GAP rates are on the rise. Insiders say dealers should welcome the increases, adding that the performance of this core F&I product points to a severe slowdown in the next 24 months.

While auto finance execs continued to squash fears of a forming subprime bubble at the industry’s annual get-together in January, executives on the “I” side of the F&I equation say the performance of a core product tells a different story. Their advice to dealers is to start preparing for what they believe will be a severe slowdown in the next 24 months.

The product raising those alarms is GAP, which is designed to protect consumers by paying the difference between the value of a vehicle at the time it’s totaled (or stolen and not recovered) and the balance owed on the loan. For dealers, the product puts customers who suffered a total loss of their vehicle back in the market for a new car.

Ad Loading...

There’s just one problem: The frequency and severity of GAP claims — two key measures of the product’s health — are now reaching concerning levels.

Joseph Kirsits

“The rate that the frequency is deteriorating, from my perspective, is something that we haven’t seen before. I mean, these trends are getting bad,” says Joseph Kirsits, senior vice president of actuarial consulting firm GPW and Associates Inc. “But I’ve talked to other people in the industry who say they’re not seeing anything too alarming, so that’s the difficulty.”

Top of Mind While the rest of the industry was focused on new digital retailing solutions being rolled out at the 2017 National Automobile Dealers Association (NADA) Convention & Expo in New Orleans, most discussions in the F&I arena centered on the GAP situation. Executives say the alarms really started to go off last fall. The first rang during a Guaranteed Asset Protection Alliance (GAPA) event in October; the second at GPW and Associates’ F&I Reinsurance and Product Conference in November.

The consensus is that dealers should expect to see rate increases if their GAP providers haven’t done so already. The fear is that providers who have held off on raising rates to maintain production aren’t properly reserved for further deterioration. Executives offered several reasons for the product’s issues — some of which could cause problems for other core products like vehicle service contracts.

Scott Karchunas

“There was no better time to write GAP than 2008 and 2009. That was a great time,” says Scott Karchunas, president of Protective Asset Protection. “The lenders became more conservative and were less willing to fund loans at a 150% loan-to-value ratio. Now we’re on the other side, with longer loan terms and lenders are back to lending more aggressively again at 140% to 150%.

Ad Loading...

“So all these factors that were positive indicators for the GAP business are now turning negative. And you don’t add them together, you multiply them together,” he adds. “So claim frequency and severity accelerate quickly, and that’s what’s happening in this environment.”

Dave Borders, president of Allstate Dealer Services, says the F&I product provider has taken some rate increases and suffered “a little bit” in terms of production. But he notes that dealers who reinsure the product with the company appreciate the higher reserves. “It keeps them secure from having any undue pressure on their results,” he says.

“It’s being addressed, and we’re comfortable with where we are on that,” he adds, attributing the situation to a combination of soft lending and consumers simply driving more. “As a primary auto insurance provider, we’ve got excellent data that we’re able to bring into the dealer services program.”

And what his data shows is that insurance companies are totaling more cars because expensive components like vehicle sensors are increasing the cost to repair. At the same time, loan-to-value ratios are rising, more credit is being extended, interest rates are increasing, and loan terms are stretching.

More Accidents, Larger Claims

Ad Loading...

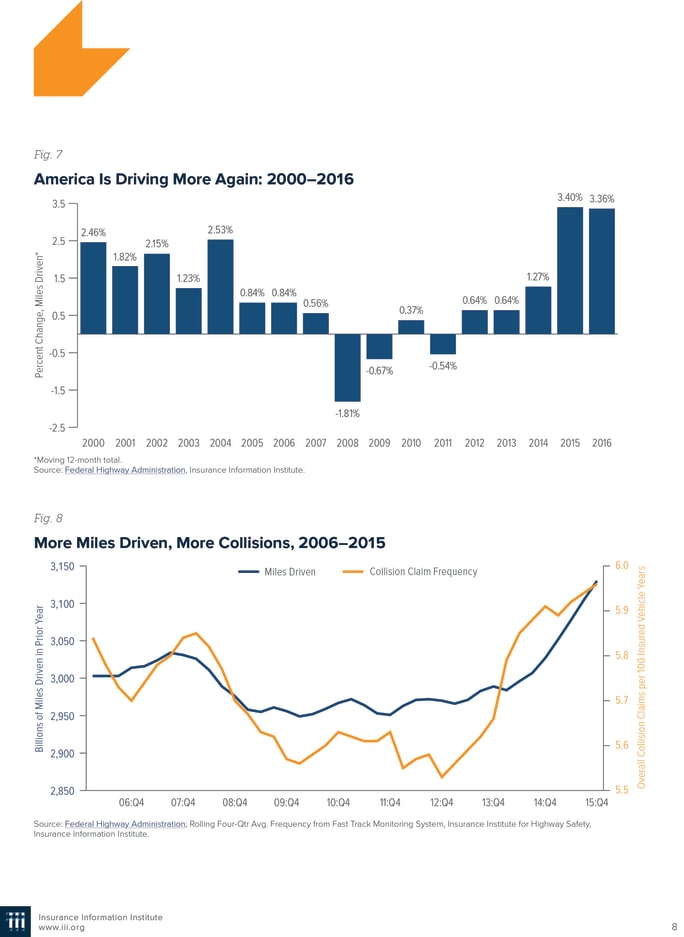

In October, the Insurance Information Institute (III) released a report titled, “Personal Automobile Insurance: More Accidents, Larger Claims Drive Costs Higher.” It shows that claim frequency rose 2.4% in 2013, 4.4% in 2014, and 0.8% in 2015. That’s more than 7% over the past three years, the report noted. Collision severity is also on the rise, increasing 8.2% over the past two years after several relatively flat years.

“It appears the immediate reason claim frequency is rising is that people are driving more miles,” the report states, in part. “There has been a noticeable spike since 2013 in miles driven, coinciding with the increase in claim frequency.”

Between 2004 and 2013, miles driven increased by 26.2 billion miles, according to the National Highway Traffic Safety Administration (NHTSA). Over the last three years, however, miles driven has increased by an estimated 207 billion miles. Last year alone, Americans drove 3.2 trillion miles, the highest recorded total since 1991.

“This is a significant issue, and not only for GAP providers,” says Protective’s Karchunas. “These challenging trends also show up in the loss performance of many of the prominent publicly traded auto insurers.

“From a GAP perspective, more miles driven means a couple of things: Vehicles depreciate over time, and they depreciate faster when more miles are on the vehicle at time of loss,” he added. “So when an insurance company determines the value of your vehicle once it’s been totaled, the valuation is often lower based on a vehicle with higher mileage. The end result is the gap between the vehicle’s value and balance due on the loan widens.”

Ad Loading...

