents and product providers, only provides real-time pricing for service contracts, but Burgiss said the plan is to extend the tool’s capabilities to other ratings-based products. F&I and Showroom went one-on-one with Burgiss to get a full progress report.

F&I: So the napkin-sketch story is true?

Burgiss: That’s how we started MakeMyDeal as an incubator business inside Cox Automotive. By the way, we graduated out of the Cox Automotive New Ventures Group in early December. So we’re now part of the Cox Automotive software organization, which is aligned with the Dealertrack and Dealer.com part of the organization. Now we’re even more tightly integrated with them, and the opportunity to really build the best solutions for dealers has become more readily available.

But the original charter was, “Mike, go figure out how we’re going to do ecommerce.” Dale and I knew we couldn’t solve online retail until we understood fundamentally what needs to evolve in terms of retail. So the little sketch we drew was a diagram that says, from the time the shopper and the dealer meet, they’re pulling in opposite directions.

Now this is where I start to get out on the edge a bit, but I believe in the next few years, there will be evolution in the automotive retail business around the stereotypical used-car salesman. We’ve already moved past it. The question is, how is the country going to move past that? Will the move be direct-to-consumer models where there’s no dealership? … I don’t believe that’s going to be it.

F&I: So how is MakeMyDeal performing in the market?

Burgiss: We don’t have a DMS pull. We think that imposes too much on the dealer. That means everything we do is based on a sample set of dealers who give us access to their CRM. Based on our sample sets, dealers can achieve closing ratios that are two times or better than email leads.

So if you get 100 email leads on your website, you might sell anywhere between four and 12 cars. If you’re using MakeMyDeal, you get fewer opportunities because people don’t know they can buy their car online just yet. But for the sake of example, if you get 100 deal proposals from consumers through MakeMyDeal, instead of four to 12, you’d sell eight to 24 or even more.

F&I: Tell me about the onboarding process.

Burgiss: We’re averaging 16 days from the time the dealer says “Yes” until they’re live. Then the training we provide goes on for months. Then we have an ongoing support model, which is carried out by our performance managers.

As for price, what I can say is that almost none of the more than 1,000 dealers we’ve presented this to have objected to the price of our subscription. In terms of the value MakeMyDeal delivers, dealers who are using the process I call “self-penciling” — where you’re working the car payment online — that element of their websites is over five times more engaging than the lead forms they have on their sites.

F&I: Tell me about F&I Connect.

Burgiss: If you want to quote a realistic monthly payment on a vehicle service contract, you have to rate it based on the car and the dealer’s financing terms. That means you need to know what credit tier the customer is in to get the right APR and terms. The last thing the dealer needs to determine is what his markup is going to be on the product above wholesale, whether it’s a dollar amount or a percentage. If you do all four things, now you can give your customers a realistic estimate of the product’s monthly payment.

And when you give them the option to choose the length of coverage and the deductible, they can see in real time how the payment changes. By doing this, you’ve lifted the curtain on how all the pricing works, which builds trust. And when customers trust, they buy more.

O’Neil said MakeMyDeal was integrated into Dealertrack’s network earlier this year. He revealed, however, that Cox Automotive is preparing to unveil its next version of digital retailing, which will connect the payment, the F&I experience, menu experience, and link trade-ins to Kelley Blue Book Instant Cash Offer.

F&I: I’m sure you’re aware the industry has been reluctant to move any part of the F&I process online.

Burgiss: The goal here is not to replace the F&I manager but to augment and extend the time the F&I manager has to speak with the customer. Today, you’ve got 30 to 45 minutes to complete the process, including all the regulatory items F&I managers have to deal with. So you don’t have a lot of time to explain the product benefits to the consumer.

So let’s say I’m in there on a Saturday. It’s busy. I say “Yes” and sign the deal sheet, not the buyer’s order. Then I say I’m coming in on Tuesday to take delivery. “Great, sir. When you’re at home, why don’t you review these options with your family.” Now you’ve got four days to allow that person to engage in the process, which, again, builds trust, educates the customer, and makes the conversation in the dealership all that much smoother.

