CFPB Accuses 'One or More' Finance Sources of Deceptive GAP Ads, Payment Deferral Offers

In its recent Supervisory Highlights report, the CFPB accused ‘one or more’ auto finance sources of being deceptive in their advertisements of GAP and in the way they disclose payment deferral terms.

WASHINGTON, D.C. — In its summer edition of Supervisory Highlights, the Consumer Financial Protection Bureau accused one or more finance sources of being deceptive in their advertisements of GAP and in the way they disclose payment deferral terms.

According to the report, the GAP advertisements gave the impression that the product fully covered the remaining balance of a consumer’s loan in the event of a total loss, when, according to the bureau, the products only covered the amounts below a certain loan-to-value ratio.

Bureau examiners also accused one or more auto finance sources of using a telephone script that “created the false overall net impression that the only effects of taking advantage of a loan deferral would be to extend the maturity of the loan and to accrue interest during the deferral. The finance sources, the bureau charged, failed to inform consumers that “the subsequent payment would be applied to the interest earned on the unpaid amount financed from the date of the last payment received from the consumer.” The result, the bureau said, is consumers are paying more finance charges than originally disclosed.

“These violations are under review by the bureau to determine what, if any, remedial and corrective actions should be undertaken by the relevant financial institutions,” the bureau added.

The bureau’s Supervisory Highlights report also noted that examiners determined that “weak [complaint management systems]” in place at one or more institutions allowed violations of federal consumer financial law during the review period. Weaknesses included:

Failure to raise compliance-related issues to the institution’s board of directors or other principal.

Failure to follow the institution’s policies and procedures in daily practice.

Failure to properly monitor and correct business line practices to align with federal consumer financial law.

Failure to adequately track training completed by employees and the board.

Failure to adequately follow up on consumer complaints with a corresponding failure of compliance audit to highlight deficiencies in the consumer complaint response process.

“The relevant financial institutions have undertaken remedial and corrective actions regarding these violations, which are under review by the bureau,” the report stated.

According to the bureau’s June Complaint Report, the CFPB has logged 23,000 auto finance-related complaints since July 21, 2011, representing 60% of consumer loan complaints. The Top 2 complaints were “Managing the loan, lease or line of credit” at 47%, and “Problems when you are unable to pay” at 22%.

“Taking out a loan or lease or account terms and changes” ranked third at 18%, following by “Shopping for a loan, lease or line of credit” at 11%.

According to the report, consumers complained about payment processing issues, including not having their payment applied to their accounts in a timely or correct manner. Consumers also complained of repossessions without notice or having to voluntarily surrender their vehicle because they could no longer afford their payments.

Consumers also complained that “warranties they believe … they were required to purchase” did not cover basic repairs. “In these complaints, consumers purchased older cars and they were under the impression that the warranty would cover the repairs often associated with cars that have high mileage,” the bureau stated in its report. “Since these repairs were not covered, consumers incurred high costs to fix their cars or in some instances were unable to make further use of the vehicle.”

The bureau also received complaints about misleading advertisements at buy-here, pay-here dealerships. “Consumers explained that dealerships checked their credit even though advertisements stated that their credit would not be considered,” the report stated. “Consumers also complained that although advertisements stated that making timely payments on their loans would help build their credit up, dealerships would not furnish good-standing credit information.”

Consumers also complained about having to pay what they felt were high wear-and-tear fees at the end of their lease. “These consumers explained that they disagreed with the wear-and-tear determinations and believed the process was unfair,” the report stated. “Because there is a subjective element to this determination, consumers indicated that they should be allowed to be present for the inspection.”

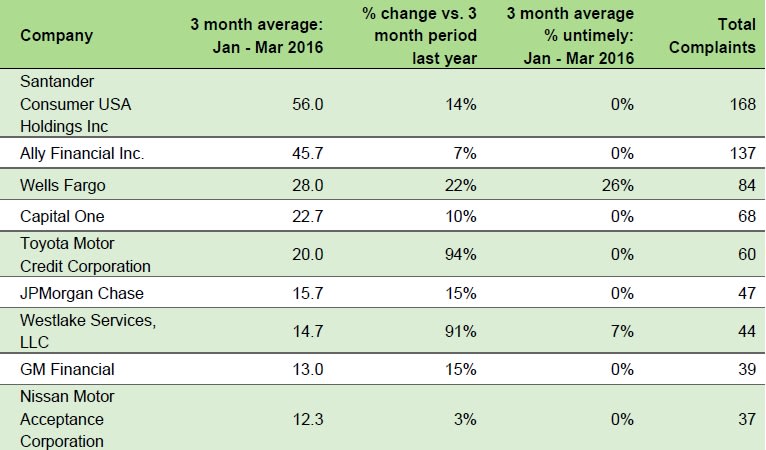

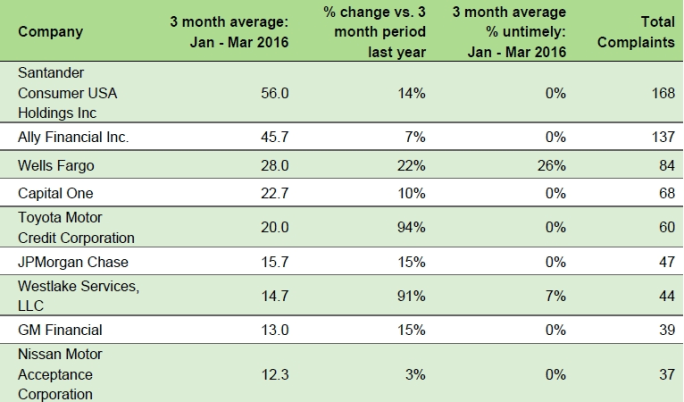

The bureau’s complaint report also contained a list of most-complained-about companies, which included Santander, Ally Financial, Wells Fargo, Capital One, Toyota Motor Corp., JPMorgan Chase, Westlake Financial Services, GM Financial, and Nissan Motor Acceptance Corp. The companies listed, according to the bureau, account for 50% of all auto finance-related complaints “sent to companies for response in January to March 2016.

“Of these companies, Toyota Motor Credit Corp. saw the greatest percentage increase in auto lending complaints (94%) from January – March 2015 to January – March 2016,” the report stated, adding that Nissan Motor Acceptance Corp. “saw the lease percentage increase in consumer loan complaints (3%) during the same period.

More F&I

Why Your F&I PVR Is Misleading You

Here’s a handy checklist of the numbers to track in 2026 instead.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →

Humble and Hungry: 12 Rules for an F&I Life

Dustin Gingerich, with a decade in the F&I business under his belt, shares his thoughts on leadership, building trust with customers, and the importance of learning and innovation.

Read More →

Focus on the Opening

F&I managers must learn as much as possible about their customers, starting before they walk into their offices. The bulk of today’s consumers expect that, and good results will follow.

Read More →

F&I Reaches for the Sky

The increasingly important profit center continued making gains in the first quarter, according to StoneEagle data, ancillary products proving more popular as consumers hold onto their buys longer.

Read More →

Timing the Market Can Hurt Long-Term Program Performance

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

The 90/10 Rule

In this video, Ryan Ruff explains the rule that elite sales professionals use to turn ordinary conversations into unforgettable customer experiences.

Read More →

Your Office Is Talking

What’s the atmosphere saying about you to your customers? You can make minor adjustments and additions that transform your space into one that creates trust with the people on the other side of the desk.

Read More →

F&I Training Fundamentals

How can auto dealerships help F&I managers fulfill their vital role in the most effective ways? Industry expert Rick McCormick shares his insights on the best ways to train these professionals and help them maintain good habits.

Read More →

Not Just Any Tire Will Do

More consumers and businesses are opting for all-season options for various reasons as safety, sustainability and convenience push practical change.

Read More →