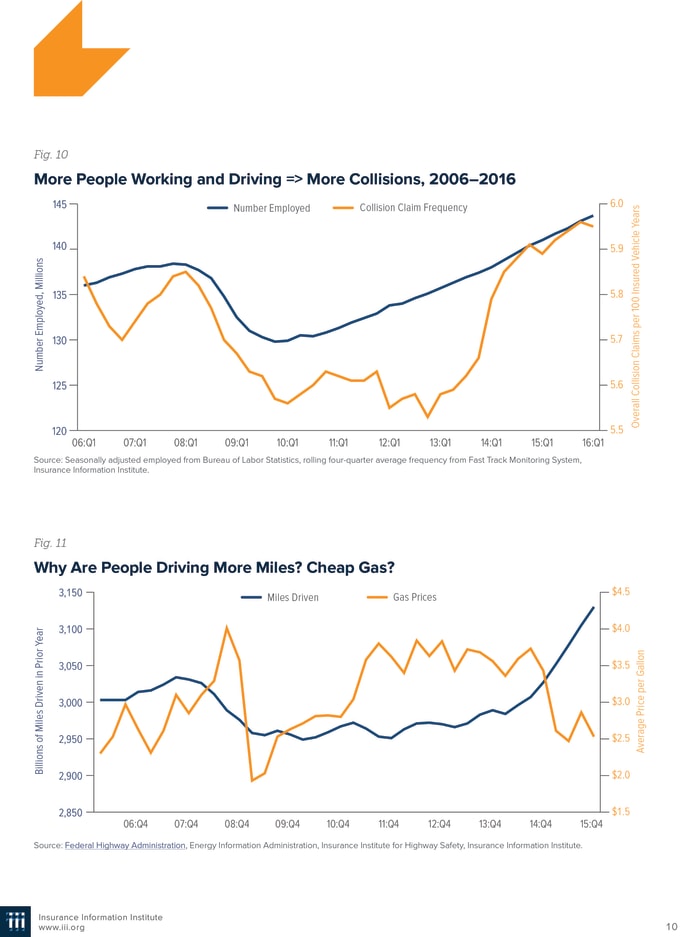

The most likely reason for the increase in miles driven is that more people are employed, according to the III’s report. Last year, the U.S. labor market posted a net employment gain of 2.4 million jobs, with hires totaling 62.5 million — the most in any year since 2006, according to the U.S. Department of Labor. And as miles driven rose after the Great Recession, so did claim frequency.

The organization also explored the link between gas prices and miles driven, but concluded the connection is weak at best. “There was a period in late 2014 and early 2015 in which miles driven rose as gasoline prices fell,” the III’s report notes. “Over the past few years, though, the link seems weaker.”

John Pappanastos

John Pappanastos, CEO and president of EFG Companies, counts the proliferation of ride-hailing services among the possible reasons for the increase in miles driven. Problem is, drivers for these services aren’t being truthful about what they do for a living. “You know, none of us used to write GAP or [vehicle service contracts] on commercial vehicles, and we don’t offer coverage on taxis,” he says. “Now we’re writing them on taxis without knowing it.”

The executive says he believes the situation also impacts service contract rates. “So the cost of a VSC for Uber is going to drive up VSC rates,” he speculates. “Everybody is going to have to share the cost increases, because we can’t tell which ones are Uber and which ones aren’t.”

Severe weather events have also contributed to the rise in auto insurance claims, according to the III’s report. Arkansas, Louisiana, Oklahoma and Texas, for example, have seen inordinate amounts of flooding, with The Weather Channel noting significant storms between March and December 2016. Texas also recorded a record 240 tornados in 2015.

Ad Loading...

Hail is another issue. In early 2016, for example, Texas was struck by a series of significant hail storms. Three April storms around San Antonio resulted in 136,000 damaged vehicles, while March hailstorms in Fort Worth and Plano resulted in $1.3 billion in insurance claims. A storm on April 11 in Wylie, Texas, also caused $300 million in insurance claims, much of it to insured vehicles.

“Floods and hail are killing us,” says Tony Wanderon, president and CEO of National Auto Care. “Hurricanes don’t bother us, but all the floods we’ve had in the Midwest and Texas and all the hailstorms — frequencies are probably three or four times what they’ve’ ever been historically.”

Rising Repair Cost The purpose of the III’s report was to explain the rise in insurance rates, which “have drawn considerable media and regulatory scrutiny,” the report notes. Last April, auto insurance prices experienced their highest monthly spike since 2003, rising 7.2%, according to the federal government’s Consumer Price Index.

And through the first nine months of 2016, the U.S. property and casualty insurance industry posted an underwriting loss of $1.7 billion and was en route to a $2.3 billion loss by year’s end, according to A.M. Best. Although the final total wasn’t available at press time, the ratings agency said the industry was on pace to suffer its first underwriting loss since 2012. The firm blamed weather events, underinsured and distracted drivers, higher repair costs, and cheap gas, among other factors.

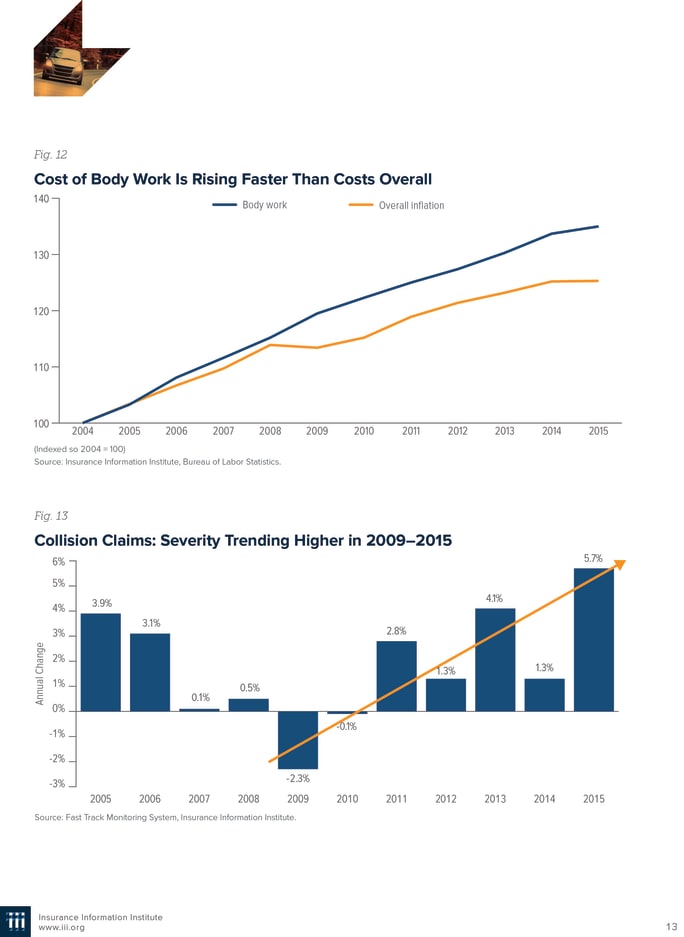

According to the III, prices for motor vehicle parts and equipment stabilized last year to 2011 levels, but that’s after prices rose every month between August 2000 and August 2012 for a cumulative gain of 46.7%. And the higher repair costs go, the more likely insurance companies are to total vehicles.

Ad Loading...

While it varies by state and insurer, the value percentage that triggers a totaling is typically between 70% and 90% of the vehicle’s resale value. In most states, insurers are legally required to declare a total loss once a vehicle reaches a certain value threshold that is set by the state. In Oklahoma, for example, that threshold is 60%. In Oregon, it’s 80%.

“I can tell you more cars are totaled just because of electronics. You’ve got sensors on cars, airbags. You’ve got so many different little pieces that cost so much money to repair,” says Wanderon, who is widely considered the industry’s GAP guru. “I mean, if you look at an F-250 or F-350 tailgate, it’s $5,500 to replace a tailgate because of all the electronics. Most states require 50% value before they total it. More cars are being totaled just because all six airbags deployed, so you got $4,000, $5,000 worth of airbags you’ve go to replace.”

Deeper Concerns

During normal times, Wanderon says, GAP claim frequency sits between 2% and 2.5%, with severity of about $2,300 to $2,700. During the recessionary period of 2009 to 2011, severities were about $1,600 to $1,800, he adds. Now they’re anywhere between $3,200 and $4,500, with frequency running at about 3% to 5%, depending on the GAP writer’s book of business.

Wanderon believes GAP providers are probably two years behind on rate increases. “Dealers need to make sure the companies they’re doing business with are adequately reserving to pay the claims,” he says. “I think the companies are trying not to lose market share, so they’re taking rates up gradually. But in reality, many should be raising their rates by 30% to 50%.”

Ad Loading...

Wanderon outlined the challenges facing GAP at the GAPA event this past fall. The bulk of his presentation centered on auto finance trends he says are having a significant impact on the product’s performance, including negative equity carryover, rising advance amounts, and stretching loan terms. The normalization or drop in resale and residual values is also impacting performance, he adds.

During the first three quarters of 2016, an estimated 32% of all trade-ins rolled into a new-vehicle purchase were under water — the highest on record, according to an Edmunds report. The amount of negative equity car buyers rolled over also reached a record high, averaging about $4,832.

As for loan lengths, Experian reported that the average term in the third quarter of 2016 rose one month from the prior-year period to 68 months. A year earlier, TransUnion reported that the average term between 2010 and 2015 rose five months to 67 months, with seven out of 10 new auto loans having terms longer than 60 months. And a quarter of all loans originated in 2015’s third quarter, the firm added, had terms in the 73- to 84-month term band.

It’s clear that consumers are seeking out payment relief and finance sources are obliging. Experian reported that the average amount finance in the third quarter jumped $1,086 from the prior-year period to $30,022. By December, Kelley Blue Book reported that the average transaction price for light vehicles reached an all-time record high of $35,309.

Although there is no data tracking advance amounts, Wanderon says they’re reaching concerning levels as well. “We’ve seen deals as high as 225% of MSRP advancement. We’re also seeing $15,000 to $18,000 of negative equity carryovers,” he says. “I mean, $15,000 to $18,000 of negative equity carryovers, which, from what I can see — and we don’t gather the information — have 600, 650 Beacon scores. That factor is clearly driving the severities.

Ad Loading...

“We’re also seeing much higher longer term financing that ever before,” he adds. “I mean, you can go back to 2007, 2008, which everybody says were crazy times. That was mild compared to today.”

Representative from Equifax, Experian, and TransUnion shot down claims of a subprime bubble during a panel session at the American Financial Services Association (AFSA)’s 2017 Vehicle Finance Conference and Exposition in late January. The event preceded the NADA convention in New Orleans.

Equifax’s Amy Crews Cutts said there is no bubble because, unlike in the mortgage segment, there’s no asset-flipping in auto finance. TransUnion’s Jason Laky said that, even if half of all auto loans defaulted, finance sources would be able to recover most of that inventory. Experian’s Melinda Zabritski blamed the appearance of a bubble on several factors, including the “massive trough” that appeared when the lending market came to a screeching halt in 2009. That’s when the Great Recession was in full swing.

Wanderon, however, was unmoved. “Look, I’d debate anybody in the industry and tell them that there’s never been a time that I’ve seen auto lending so loose,” he says. “It’s great for the dealer and the consumer, but I’ve been telling dealers this for a while, ‘Put away some money right now, because we’re gonna have a pretty severe slowdown in the marketplace in the next 24 months.’”

‘Profit’ Isn’t a Bad Word

Ad Loading...

What frustrates EFG Companies’ Pappanastos is that some providers have been slow to respond to the situation. That forces EFG to push some clients who balk at its rising rates to other providers. Based on conversations he’s had with other carriers, that should change this year. “It’s not something I like doing, because we don’t like to let a competitor have a foothold on any account,” he says. “This is a very significant trend, and it’s plaguing everyone.”

The executive says the company began to feel the sting of rising claims right after signing up as the exclusive product provider for a major subprime finance source. Since then, performance of the product has defied all expectations, making it difficult to know where the product needs to be priced.

“I don’t know why subprime borrowers have more accidents, but I do know why their severity is greater,” he says, noting that frequency runs at about 3% for the company’s prime business and at about 6% to 7.5% for subprime.

“There was an article in the press a few months ago that says 31% of auto loans now roll in negative equity. The average was like $4,000 per loan. Well, with subprime, it’s greater,” he adds. “Then you give them a 20% or 23% interest rate, and they’re paying down less principal on their auto loan than their car is depreciating. So the loan-to-value actually increases over the life of their loan.”

Sitting at or below 13% between 2011 and 2015, the depreciation rate now sits at 17.3%, according to Black Book’s Anil Goyal. That’s right in that normal 16% to 18% range. And based on the trends he’s seeing, the executive believes a sustained level of high depreciations is here to stay — at least for a few more years.

Ad Loading...

One of those trends is leasing. Edmunds reported last month that lease volume reached an all-time high of 4.3 million vehicles in 2016. That equated to a penetration rate of 31%, a level Goyal says is unsustainable. “The reason why leasing has taken off is because it has been subvented heavily to keep the monthly payment down,” he says, noting that the gap between a lease payment and a normal car payment continues to widen. The difference between last year and this year, he adds, is remarketers are going to feel the pinch.

“So what happened was, when those cars came back, the remarketers still made money, because the values were so high,” he says. “So you were still in positive territory in terms of not losing money at the back end. But you’re entering that area now, and in 2017, you’re gonna start losing money.”

Incentive levels are another reason the depreciation rate will remain elevated. Goyal says incentives reached 11% of MSRP last year, noting that they are normally 9% of MSRP. Then there’s the lease-return situation, with Experian reporting that approximately three million leases are set to expire in the next 12 months. And Goyal doesn’t believe CPO sales will be enough to offset the returning supply.

“Last year, certified pre-owned only grew about 3.5%, compared to lease returns [at] 25%,” he says. “So it’s not growing as big to absorb all those lease returns.”

As for the credit situation, Goyal believes 2017 will be the year finance sources tighten up. And with the unemployment rate sitting below 5%, he believes the Federal Reserve will be more inclined to raise rates this year. “Nearly every finance lender we talk to is tightening that criteria,” he says. “So from an F&I manager’s perspective, I think it would be important to really build relationships and identify which lenders are looking to grow or shrink their business in different risk bands.”

Ad Loading...

There’s another issue that could impact GAP performance: regulators. In recent years, regulatory insiders have warned that the Consumer Financial Protection Bureau (CFPB) is preparing to target F&I products, and the one product the bureau may have the authority to regulate is GAP. The thought is that the bureau may consider the product part of an extension of credit since the finance source is waiving its right to collect a portion of its debt.

Then there’s this line in the CFPB’s June 2015 Auto Finance Examination Procedures: “Determine how the servicer monitors optional products attached to loans or leases, including canceling the products in a timely manner, where applicable.” While the document doesn’t define a “timely manner,” a white paper issued by F&I Express in August 2015 points to the 15 days the bureau gives finance sources to respond to a consumer complaint as a possible guide. And failure to cancel in a timely manner, the white paper warns, “may be considered an abusive practice.”

That year, F&I Express launched Express Recoveries, an online system designed to help finance sources obtain cancelation refund amounts and electronically file cancelation requests directly with product providers. In September, Dealertrack announced it would begin marketing and selling the platform to its 6,800 lender partners through its finance platform. F&I Express reported in January that more than a dozen finance sources are currently using the platform, with most major product providers expected to be connected by mid-2017.

GPW and Associates’ Kirsits, however, doesn’t believe GAP providers have baked that additional refund exposure into the pricing of the product, which could cause further deterioration, he says.

“The truth is that most administrators don’t make enough front-end commission on GAP to warrant the back-end exposure, which can be substantial,” EFG Companies’ Pappanastos says.

Ad Loading...

Wanderon puts it a different way. “You know, people think GAP companies are making money, but nobody’s getting rich in the GAP business right now,” he says. “And that’s the nature of the beast. You’re either making money on it or you’re not. And there doesn’t seem to be a real sweet spot in between.

“So, just like dealers complain about people not wanting them to make a profit, let your providers make a fair return,” he adds. “And if you don’t believe it’s true, have them prove it to you.”

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

What’s the atmosphere saying about you to your customers? You can make minor adjustments and additions that transform your space into one that creates trust with the people on the other side of the desk.

How can auto dealerships help F&I managers fulfill their vital role in the most effective ways? Industry expert Rick McCormick shares his insights on the best ways to train these professionals and help them maintain good habits.

Some of it should be given to the customer, but that doesn’t mean the F&I office relinquishes the process. In fact, a different approach both builds trust and boosts sales.

Talk to F&I customers like you’d talk to a friend, without industry lingo or sales-like questions, and use hard proof to show, not tell, them about a need.

Helping F&I customers understand complementary offerings is likely to lead to more sales, based on the success of a high-performing practitioner of the philosophy.