F&I: That all sounds great, but you do realize not every F&I manager is going to embrace that, right?

Burgiss: I believe there’s a shift that will happen in F&I, which is that we have to price the product, not the customer. If you believe you’ve got to price the product, the online experience starts to make a whole lot more sense. If you don’t believe it, the regulators are going to make us get there.

F&I: But realize that a lot of F&I managers don’t even want their salespeople endorsing their products. They want that first objection to happen in their office to make sure the benefits aren’t misrepresented. Are you concerned you might create a situation in which consumers may decide to not buy any products before they even step inside the dealership?

Burgiss: Go Google “F&I products.” What do you see?

F&I: Nothing positive.

Burgiss: Right. As we see the vehicle purchase move more online, there are some players out there that want to go direct to consumers and bypass the dealership process entirely. If you think that won’t extend to F&I products, you have your head in the sand. What I would love to see happen is for dealerships to embrace this. When they do, all of this becomes Google content. In other words, the dealerships become what people are seeing, not the bad stuff.

F&I: So which F&I product providers are behind this?

Burgiss: American Financial & Automotive Services was our first connection. There are more, but the other names I can mention right now are JM&A and Wise F&I.

F&I: The F&I industry has been trying to update the F&I experience with tools like the tablet menu. How do those attempts play into F&I Connect?

Burgiss: The iPads are absolutely a component of this process, and the first version of our iPad solution will be out later this year. And as we talked about earlier, we’re just now beginning to engage Dealertrack and Dealer.com about what the product roadmap looks like.

Think about it at a high level. Dealertrack has a heritage of transactions. They fund loans and they’re really good at it. They know the transaction process very well. Autotrader has its heritage in consumer experience and engagement. MakeMyDeal was born out of that heritage.

F&I: Powering F&I Connect is F&I Express. Tell me about that relationship.

Burgiss: Cox Automotive owns slightly more than 49% of the company, and I’m one of the board members. So we’ve integrated into F&I Express to facilitate product ratings. So the way MakeMyDeal knows how much a dealer prices his or her F&I products is we get it from F&I Express, which, by the way, is the same econtracting platform the dealer uses in the store. And its connected to upwards of 80 providers. So that solves the problem of, “How do I present products from multiple providers?”

F&I: And F&I Connect was rolled out with select providers in June, correct?

Burgiss: Yes, and it’s in early testing right now. And every two weeks we release additional features and functionality to increase consumer engagement.

F&I: Can you share some early results of that testing?

Burgiss: We do have a handful of dealers that have some experience with F&I Connect, but we don’t see consumers adding F&I products to their deal structure online as the primary value and benefit to the dealer. We expect the consumer to engage the content and to engage in the self-penciling to learn about the product benefits and come up with a monthly payment for the products. And those activities are happening, but adding the product to their deal structure is so new to the consumer. This is going to be a process of engaging consumers in the coming years, not just over the next few months.

More F&I

Integrating Nontraditional F&I Products

The niche presents a strategic advantage for auto dealerships as they move to adapt to fast-changing consumer expectations in today’s market.

Read More →

Trust Is Personal

Technology, no matter how efficient, can’t replace what the human F&I manager can do, which is to bridge the divide between cyberspace and the in-store experience.

Read More →

Amplify 2026 Billed as Turning Innovation Into Results

Reynolds and Reynolds says its annual retail summit will connect dealers with practical strategies, peer insight, and technology-driven ideas.

Read More →

Own Your Outcome: F&I in the Digital Customer Journey

Finance has historically been the last step in the car-buying process, but it doesn’t have to be. The customer’s journey starts long before they arrive at the dealership, and so should F&I’s involvement.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

New Lifetime Battery F&I Product Meant to Drive Dealer Traffic

EFG Cos. offering is intended to create lifetime auto dealer engagement with customers.

Read More →

The Psychology Behind Menus That Increase Add-On Sales

There is a science to crafting a menu that gives customers confidence in the choices presented, and moving the process outside the F&I office can further boost results.

Read More →

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →